When Profit Grows Faster Than Revenue: ST Engineering's 1H2025 Results Signal Something Big

Plus the order book bombshell that should have every SGX investor paying attention

When Profit Grows Faster Than Revenue: ST Engineering's 1H2025 Results Signal Something Big

Plus the order book bombshell that should have every SGX investor paying attention

Hey everyone, this is Iggy breaking down what might be the most important set of results to cross my desk this earnings season. ST Engineering just dropped their first-half 2025 numbers, and while some traders faded the print, the market is missing something big here.

As your Singapore financial analyst who has tracked aerospace and defense across cycles, I’ve seen enough earnings to know when quality is compounding. ST Engineering’s report shows profit growing faster than revenue, strong backlog visibility, and cleaner balance sheet math. That’s the trio you want when building CPF and SRS core positions.

Here’s the plan for today’s deep dive. We’ll go slide by slide through the company’s 1H2025 presentation to unpack the drivers behind margin expansion, the $31.2b order book, the quality of new wins, debt dynamics, portfolio moves, and the dividend cadence. I’ll keep this SG-first, with clear takeaways you can act on.

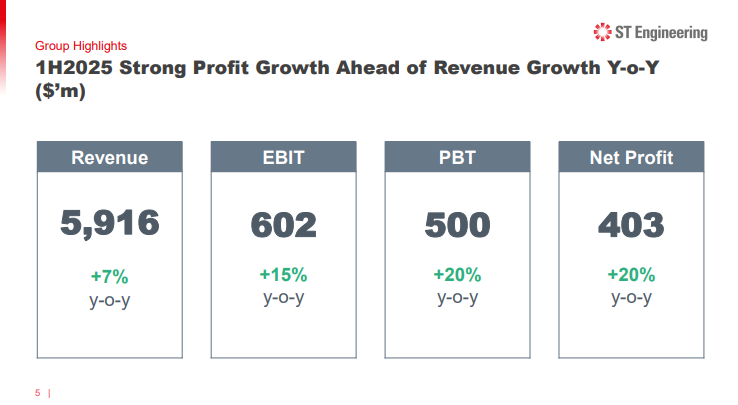

Slide 5: Group Financial Highlights – The Profit Growth Story

ST Engineering delivered what long-term investors prize: profit outpacing revenue. For 1H2025, revenue rose 7% year-on-year to $5,916m, EBIT climbed 15% to $602m, and net profit rose 20% to $403m. EPS printed 12.93 cents versus 10.80 cents a year ago.

Why this matters: when EBIT grows roughly double revenue, you’re seeing operating leverage, better pricing/mix, and cost discipline. In SG portfolios, this profile supports both payout stability and long-term value creation. Think of it like upgrading a hawker stall to a franchise—same ingredients, better throughput and pricing power.