When Genius Spots a Bubble: Michael Burry’s 2025 Portfolio Shift and What Singapore Investors Should Learn

The man who called 2008 is now warning us about AI excess. Is it time to get defensive—or is this just bearish noise?

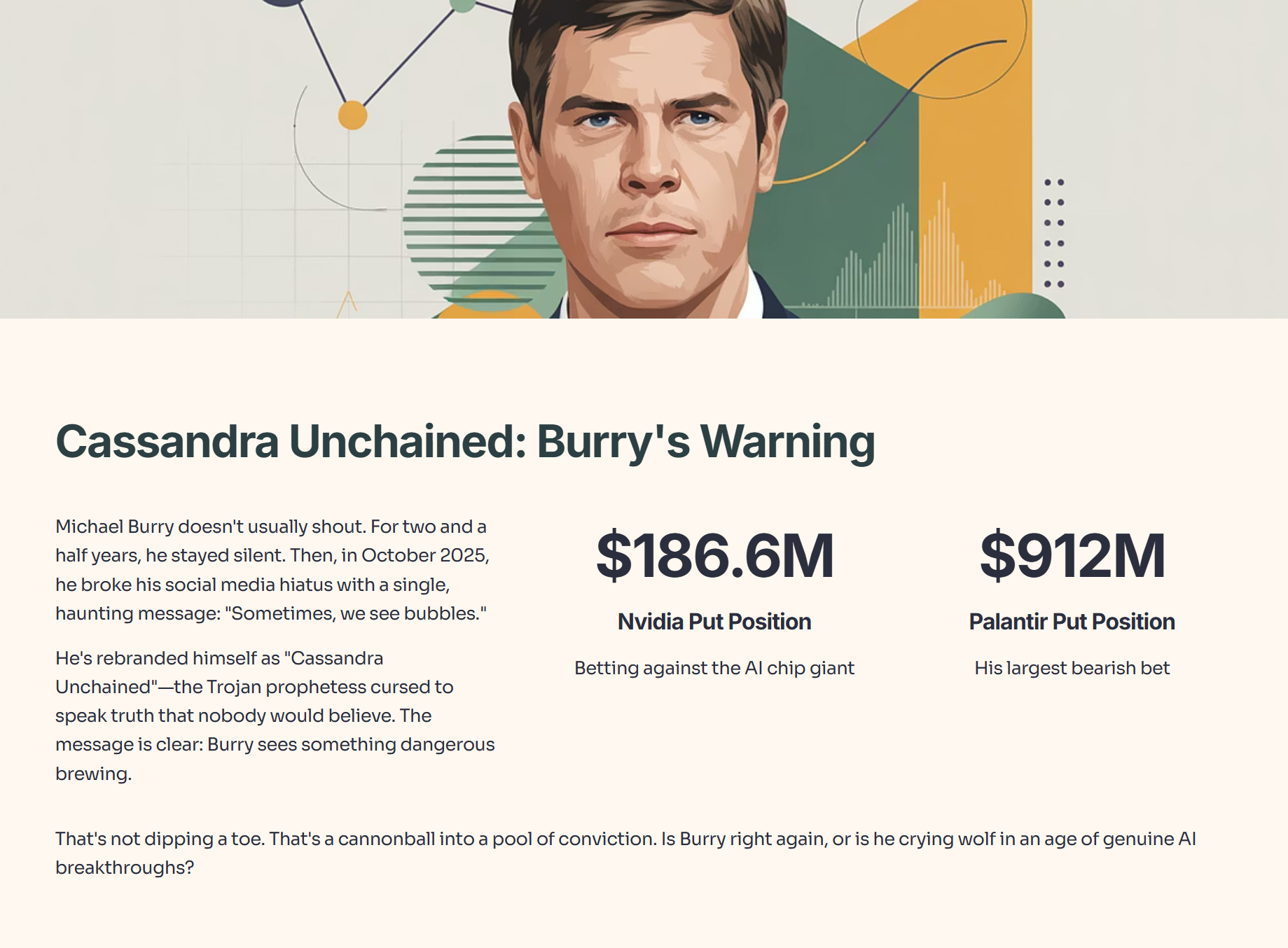

Michael Burry doesn’t usually shout. For two and a half years, he stayed silent. Then, in October 2025, he broke his social media hiatus with a single, haunting message: “Sometimes, we see bubbles.” Attached was an image from his iconic role in The Big Short—the film that documented his prescient call on the 2008 housing collapse.

This time, he’s rebranded himself as “Cassandra Unchained.” Cassandra was the Trojan prophetess cursed to speak truth that nobody would believe. The message is clear: Burry sees something dangerous brewing, and he’s betting big money against it.

Within weeks, regulatory filings revealed the details. Scion Asset Management, Burry’s hedge fund, loaded up on put options—bets that profit if stock prices fall—targeting two of the market’s darlings: Nvidia and Palantir Technologies. He wasn’t just cautiously skeptical. He went all in with a $186.6 million put position on Nvidia and a massive $912 million put position on Palantir. That’s not dipping a toe. That’s a cannonball into a pool of conviction.

The question you should ask: Is Burry right again, or is he crying wolf in an age of genuine artificial intelligence breakthroughs?

In This Article:

• The Case Against Nvidia: Valuation Meets Geopolitics

• The Fundamental Case for Nvidia

• Geopolitical Risk: The Silent Killer

• Palantir: Hype Over Fundamentals?

• The Selective Bullishness: Where Burry Finds Value

• Why Meta?

• Why UnitedHealth?

• Is Burry Right? The Case for Skepticism

• What Singapore Investors Should Actually Do

• First: Acknowledge the Real Risks

• Second: Look for Resilient Businesses

• Third: Diversify Your Time Horizon

• The Bigger Picture: Capital Preservation in Uncertain Times

• Your Next StepsThe Case Against Nvidia: Valuation Meets Geopolitics

Let’s start with the numbers. Nvidia reached a $5 trillion market capitalization in October 2025—a historic milestone. It’s the world’s first company to touch that threshold. In twelve months, Nvidia climbed from $4 trillion to $5 trillion. The stock jumped 50% in 2025 alone.

To put that in perspective, $5 trillion is more than ten times the entire market capitalization of the Singapore Exchange (SGX).

On paper, this looks absurd. But before we dismiss Burry outright, we need to understand why valuations got this extreme.

The Fundamental Case for Nvidia

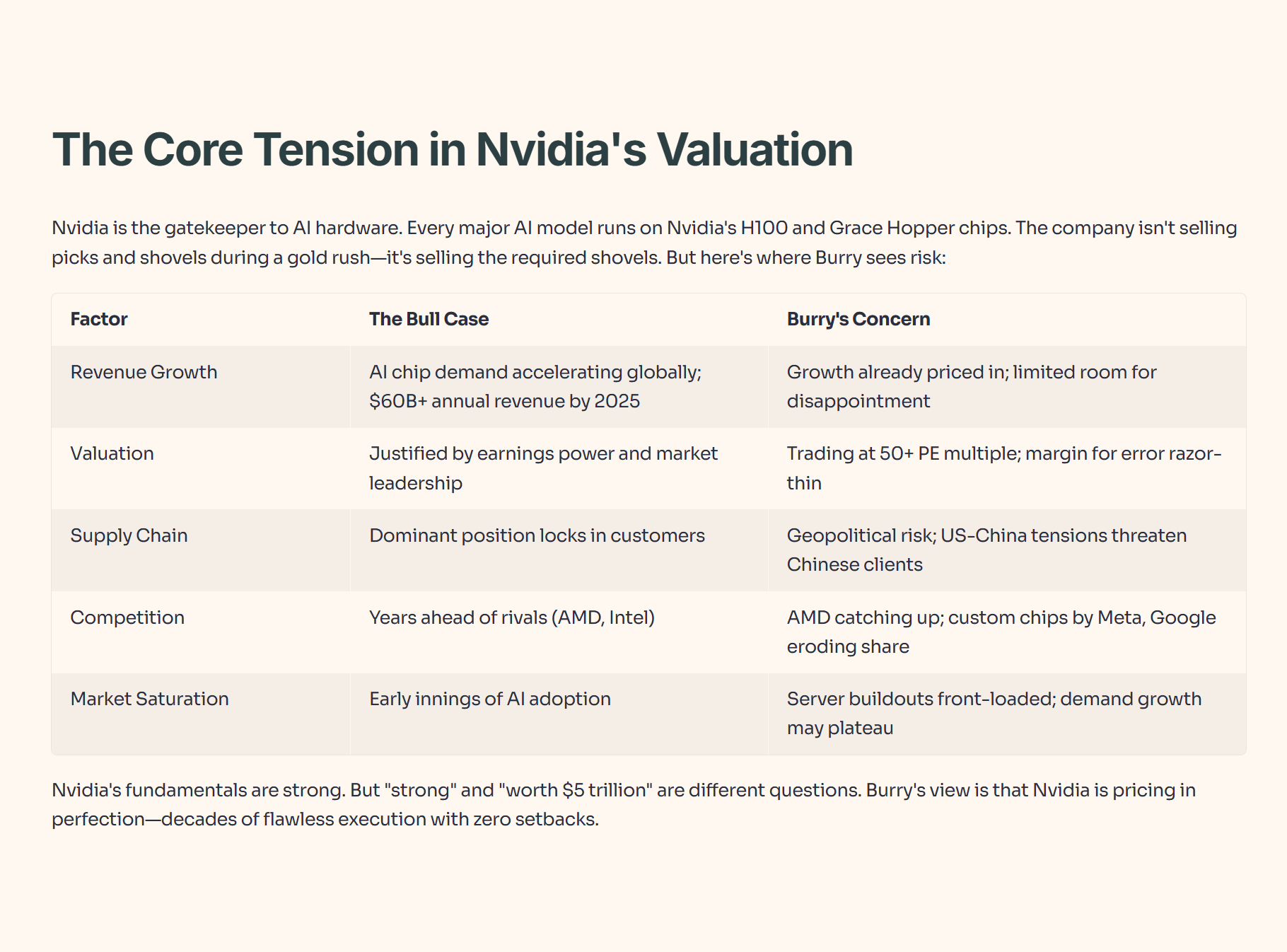

Nvidia is the gatekeeper to artificial intelligence hardware. Every AI model that matters—from OpenAI’s GPT series to Meta’s LLaMA—runs on Nvidia’s H100 and newer Grace Hopper chips. The company isn’t selling picks and shovels during a gold rush; it’s selling the required shovels. Revenue scales with AI adoption. That’s a real moat.

But here’s where Burry sees risk:

Table 1: The Core Tension in Nvidia’s Valuation

The chart above captures the core tension. Nvidia’s fundamentals are strong. But “strong” and “worth $5 trillion” are different questions. Burry’s view is that Nvidia is pricing in perfection—decades of flawless execution with zero setbacks. History suggests that’s a bad bet.

Geopolitical Risk: The Silent Killer

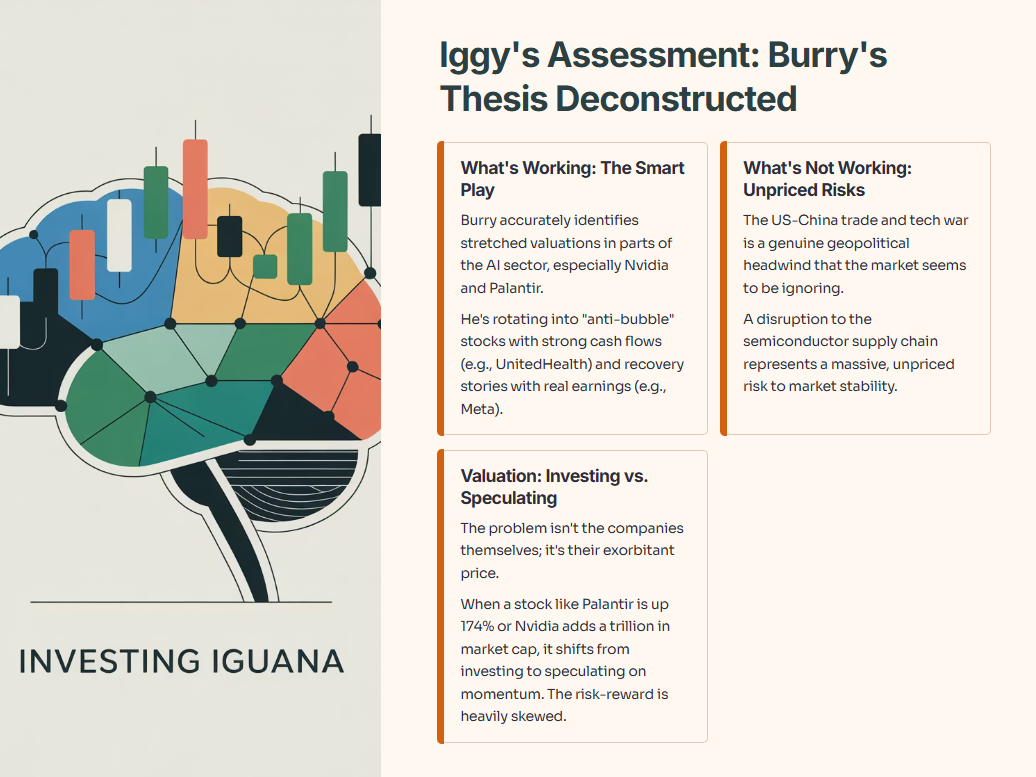

Here’s the wrinkle Burry can’t ignore. Nvidia’s largest growth markets include China. Chinese tech firms like Alibaba, Baidu, and Tencent depend on Nvidia chips for their AI infrastructure. But US-China trade tensions are escalating.

In October 2025, the Trump administration imposed 100% tariffs on Chinese exports and slapped restrictions on semiconductor exports to China. China retaliated by limiting rare earth exports—critical materials for semiconductor manufacturing. This isn’t just noise. This is the foundation of Nvidia’s supply chain and customer base under pressure.

Burry liquidated his positions in major Chinese tech firms, reflecting this exact concern. He knows that if US-China tensions worsen, Nvidia’s growth in its second-largest market could stall. Worse, Chinese competitors—backed by government subsidies—are racing to achieve semiconductor self-sufficiency. That’s an existential threat to Nvidia’s moat in the long run.

Table 2: Key Geopolitical Risks to Nvidia’s Business

This table shows why Burry is nervous. It’s not that Nvidia’s business is broken today. It’s that the risk environment is deteriorating faster than the stock price is pricing it in.

For Singapore, which thrives on regional stability and is a key node in the semiconductor supply chain (think SGX-listed names like AEM Holdings or UMS Holdings), this isn’t a distant threat. A disruption to TSMC in Taiwan would be felt directly in our own market.

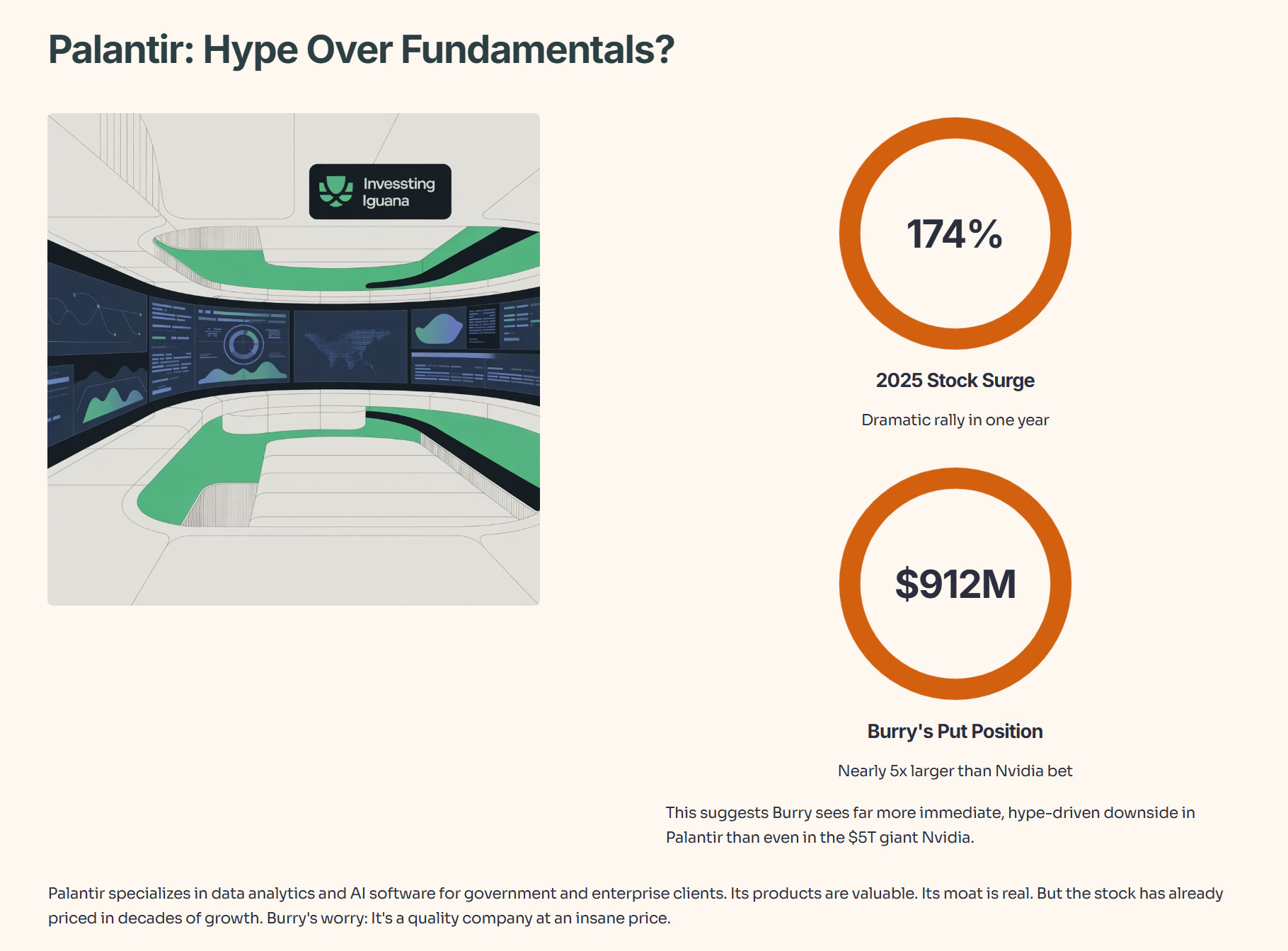

Palantir: Hype Over Fundamentals?

Palantir Technologies saw an even more dramatic move: up 174% in 2025. Burry took a $912 million put position—a bet nearly five times larger than his Nvidia one.

This suggests Burry sees far more immediate, hype-driven downside in Palantir than even in the $5T giant Nvidia.

Why? Look at the valuation. Palantir trades on promise, not current profitability. The company specializes in data analytics and AI software for government and enterprise clients. Its products are valuable. Its moat is real. But the stock has already priced in decades of growth.

Burry’s worry: Palantir is a quality company at an insane price. It’s the difference between buying a good house and overpaying by 300%. Yes, it’s a good house. But paying $3 million for a $1 million home is still a bad investment. When growth expectations reset—even slightly—the downside is brutal.

The Selective Bullishness: Where Burry Finds Value

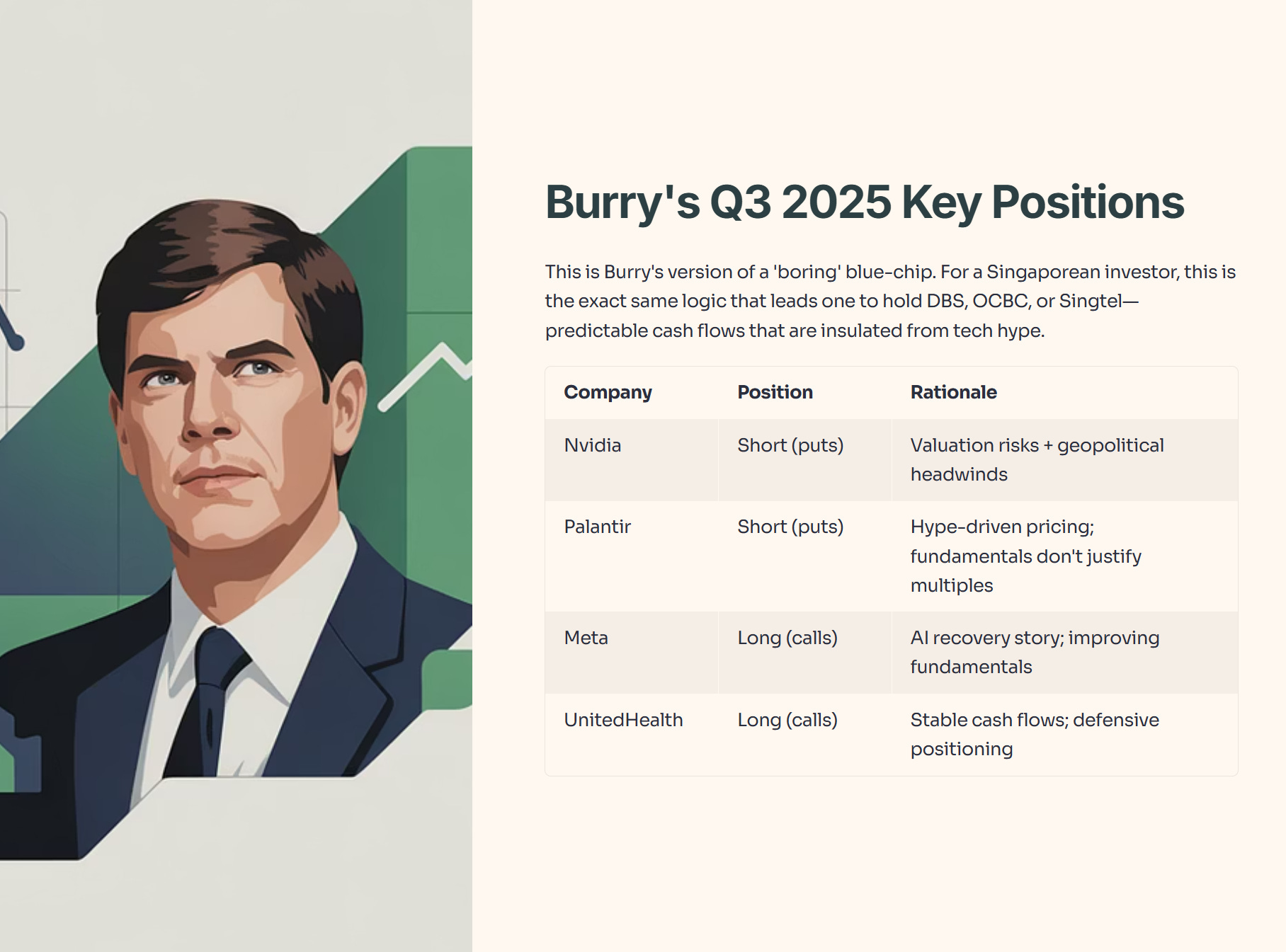

Here’s where Burry’s strategy gets interesting. He’s not simply going short. His Q3 2025 filings also show call options on Meta and UnitedHealth—bullish bets that these stocks will rise.

Why Meta?

Meta faced brutal headwinds in 2021–2024. Apple’s privacy changes decimated its ad targeting. Wall Street abandoned it. But by 2025, Meta’s AI infrastructure investments are paying off. Its data center buildout is positioning it as a serious player in AI training and inference. Meanwhile, its traditional ad business is stabilizing. Burry sees a recovery story with actual earnings growth—not just hype.

Why UnitedHealth?

UnitedHealth is a stalwart healthcare company with predictable cash flows, strong management, and a growing business (especially after acquiring Amedisys in August 2025). It’s the anti-bubble: boring, profitable, and priced rationally.

This is Burry’s version of a ‘boring’ blue-chip. For a Singaporean investor, this is the exact same logic that leads one to hold DBS, OCBC, or Singtel—predictable cash flows that are insulated from tech hype.

Table 3: Burry’s Q3 2025 Key Positions

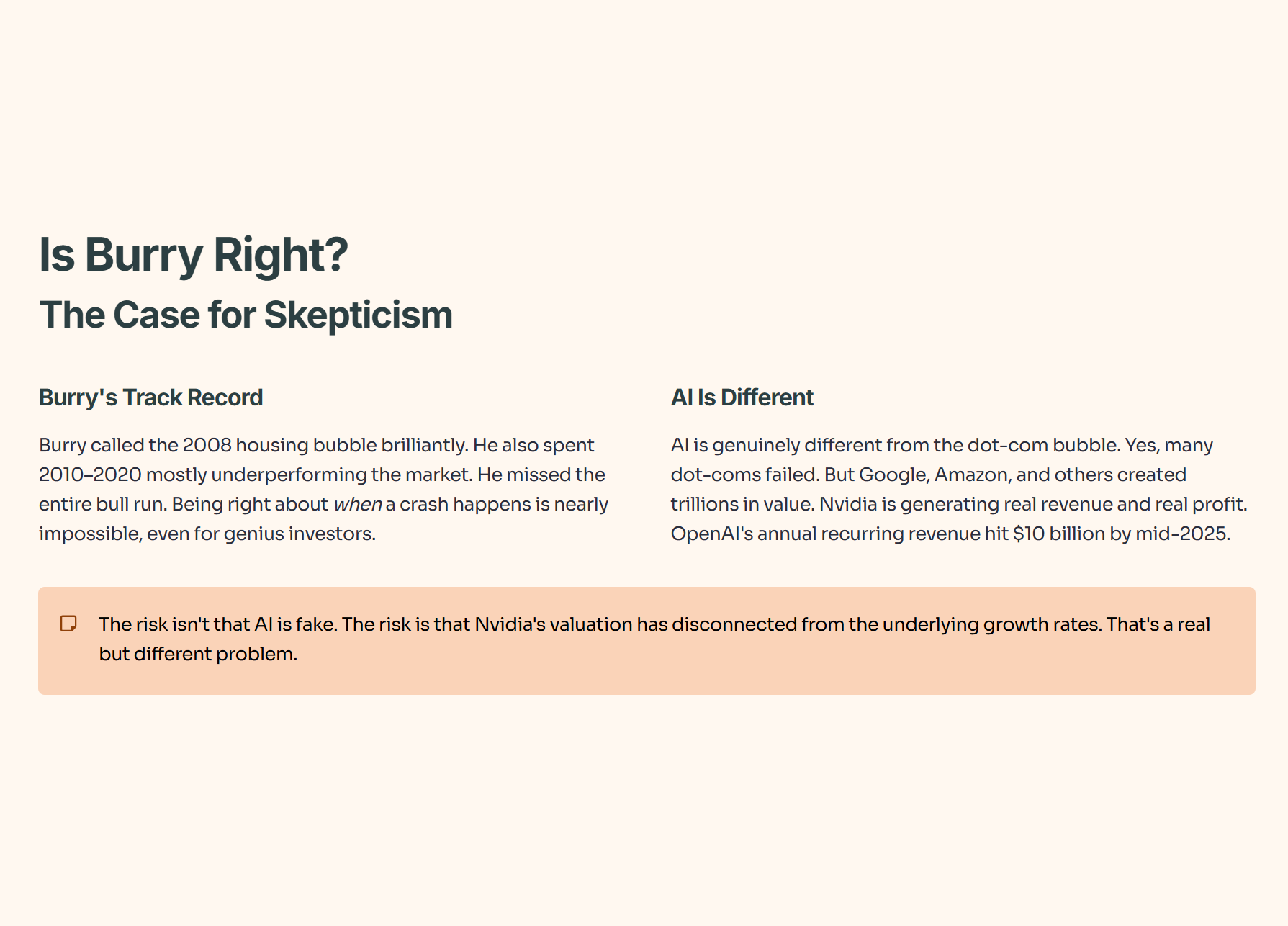

Is Burry Right? The Case for Skepticism

Before you lock in your own short positions, consider this: Burry called the 2008 housing bubble brilliantly. He also spent 2010–2020 mostly underperforming the market. He missed the entire bull run. Being right about when a crash happens is nearly impossible, even for genius investors.

Also, AI is genuinely different from the dot-com bubble. Yes, many dot-coms failed. But Google, Amazon, and a handful of others created trillions in value. Nvidia, despite being expensive, is generating real revenue and real profit. OpenAI’s annual recurring revenue hit $10 billion by mid-2025. Anthropic jumped from $100 million to $4.5 billion. These are actual businesses, not vaporware.

The risk isn’t that AI is fake. The risk is that Nvidia’s valuation has disconnected from the underlying growth rates. That’s a real but different problem.

What Singapore Investors Should Actually Do

This is where Burry’s thesis gets practical for us in Singapore.