Which CapitaLand REIT Is the Top Iguana Pick? Real Data, Real Risks – Let’s Cut Through the Noise

Too many CapitaLand REITs, too little clarity? Confused by all the market chatter about which is best for your CPF or cash portfolio? Here’s the deep-dive breakdown Singapore investors need.

Editor’s Note: This post was updated on October 19, 2025, to reflect the latest market data. More importantly, it has been refined to remove repetition and provide a sharper, more streamlined “Action Plan” and a consolidated “Final Iguana Verdict.”

Are you tired of analysts giving vague “it depends” answers on CapitaLand’s REITs? Whether you’re looking for income, diversification, or the next big thing, the CapitaLand stable offers several strong choices – but “strong” means different things for different risk appetites, asset classes, and timeframes. If you find yourself second-guessing which one truly fits your goals (and wondering if you should just “buy them all” like a buffet), you’re not alone.

This article promises clarity, numbers, a fair ranking across four major CapitaLand REITs, and – critically – a straightforward action plan. I’ll pull apart the flash, focus on the fundamentals, and show you not just which REIT is “biggest” or “cheapest,” but which setup is most likely to serve your specific needs in the next 12–18 months. Let’s get tactical, not just theoretical.

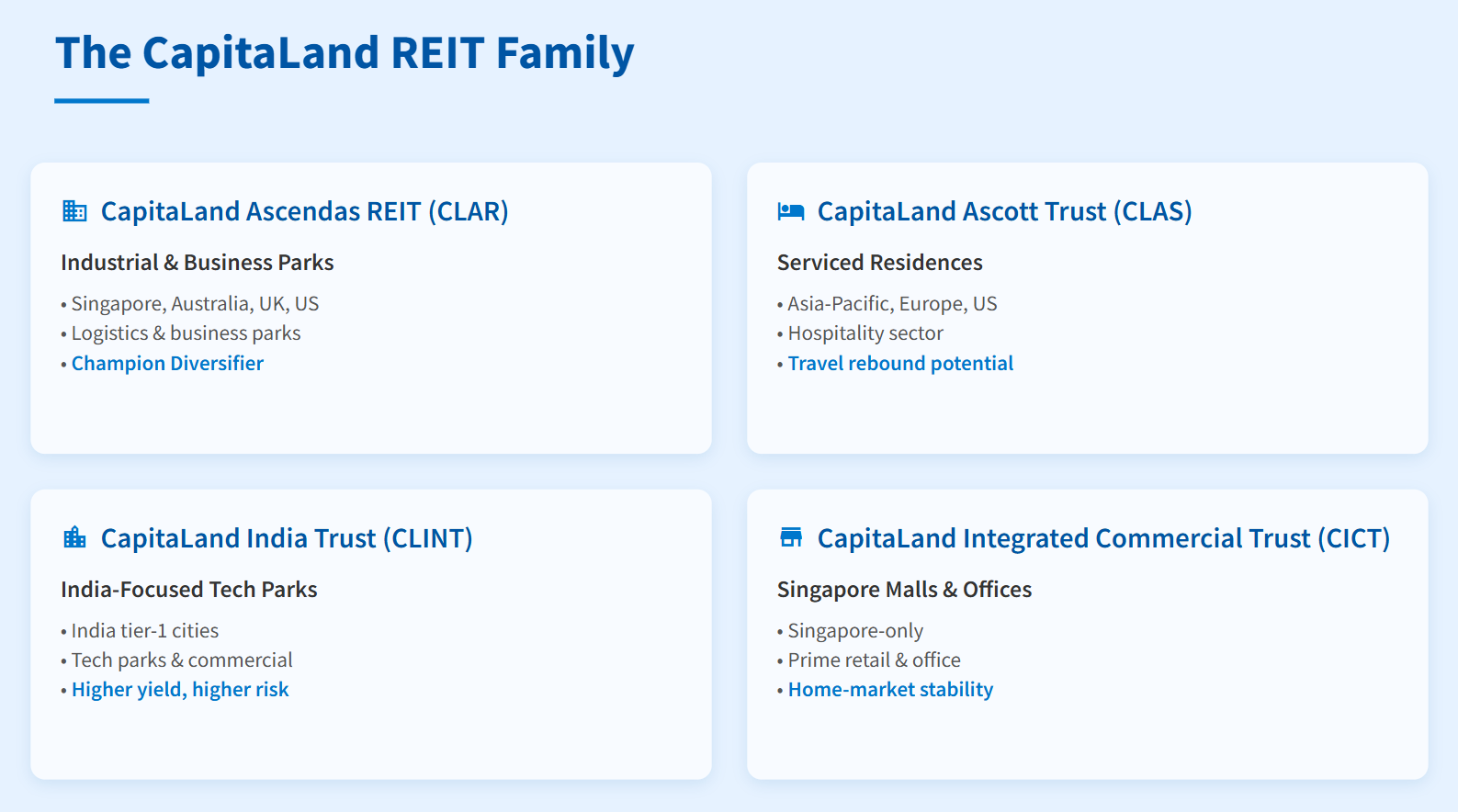

The CapitaLand REIT Family: Where Each Stands

CapitaLand now manages one of the broadest REIT portfolios in Singapore. Here are the main public-facing vehicles:

CapitaLand Ascendas REIT (CLAR): Industrial, logistics, and business parks in Singapore, Australia, UK, and US.

CapitaLand Ascott Trust (CLAS): Serviced residences, mainly in Asia-Pacific, Europe, and the US.

CapitaLand India Trust (CLINT): India-focused, mostly tech parks and commercial developments.

CapitaLand Integrated Commercial Trust (CICT): Prime Singapore malls and office assets.

Here’s Iggy’s Take: CapitaLand’s four REITs are like picking the right dish for your investment meal—each has a unique “flavour” suited to different goals. Ascendas is your reliable main course, mixing global reach and steady income. Ascott Trust adds spice with its focus on hospitality and travel, great for yield but prone to cycles. India Trust is the wild card, serving tech-driven growth and yield but with bigger currency and rate risks. Integrated Commercial Trust is the simple staple, anchored in prime Singapore malls and offices for those who crave stability above all. Know your appetite and mix wisely to build a balanced investing plate.

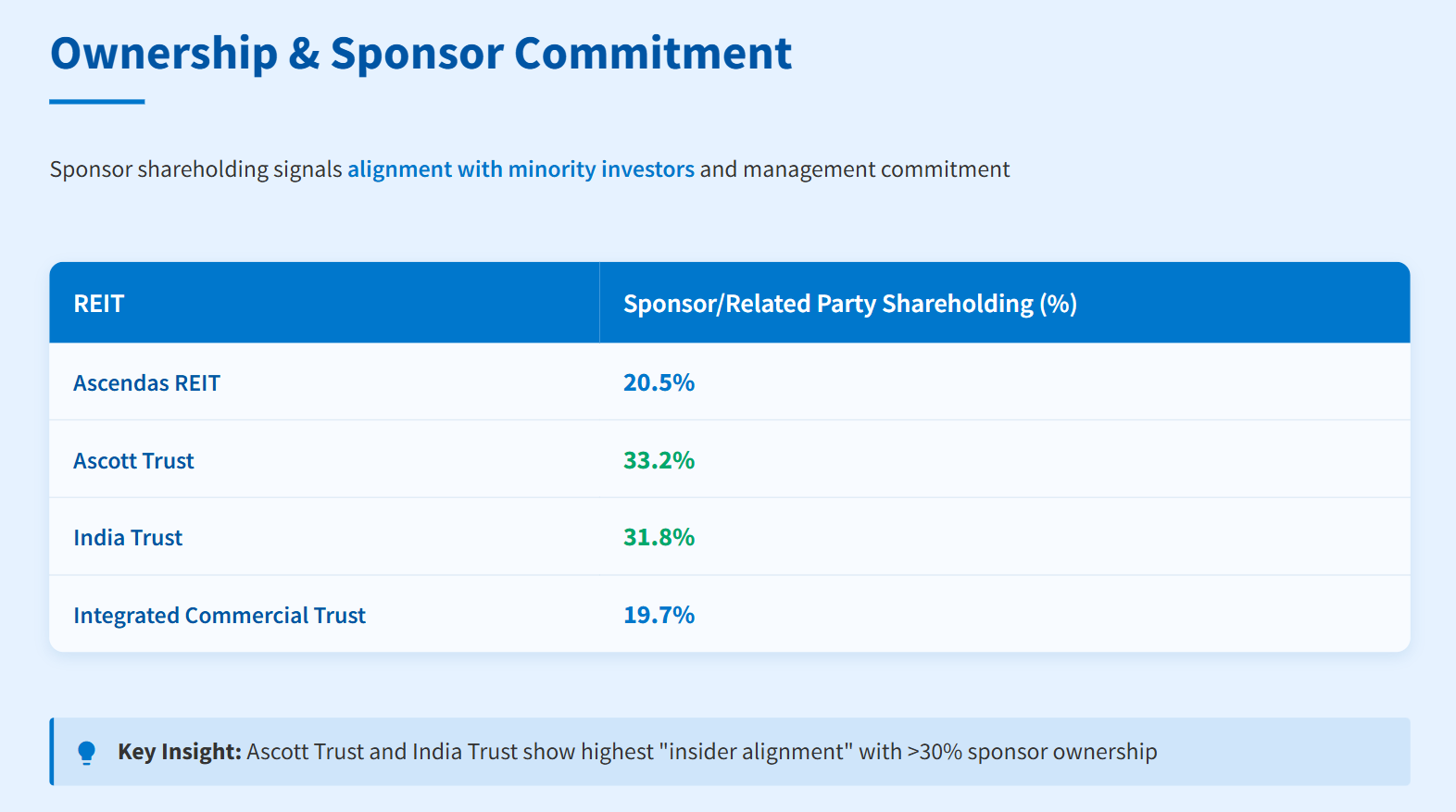

Ownership & Sponsor Commitment: Alignment or Just Branding?

Many investors overlook how much CapitaLand itself holds in its own REITs, but this is a key signal for anyone serious about risk. When the sponsor has a big stake, their interests are tied to yours—they want returns, not just management fees. High sponsor ownership usually means more proactive stewardship and attention to detail, lowering the risk of poor decisions or conflicts. It doesn’t guarantee outperformance, but when CapitaLand puts real money in, you can bet they’re looking out for the long-term health of the business rather than just branding for show. In short, strong sponsor alignment often leads to better protection and clearer focus for minority investors.

This table shows the sponsor’s (CapitaLand group or related entities) direct stake in each trust. Higher alignment typically means more proactive management and less agency risk, though it doesn’t guarantee performance. Ascott Trust and India Trust score highest for “insider alignment.”

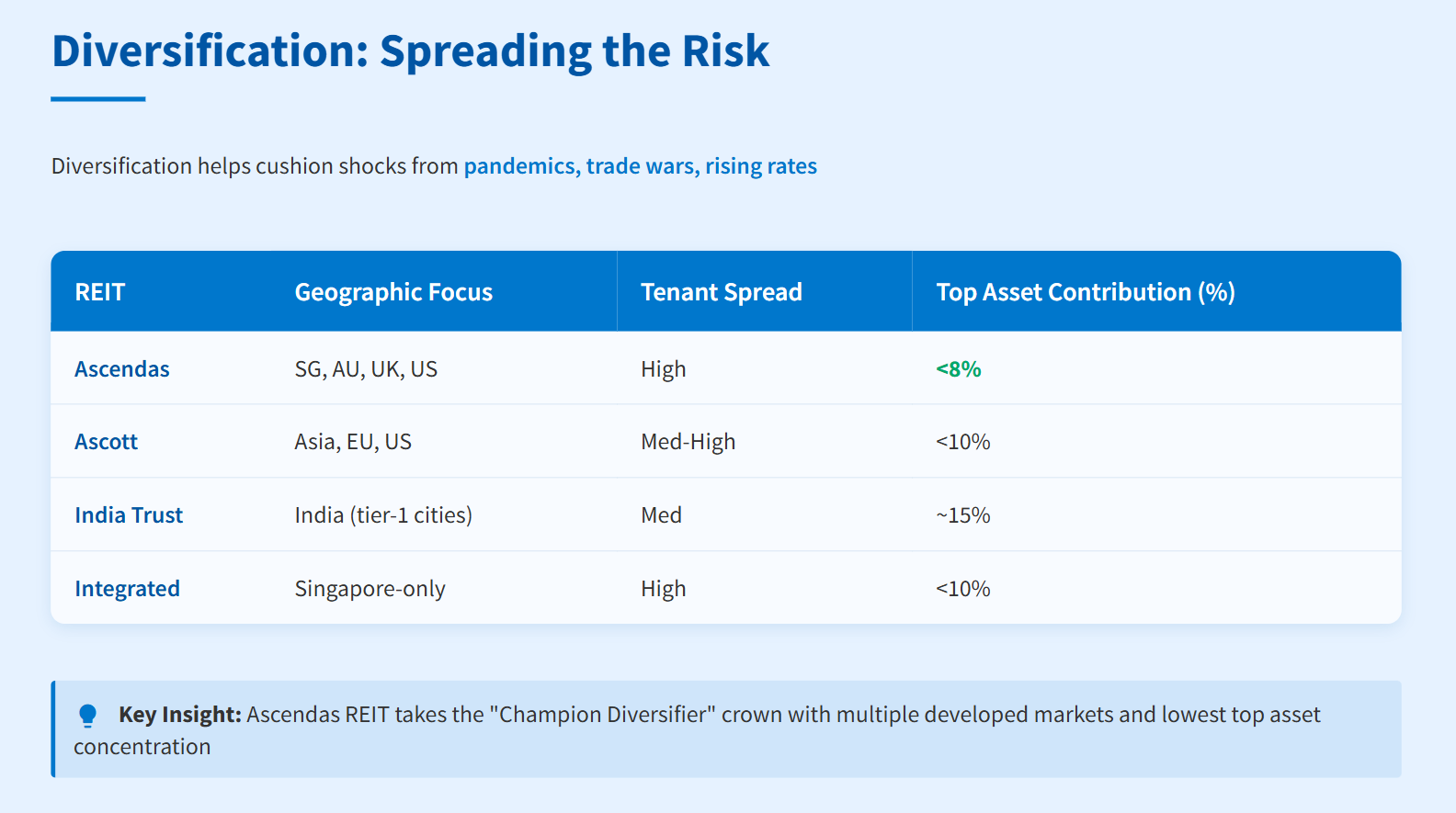

Diversification: Spreading the Risk, or Spreading Too Thin?

Growth is tempting, but it’s not the only ingredient for a strong REIT portfolio. Spreading your investments across different REITs gives you more protection when things get shaky—like during a pandemic, a trade war, or when interest rates spike. Let’s look at the four CapitaLand picks: Ascendas mixes global assets to soften blows from any one region, Ascott Trust balances hospitality risks with geographic variety, India Trust takes on India’s growth (but also its unique risks), and CICT anchors everything with stable Singapore malls and offices. By not putting all your eggs in one basket, you protect yourself against surprises and keep your income stream more reliable.

Ascendas REIT takes the “Champion Diversifier” crown, balancing multiple developed-market economies. CICT is more concentrated but offers core exposure to Singapore’s stable commercial property base.

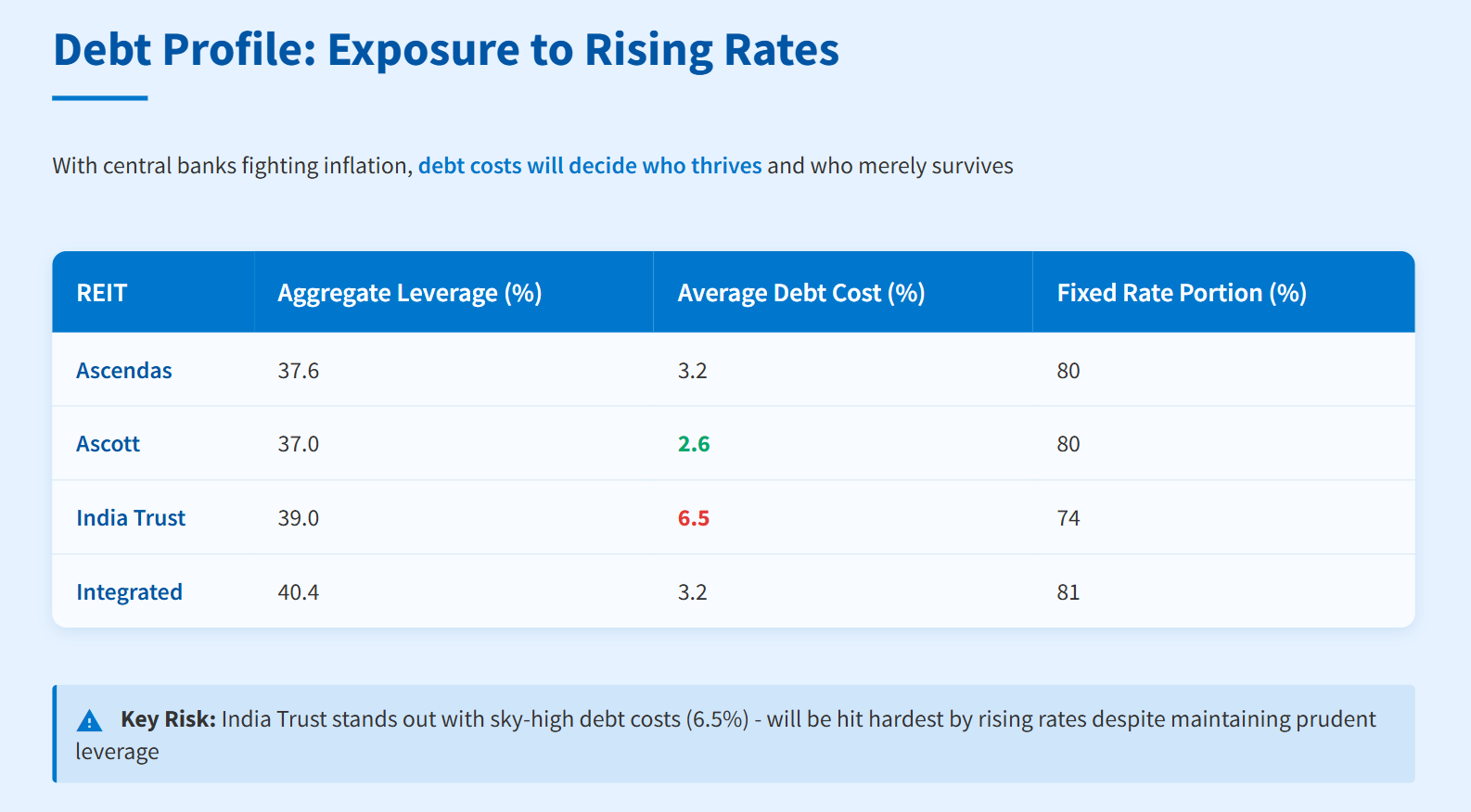

Debt Profile: Who’s Most Exposed to Rising Rates?

With central banks still fighting inflation, debt costs will decide who thrives and who merely survives. Here’s the situational awareness for each trust:

India Trust stands out for sky-high debt costs, reflecting India’s policy rates and rupee risk. Ascott Trust has a low average cost, while Ascendas and CICT sit in the mid-range with healthy fixed-rate buffers. Rising rates will hit India Trust the hardest, though all REITs maintain prudent leverage below MAS caps.

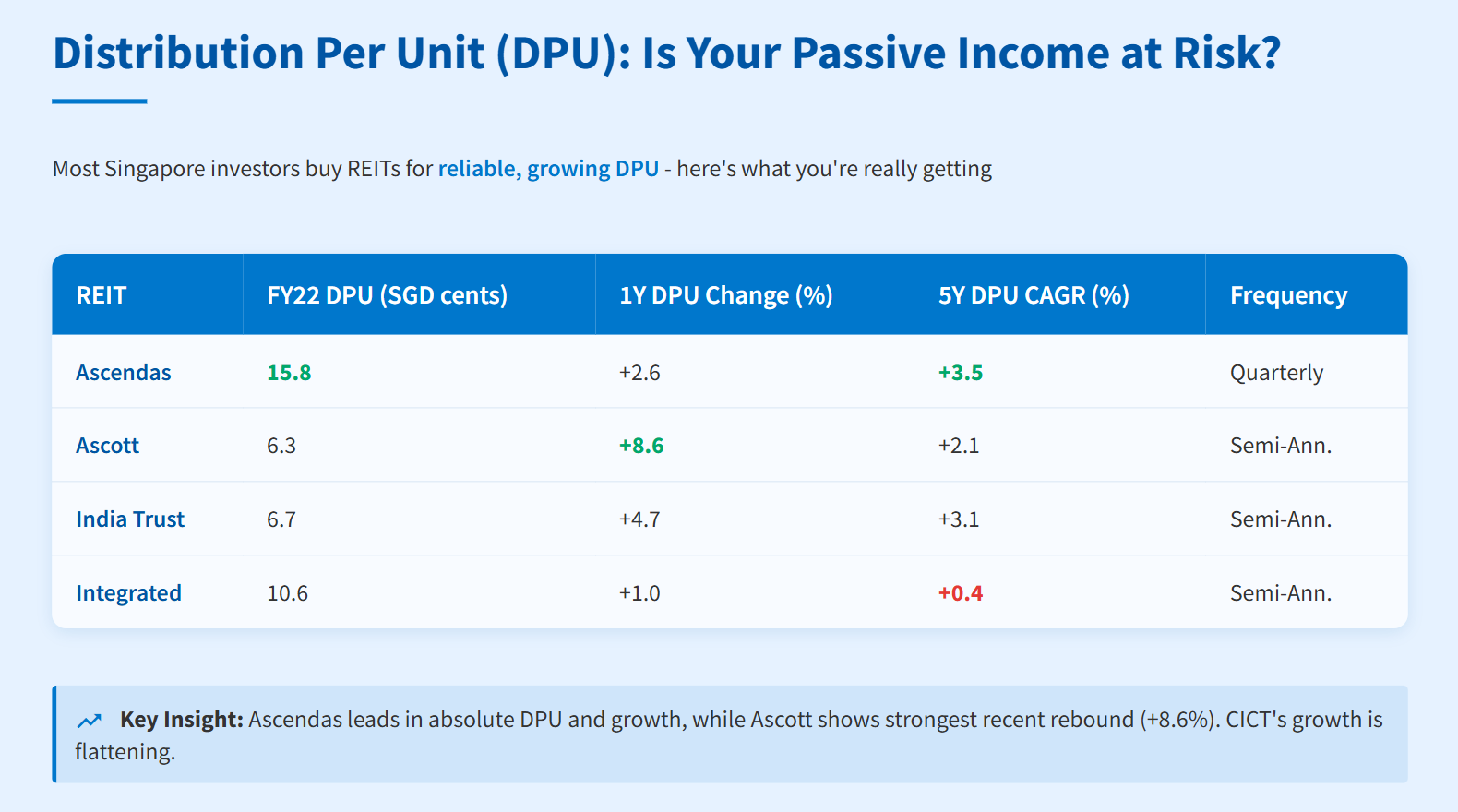

Distribution Per Unit (DPU) – Is Your Passive Income at Risk?

Let’s face it: Most Singapore investors buy REITs for reliable, growing DPU. But the truth is, income trends aren’t guaranteed. Some trusts like Ascendas have a strong track record of steady and rising distributions, while others—like CICT—offer more stability but flatter growth. Ascott Trust shines when tourism rebounds and income jumps, but its payouts swing with travel cycles. India Trust is a wild card that may boost your yield, but you’ll feel the ups and downs of rate changes and currency swings. So, when you buy for DPU, understand you’re getting a mix of trends, risks, and plenty of surprises along the way.

Ascendas leads in absolute and growth terms, while CICT’s DPU trend is much flatter—echoing retail/office sector headwinds. Ascott stands out for rebound potential; India Trust for steady mid-grade growth.

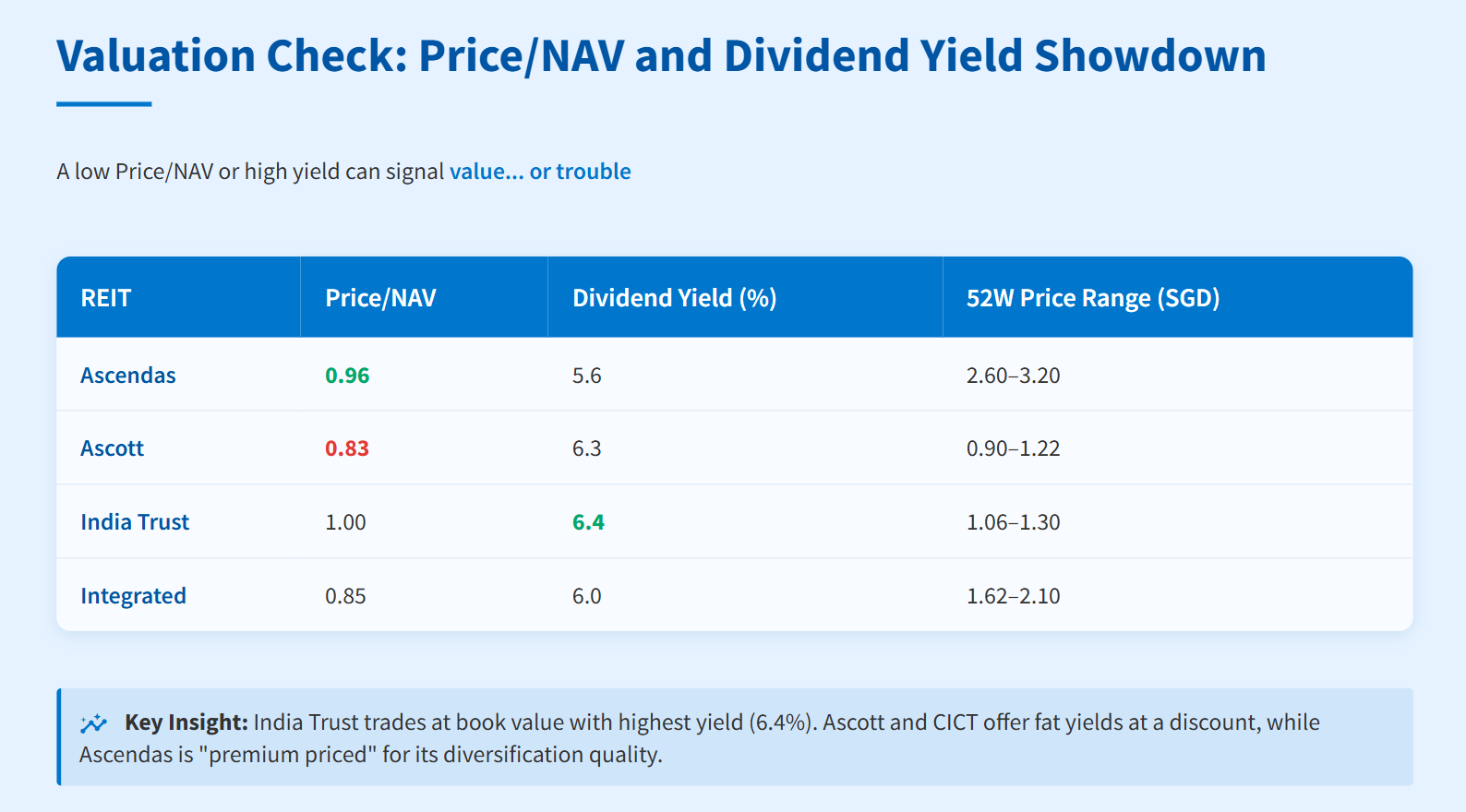

Valuation Check: Price/NAV and Dividend Yield Showdown

A low Price/NAV can mean a REIT is cheap compared to its asset value—which may look like a bargain. But sometimes cheap is cheap for a reason, like weak assets or higher risk. A high yield can also catch the eye, hinting at juicy payouts, but it might signal the market expects trouble ahead, like falling rents or rising debt costs. When looking at the current numbers, don’t just chase the lowest Price/NAV or the fattest yield—always check if the payout is sustainable and if the discount reflects real problems or just market fears. These signals can point to genuine value, but sometimes they’re red flags waving you away.

India Trust currently trades at book value with the highest yield. Ascott and CICT both offer fat yields at a discount, while Ascendas is more “premium priced” for its diversification quality.

The Iguana’s Unbiased Rankings – Who Wins in 2025?

Let’s “scorecard” the lot. Each major metric gets +1 for a top-2 spot, -1 for bottom-2.