Why 8 Out of 10 SGX Dividend Stocks Fail The CPF Retirement Test

You are earning a 4.0% guaranteed return in your CPF Special Account right now without taking a single cent of risk.

Why 8 Out of 10 SGX Dividend Stocks Fail The CPF Retirement Test

You are earning a 4.0% guaranteed return in your CPF Special Account right now without taking a single cent of risk.

I ran the ten most popular dividend stocks on the Singapore Exchange through my forensic auditing system. Only two of them actually justify the extra risk of leaving that safe haven. This is the exact math that the remaining eight companies do not want you to look at.

If you are chasing growth and momentum, a higher-risk profile may clear your hurdle. But if you are a retiree focused on wealth preservation and dependable drawdown income, my forensic standard is built to protect that. It does not accommodate a momentum trade that could derail 20 to 30 years of compounding.

My job is simple, even if the balance sheet is not. I read the numbers that the headline skips — the interest coverage, the gearing, the free cash flow sustainability — so that the Singaporean building or living off a dividend portfolio gets the same forensic clarity that institutional money takes for granted.

This piece is a lightning audit designed to clear out the noise. We are skipping the marketing brochures and looking directly at the raw balance sheets of Singapore’s favourite income counters.

In This Article:

Section 1 — The CPF sanctuary argument

Section 2 — The lightning audit

Section 3 — The two that pass

Section 4 — What to do with the eight that fail

Section 5 — The retirement portfolio implication

SECTION 1 — THE CPF SANCTUARY ARGUMENT

Let us start with a basic reality check. I call this Kopitiam Logic.

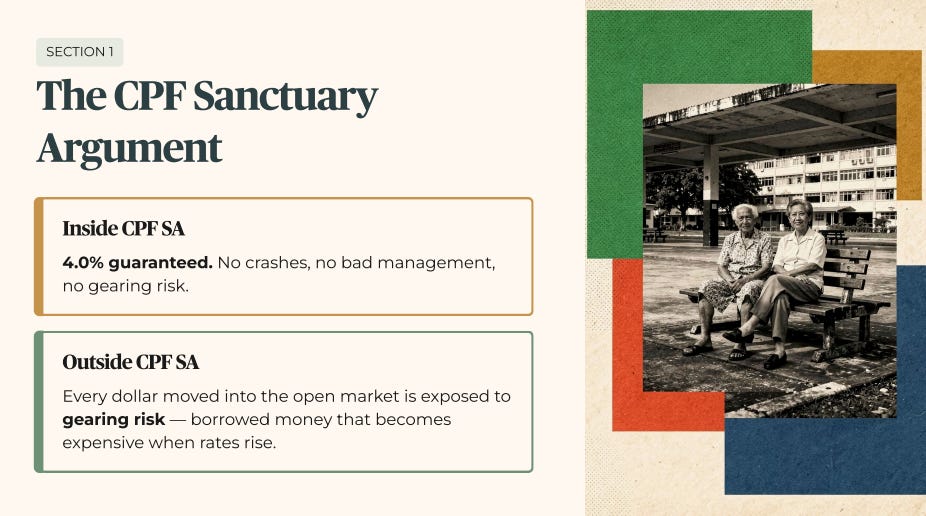

When you leave your money inside your CPF Special Account, the government guarantees you a 4.0% annual return. You do not have to worry about stock market crashes, property devaluations, or corporate management making bad business decisions. The money simply grows safely.

When you take a dollar out of that sanctuary to buy a dividend stock on the open market, you are exposing yourself to gearing risk. Gearing measures how much of a company’s assets are funded by borrowed money. If a company borrows too much when interest rates are high, that debt becomes expensive to service — and management gets forced to cut your dividend payouts just to survive.

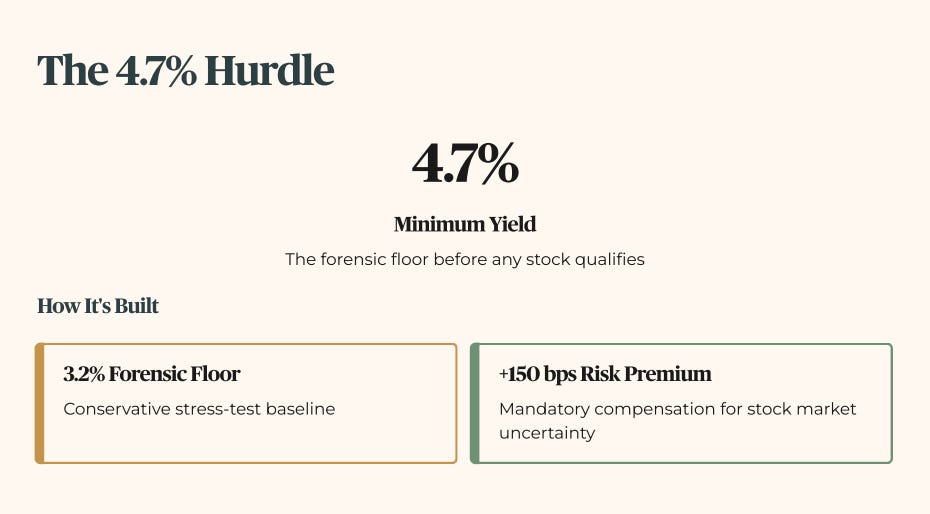

That is why my forensic framework uses a strict minimum yield hurdle of 4.7%.

Here is what that number means. It represents my 3.2% forensic floor plus a mandatory 150 basis points (each basis point is one hundredth of one percent, so 150 basis points equals 1.5%) of risk premium. A risk premium is simply the extra return you must demand to compensate you for the uncertainty of moving your money into the stock market.

If a stock cannot pay you at least 4.7%, it fails the retirement test immediately. You would be taking on stock market volatility for a return that barely beats a risk-free government account.

🦎 Iggy’s Insight

The mathematical reality of retirement investing in Singapore comes down to a very simple spread calculation.

If you move your hard-earned cash from a guaranteed 4.0% CPF Special Account into an SGX dividend stock yielding 4.55%, you are exposing your capital to debt refinancing shocks and management mistakes. What do you get in return? An extra return of just 55 basis points — just over half a percent.

That is a microscopic premium for an enormous amount of balance sheet risk.

When the storm hits the open market, that extra half a percent will not save your portfolio from capital loss. Protect the foundation first.

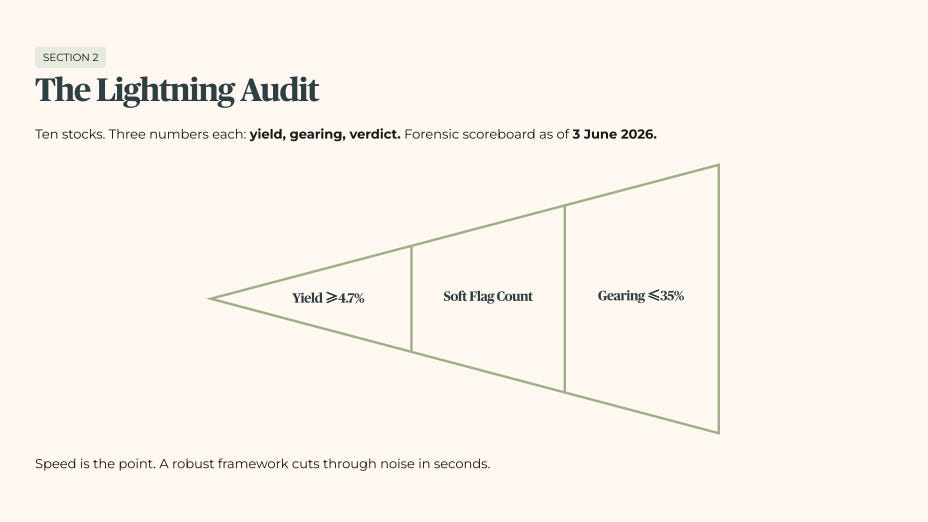

SECTION 2 — THE LIGHTNING AUDIT

We are now going to run our ten stocks through the forensic screen. We will look at three numbers for each: the current yield, the gearing ratio, and the final zone verdict.

The speed is the entire point here. I want you to see exactly how quickly a robust framework can cut through the noise.

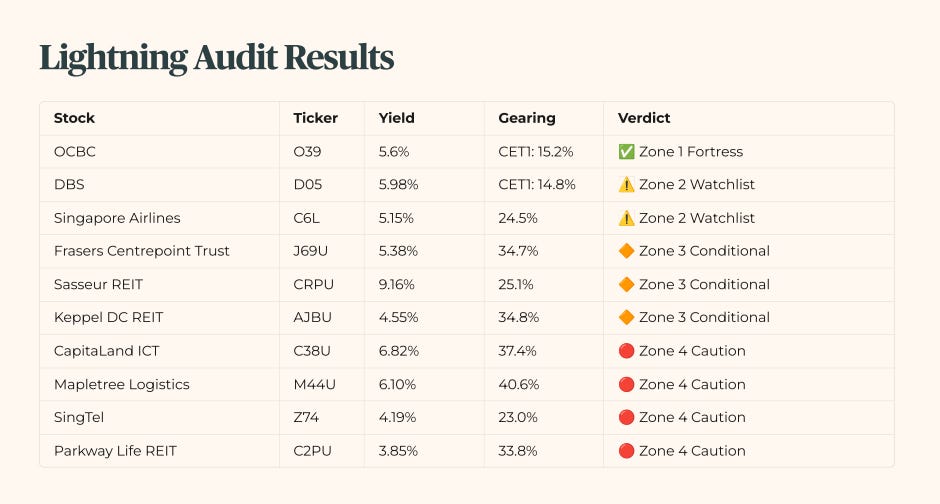

This is the forensic scoreboard as of 3 June 2026.

Table 1 — Lightning Audit Results

Note on OCBC yield: The 5.6% figure is the trailing total yield including a special dividend. The forward ordinary yield is 3.45%. Zone 1 is assigned on the trailing total basis, which is the relevant figure for a retirement income screen that tracks actual cash received. Forward yield should be monitored at the next earnings cycle.

Note on SingTel gearing: The 23.0% figure is derived from total long-term debt against total assets. If IFRS 16 lease liabilities are included, the adjusted figure would be higher. Verify against the FY2026 annual report before treating this as the definitive gearing figure. SingTel’s Zone 4 verdict is based on yield grounds, not gearing.

Let us look at why these numbers landed where they did.

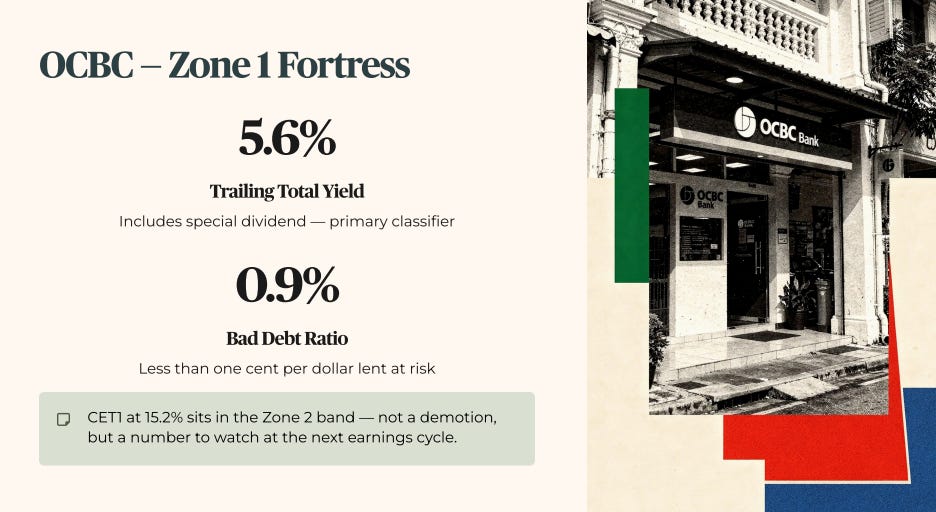

OCBC takes the only Zone 1 Fortress spot. Its trailing total yield sits at 5.6%, including the special dividend paid to shareholders this cycle. Its Core Equity Tier 1 (CET1) ratio — the financial buffer banks hold to absorb unexpected losses — stands at 15.2%.

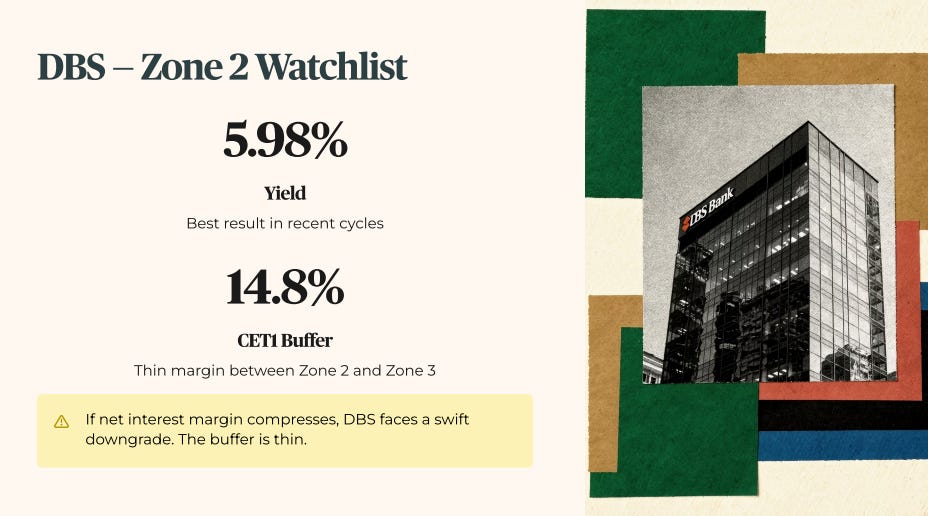

DBS lands in Zone 2 Watchlist as a narrow passer. Its yield comes in at 5.98%. But its financial buffer is thinner at 14.8%. Any major share buybacks will put pressure on its balance sheet, which is why it sits under active review rather than cleared for the fortress tier.

Singapore Airlines also holds a Zone 2 spot. Its 5.15% yield clears the hurdle. But it carries a soft flag for net profit compression — its bottom-line earnings are beginning to shrink.

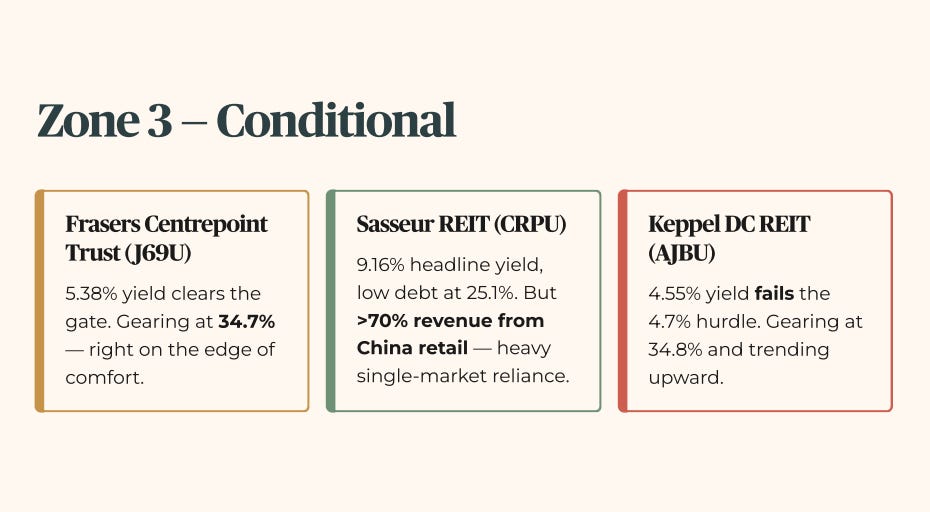

Moving into Zone 3 Conditional.

Frasers Centrepoint Trust clears the gates with a 5.38% yield. But its debt load has crept up to 34.7%. That sits right on the edge of my comfort zone.

Sasseur REIT shows a massive headline yield of 9.16% and low debt at 25.1%. But it triggers three separate soft flags. The biggest one? More than 70% of its revenue comes from retail assets in China. That is heavy reliance on a single market.

Keppel DC REIT falls into Zone 3 because its 4.55% yield fails to clear my 4.7% mandatory hurdle — the minimum return I require before any stock qualifies for a retirement portfolio. Its gearing sits at 34.8%, just inside the ceiling, but trending upward.

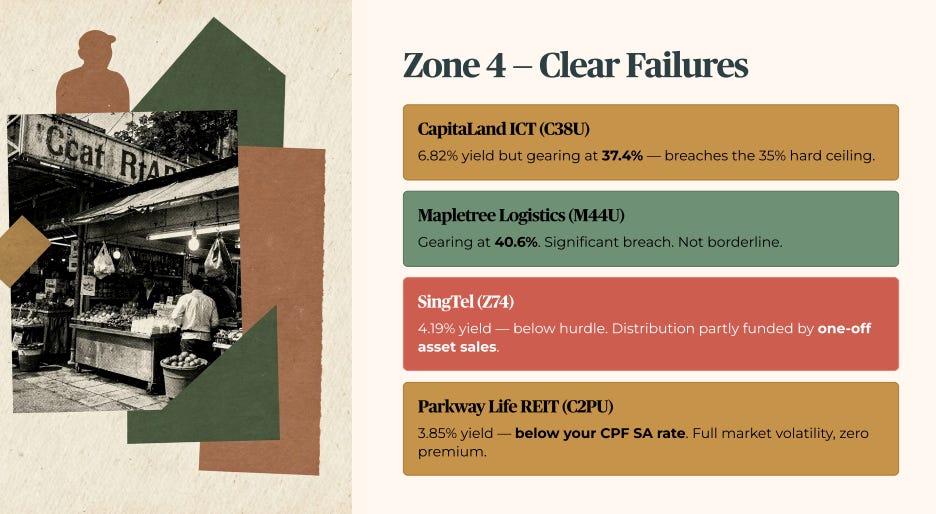

Now we hit the clear failures in Zone 4 Caution.

CapitaLand Integrated Commercial Trust is paying 6.82%. But its gearing is a bloated 37.4%. That means it has breached my hard safety ceiling of 35% — for every $100 of assets it holds, $37.40 is funded by borrowed money.

Mapletree Logistics Trust has now been verified: its gearing sits at 40.6%. That is not a borderline number. It is a significant breach of the 35% ceiling and firmly supports the Zone 4 verdict.

SingTel fails completely. It has a 4.19% yield, which falls below the 4.7% hurdle. And a large portion of that distribution is funded by one-off asset sales rather than recurring business profits.

Parkway Life REIT fails the test because its 3.85% yield actually pays you less than your guaranteed CPF Special Account — and you are exposed to full stock market volatility at the same time.

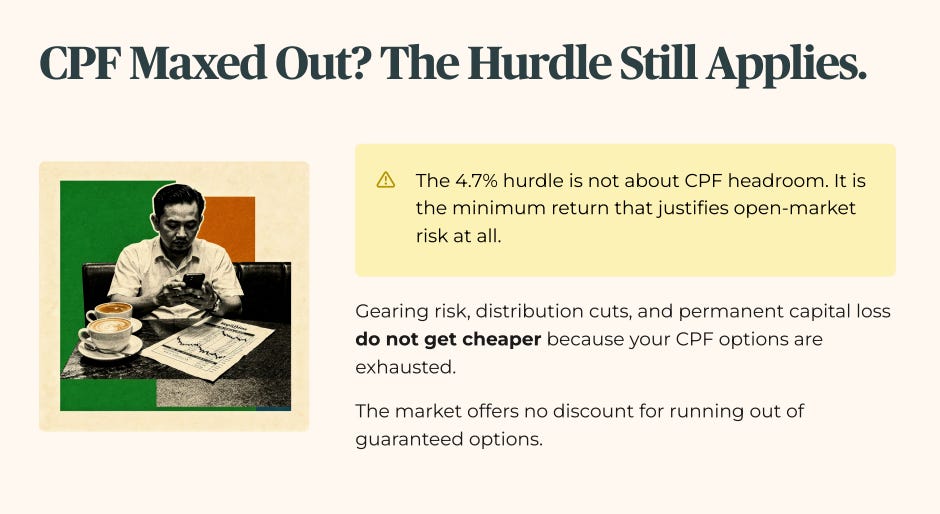

A common question worth addressing directly.

If CPF SA is already maxed out, why does the 4.7% yield hurdle still apply to the dollars sitting outside the CPF system?

The answer is that the hurdle has nothing to do with what CPF will or will not pay you. It is the minimum return that justifies the risks you are taking on by being in the open market at all. Those risks are gearing risk, distribution cuts, and the possibility of permanent capital loss.

Those risks do not get cheaper because your CPF headroom is exhausted. The market does not offer you a discount for running out of guaranteed options.

The Zone 4 verdict here is not a permanent rejection. It is a forensic timing signal. At the current yield and price, this stock is not compensating you adequately for the risk you would be taking on. That changes when the yield clears the hurdle, when the balance sheet strengthens, or when the price corrects to a level where the math works. When any of those conditions are met, Iggy will say so. Until then, the framework holds. The framework exists precisely for the moments when there is pressure to compromise it.

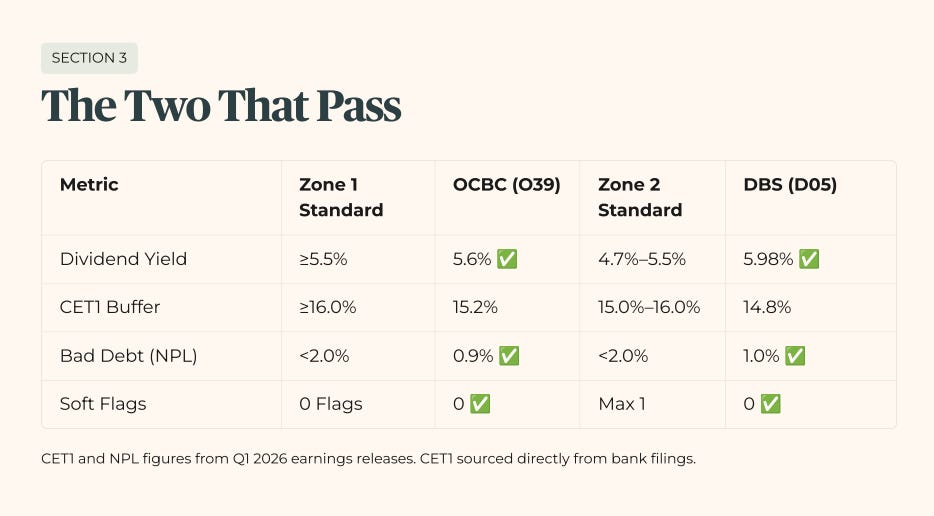

SECTION 3 — THE TWO THAT PASS

Let us zoom in on what true forensic strength looks like by comparing our top two banking entities. When a company passes the hurdle properly, its income streams are backed by an elite fortress balance sheet.

Table 2 — What Passing The Hurdle Actually Looks Like

CET1 and NPL figures sourced from Q1 2026 earnings releases. CET1 is a regulatory capital disclosure and is not available via market data APIs — these figures are taken directly from bank filings.

OCBC clears the Zone 1 yield requirement on a trailing total basis at 5.6%. It maintains a clean bad debt ratio of just 0.9% — less than one cent in every dollar lent is at risk of default. One note worth flagging: OCBC’s CET1 of 15.2% sits in the Zone 2 CET1 band (15.0% to 16.0%) even while its yield earns Zone 1. This is not a demotion — the yield gate is the primary classifier — but it is a number to watch at the next earnings cycle.

DBS performs strongly on yield at 5.98%, its best result in recent cycles. But its financial buffer sits at 14.8%. Its net interest margin — the difference between the interest the bank earns on loans and the interest it pays out on deposits, which is the core measure of bank profitability — if that margin compresses, DBS faces a swift downgrade. The buffer between Zone 2 and Zone 3 is thin.

The yield and CET1 spread between OCBC and DBS clears the 4.7% hurdle on paper — but the next section’s one-page fortress test is where this CPF retirement verdict is actually decided.