Why Are 4 SGX REITs Failing Gearing Tests Now | SGX Daily Pulse 24 Apr 2026 | 🦖EP1570

When CICT, Suntec, FCT, and CLINT all breach the 35% gearing ceiling as T-bill sits at 1.40%

EP1570 | 24 April 2026 | Daily Pulse

THE MACRO PICTURE

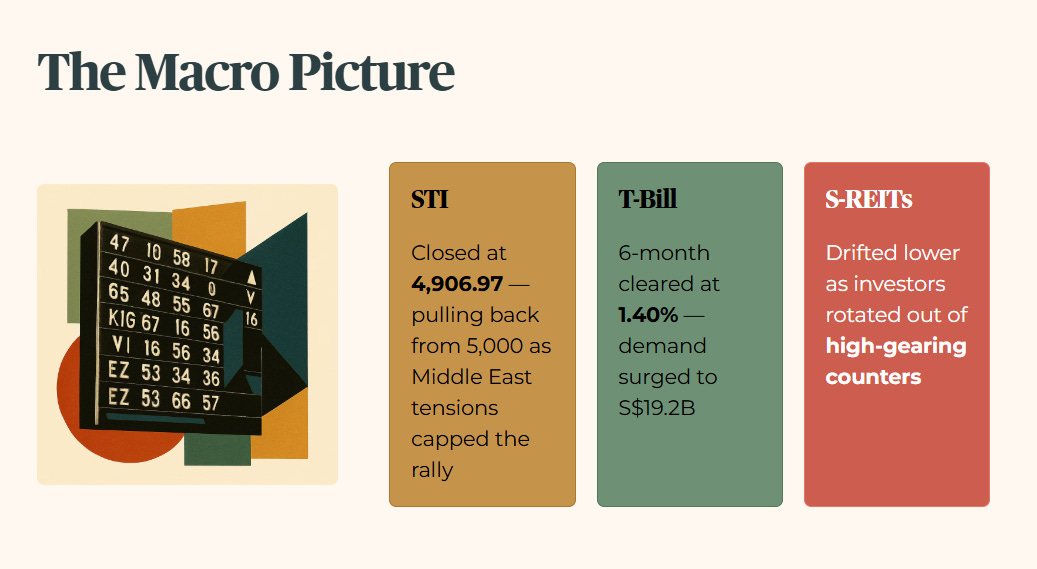

The STI closed at 4,906.97, pulling further back from the 5,000 psychological handle as Middle East tensions capped the week’s attempted rally. The 6-month T-bill cleared at 1.40% after demand surged to S$19.2B — retail investors voting with their feet for the risk-free sanctuary. The S-REIT sector drifted lower as yield-hungry investors rotated out of high-gearing counters. Local short-term rates remain stable for now, providing a temporary breather for mortgage-heavy REITs, but that floor is not guaranteed.

In this article:

The macro picture

The audit

ST Engineering (S63) — Yield trap

CapitaLand Integrated Commercial Trust (CICT / C38U) — Gearing alert

CapitaLand Investment (CLI / 9CI)

Suntec REIT (T82U) — Gearing alert | ICR alert

Sheng Siong (OV8) — Yield trap

Frasers Centrepoint Trust (FCT / J69U) — Gearing alert

CapitaLand India Trust (CLINT / CY6U) — Gearing alert

ESR-LOGOS REIT (J91U) — Occupancy alert

PropNex (O9G)

iFAST (AIY) — Yield trap

🦎 Iggy’s insight — Suntec REIT

🦎 Iggy’s insight — CICT

Analyst chatter

Watchlist yield spread (T-bill: 1.40%)

Iggy’s take — The bottom line

Iggy’s forensic disclaimer

THE AUDIT

1. ST Engineering (S63) — YIELD TRAP

“The Middle East revenue shield is holding, but the dividend math has hit the forensic floor.”

CEO Vincent Chong confirmed at the FY2025 AGM that Middle East revenue is below 3% of group income and the regional conflict impact is “not material.” That is the good news. The bad news is a 1.54% yield against a 4.7% forensic hurdle — a failure by 316 basis points. The 3-year average yield sits around 3.5%, so the current reading is not just below the hurdle, it is below the stock’s own historical norm.

Peer SIA Engineering (S59) offers 3.01%, which is technically higher but also fails the 4.7% hurdle — neither counter qualifies as a sanctuary asset on yield alone. For a 60-year-old retiree in Jurong managing an SRS drawdown, the 1.54% yield represents a S$2,460 annual income gap per S$100k capital against the 4.0% CPF SA sanctuary benchmark. The spread against the 1.40% T-bill is a mere 14 basis points. You are taking equity risk for almost nothing.

Forensic Stance: Yield Trap.

2. CapitaLand Integrated Commercial Trust (CICT / C38U) — GEARING ALERT

“NPI growth is a shiny distraction from a balance sheet nearing the 40% danger zone.”

CICT posted a 7.9% rise in NPI driven by the CapitaSpring acquisition and Gallileo (Germany) contributions. The occupancy at 95.2% clears the 95% prime asset threshold. Those are the positives. The problem is gearing at 38.5%, which breaches the 35% forensic ceiling. Suntec REIT sits at 41.6%, making CICT look conservative by comparison — but that is a dangerous relative-value comparison when both counters are above the ceiling. A 10% valuation write-down on German assets, a plausible scenario given the Eurozone slowdown, would push gearing toward 42% and trigger a mandatory deleveraging event. A 55-year-old PMET in Toa Payoh sees a S$314M NPI headline but faces a potential 5% DPU dilution if CICT is forced into an equity fund raise to cool the balance sheet.

Forensic Stance: Watchlist Trigger.

3. CapitaLand Investment (CLI / 9CI)

“Mandate wins keep the AUM lights on, but retail yield remains a secondary thought.”

CLI secured a S$2.4B real estate mandate to manage Income Insurance, bringing total deal momentum to S$12.1B over 16 months. The institutional story is compelling. The retail income story is not. At a TTM yield of 4.23% (TTM dividend S$0.12 / last done S$2.84), CLI clears the 4.7% hurdle for the first time in recent memory — but only just, and on a trailing basis. For a 50-year-old in Yishun, the mandate news stabilises the fee income base without doing anything material to immediate distribution income. Monitor, but do not treat the AUM win as a yield catalyst.

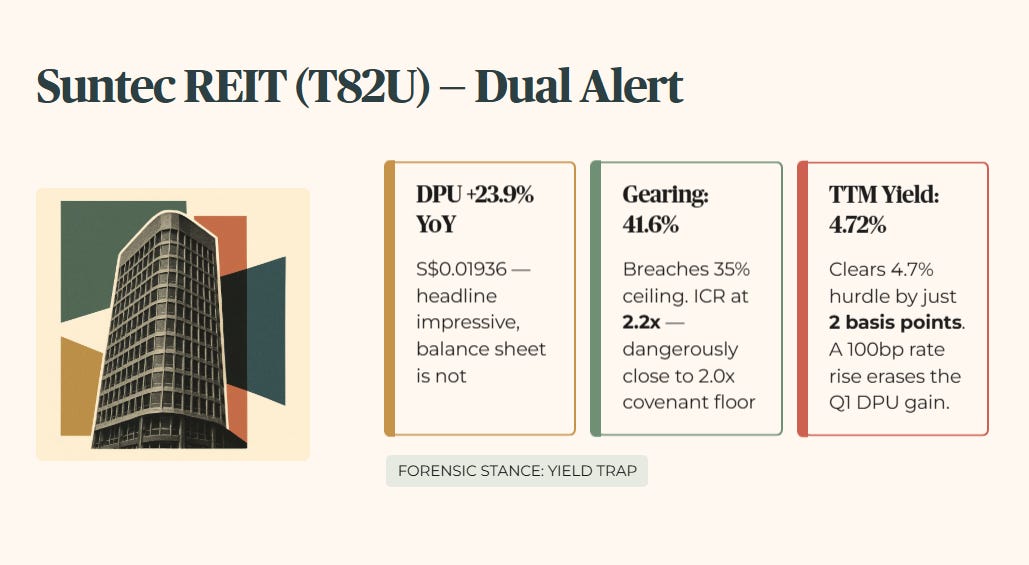

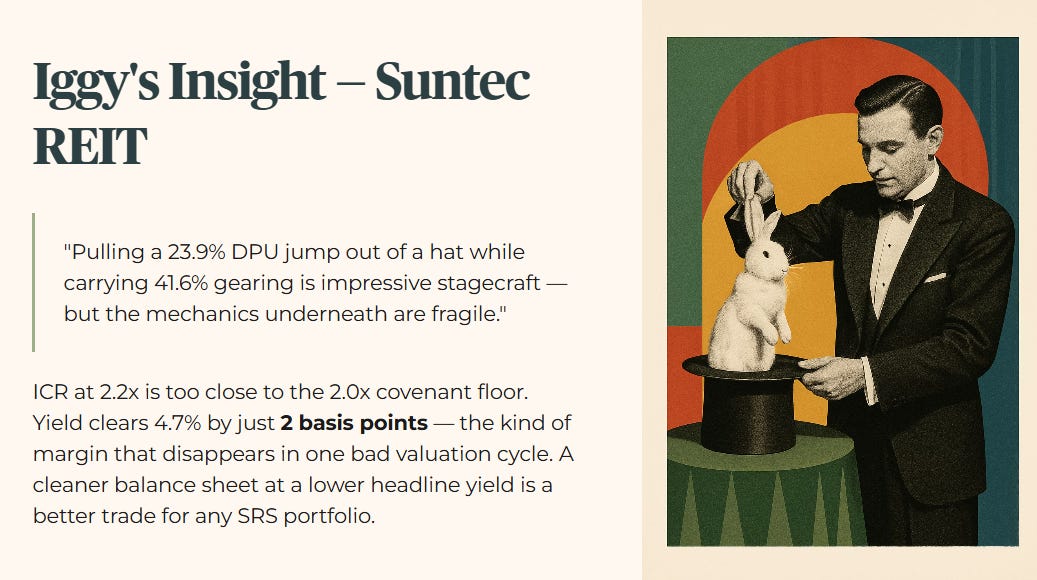

4. Suntec REIT (T82U) — GEARING ALERT | ICR ALERT

“Record DPU growth is being funded by a leverage level that has zero margin for error.”

DPU surged 23.9% despite a decline in UK income from The Minster Building. The headline number is attention-grabbing. The balance sheet underneath it is not. Gearing at 41.6% and an ICR of 2.2x are simultaneous breaches of the 35% forensic ceiling and the 4x ICR floor. The ICR of 2.2x sits uncomfortably close to the 2.0x covenant danger zone. A 100bp rise in financing costs would slash DPU by approximately 1.75 cents, effectively erasing the current Q1 gain in a single rate move. Peer Mapletree Pan Asia Commercial Trust carries a materially higher ICR, indicating Suntec is the more extended player in this space. The TTM yield of 4.72% clears the 4.7% hurdle by 2 basis points — the thinnest possible margin. The T-bill spread is 3.32%. A 55-year-old PMET in Bedok holding Suntec for SRS income is betting on Singapore office rent reversion staying at +9.5% indefinitely.

Forensic Stance: Yield Trap.

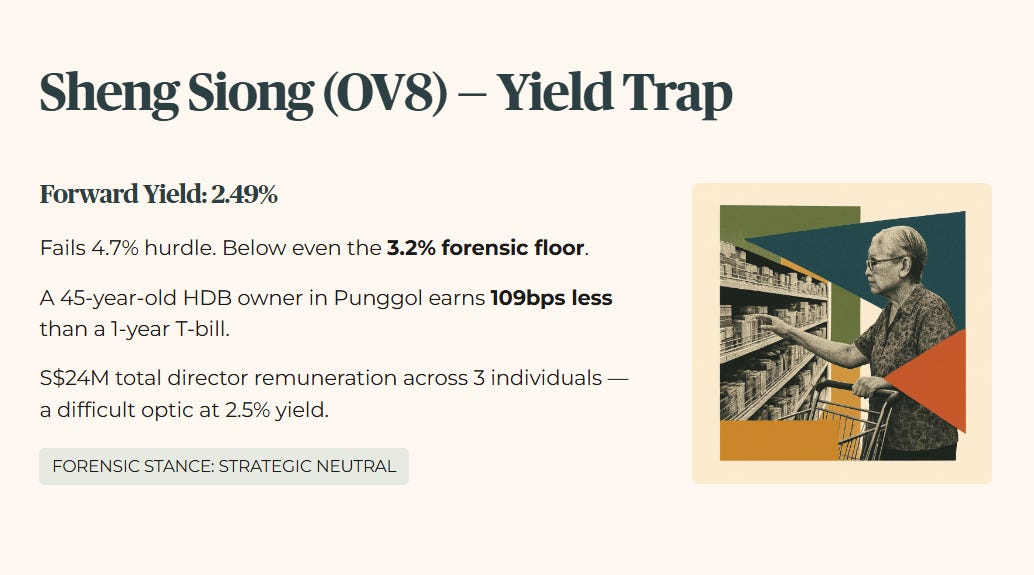

5. Sheng Siong (OV8) — YIELD TRAP

“Margins are protected by the heartland, but the dividend is not paying the bills.”

Management confirmed margin improvement headroom at the AGM but flagged upward pressure on costs from Middle East supply chain friction. The 2.49% yield fails the 4.7% hurdle and sits below even the 3.2% forensic floor. Peer Dairy Farm International (D01) offers 3.32% — also below the hurdle, but at least above the forensic floor. A 10% sustained increase in energy prices would further compress Sheng Siong’s margins or force price hikes that dampen heartland volume. A 45-year-old HDB owner in Punggol using dividends to supplement salary income is currently earning 109 basis points less than a 1-year T-bill. The S$24M total director remuneration across three individuals is a difficult optic when the retail yield sits at 2.5%.

Forensic Stance: Strategic Neutral.

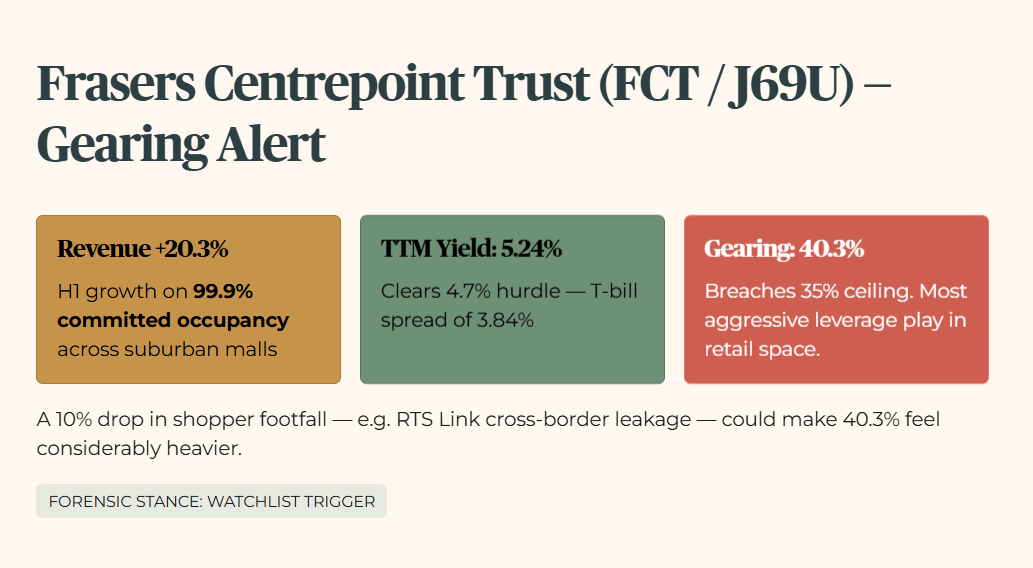

6. Frasers Centrepoint Trust (FCT / J69U) — GEARING ALERT

“Suburban retail is the necessity sanctuary, but the leverage ceiling has been broken.”

H1 revenue climbed 20.3% supported by 99.9% committed occupancy across suburban malls — a genuinely impressive operational result. The TTM yield of 5.24% clears the 4.7% hurdle with a 3.84% T-bill spread. The problem is gearing at 40.3%, which breaches the 35% ceiling. CICT at 38.5% has slightly more debt headroom, making FCT the more aggressive leverage play in the retail space. A 10% drop in shopper footfall — a scenario where the RTS Link accelerates cross-border retail leakage — could pressure rents and make that 40.3% feel considerably heavier. A 65-year-old drawing CPF LIFE in Tampines enjoys the DPU stability today but faces potential capital loss if FCT needs to divest assets at a discount to repair the balance sheet.

Forensic Stance: Watchlist Trigger.

7. CapitaLand India Trust (CLINT / CY6U) — GEARING ALERT

“Indian growth is real. The Singapore dollar translation is the forensic leak.”

The underlying asset performance in rupee terms is genuinely solid at +8.0%. The SGD translation wiped that out entirely, producing a 3.0% decline in Singapore dollar property income. Gearing at 39.6% is well above the 35% ceiling, adding balance sheet risk to what is already a currency-exposed structure. A further 10% depreciation of the rupee — a credible scenario in any EM capital flight episode — would produce a DPU cut regardless of how well the physical assets perform. Management’s push to onshore debt is the right structural move, but it does not change the SGD math today. A 50-year-old in Ang Mo Kio managing SRS and CPF SA is witnessing growth that cannot be spent at the Bedok wet market.

Forensic Stance: Watchlist Trigger.

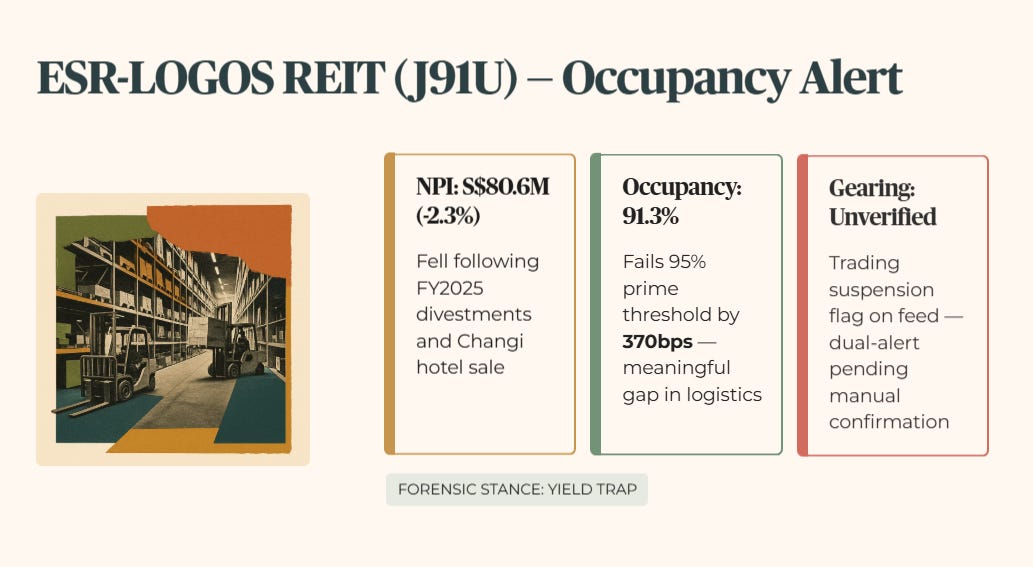

8. ESR-LOGOS REIT (J91U) — OCCUPANCY ALERT

“Divestments are pruning the portfolio, but the organic core is still wilting.”

NPI fell 2.3% following FY2025 divestments and a hotel sale in Changi. Occupancy at 91.3% fails the 95% prime asset threshold by 370 basis points — a meaningful gap in a logistics market where prime assets should be near full. Peer CapitaLand Ascendas REIT (CLAR) maintains higher occupancy and a more diversified global logistics base. Same-store revenue growth of 1.4% is fragile: any global trade slowdown reversal would accelerate the NPI decline. Gearing is unverified due to a current trading suspension flag on the Longbridge feed — dual-alert classification is held pending manual confirmation. A 50-year-old investor in Clementi holding this for industrial resilience is witnessing a portfolio contraction, not consolidation.

Forensic Stance: Yield Trap. (Gearing alert status pending verification.)

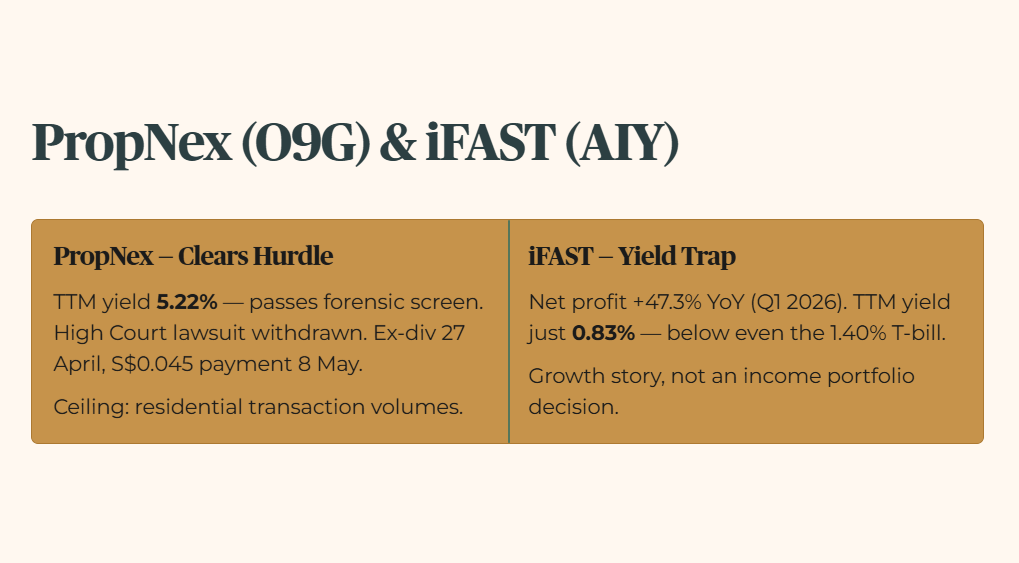

9. PropNex (O9G)

“Legal clouds clear, but the residential volume ceiling remains the real trial.”

The High Court lawsuit against subsidiary PRL was withdrawn — claimants had sought S$586k for alleged breach of duty. The legal overhang is gone. The TTM yield of 5.22% (annualised payout S$0.095) clears the 4.7% forensic hurdle. Shareholders should note the upcoming ex-dividend date of 27 April — two days from now — with a S$0.045 payment following on 8 May. For a 50-year-old in Bukit Timah, the yield passes the forensic screen, but residential transaction volumes remain the structural ceiling on earnings.

10. iFAST (AIY) — YIELD TRAP

“Hong Kong profits are soaring. The dividend remains an institutional afterthought.”

MetricValueNet Profit (Q1 2026)S$28M (+47.3% YoY)TTM Yield0.83%

Net profit jumped 47.3% on the back of the ePension business in Hong Kong. The yield sits at 0.83% (TTM dividend S$0.075 / last done S$9.04) — a failure against the 4.7% hurdle by 387 basis points, and below even the 1.40% risk-free T-bill. A 10% slowdown in Hong Kong digital adoption, the most plausible geopolitical friction scenario, would dent the profit trajectory significantly. A 55-year-old in Woodlands holding iFAST for SRS income is forgoing immediate cash flow for a growth story. That is a valid trade — but it is not an income portfolio decision.

Forensic Stance: Yield Trap.

🦎 Iggy’s Insight — Suntec REIT

Suntec is the Houdini of the SGX REIT sector right now. Pulling a 23.9% DPU jump out of a hat while carrying 41.6% gearing is impressive stagecraft, but the mechanics underneath are fragile. The UK portfolio is showing cracks, the ICR at 2.2x is too close to the 2.0x covenant floor for comfort, and the TTM yield of 4.72% clears the 4.7% hurdle by two basis points — the kind of margin that disappears with one bad valuation cycle. If you are chasing this yield, you are speculating on Singapore office rent reversion staying elevated indefinitely. A cleaner balance sheet at a lower headline yield is a better trade for any SRS portfolio.

🦎 Iggy’s Insight — CICT

The market is cheering the NPI jump. I am watching the debt pile. CICT is running a 38.5% gearing bar at the exact moment global interest rates are stress-testing every leveraged structure on the SGX. Yes, the asset enhancement at Plaza Singapura is smart, and the occupancy at 95.2% is genuine quality. But the German exposure at a time of Eurozone slowdown is not a minor footnote — a 10% valuation write-down takes gearing to 42% and forces a capital event. The NPI headline is real. The balance sheet headroom is not.

ANALYST CHATTER

Brokers are maintaining buy calls on CLI following the Income Insurance mandate. The mandate adds AUM and stabilises fee income, but CLI’s TTM yield of 4.23% clears the 4.7% hurdle on a trailing basis only — forward distribution visibility is the test. DBS remains positive on CICT and Suntec, citing high office rent reversions. The forensic read is different: rent reversion momentum does not neutralise a 35% gearing breach. Both counters are above the ceiling. Rent reversion needs to outpace leverage cost simultaneously and consistently for that thesis to hold.

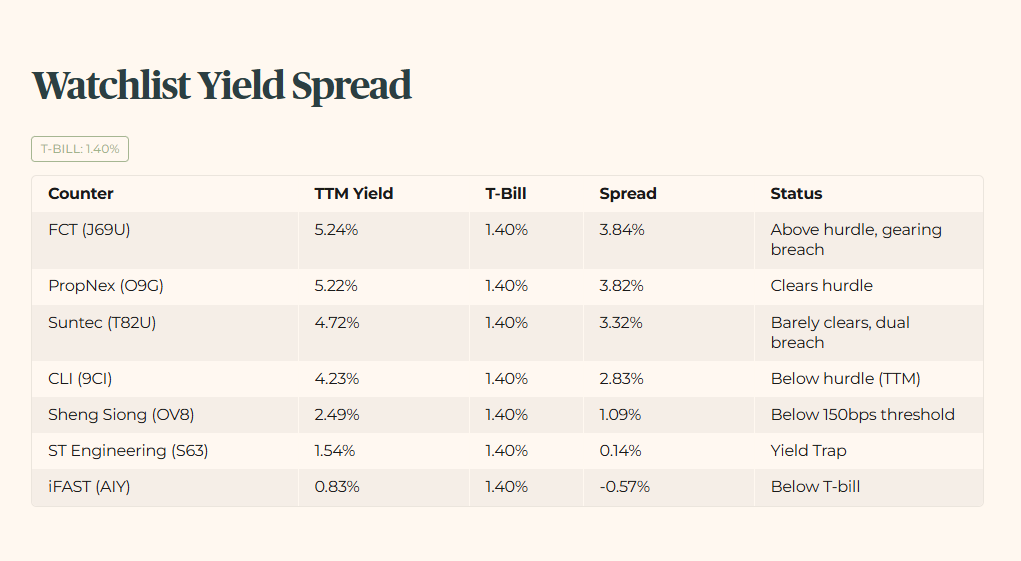

WATCHLIST YIELD SPREAD (T-Bill: 1.40%)

Stress-Test Note: The T-bill sits at 1.40% today. The forensic floor holds at 3.2% regardless. I audit for the rate environment that returns — not the one we are currently enjoying. The 4.7% minimum yield hurdle does not move with the T-bill.

The Window Is Already Open

The Window Closes Fast. In this market, the difference between a “Sanctuary” and a “Yield Trap” is decided in a single trading session. By the time this analysis reaches you as a free subscriber, the entry window Iggy identified has already opened — and often closed.

Iggy’s Elite Investors don’t just get the report earlier. They get it when the numbers still matter — zero-day forensic breakdowns, the full “Red Zone” watchlist, and institutional-grade cheatsheets at the moment the setup is live, not after the market has already priced it in.

For S$9/month — less than a kopi and kaya toast set at Raffles Place — you stop being the Exit Liquidity and start being the Analyst.

IGGY’S TAKE — THE BOTTOM LINE

The Iran trigger has not just moved oil. It has exposed how thin the margin of safety is across SGX’s leveraged REIT sector. Four counters in today’s audit — CICT, Suntec, FCT, CLINT — are simultaneously above the 35% gearing ceiling and facing macro conditions that punish leverage. The DPU growth headlines on Suntec and FCT are real. The balance sheets generating them are fragile.

For any REIT in today’s audit carrying gearing above 35%: the question is not whether the yield clears 4.7%. The question is whether a single valuation cycle, a single rate move, or a single capital raise wipes out two years of distributions. On that test, I would rather sit in PropNex at 5.22% with a clean balance sheet, or hold the T-bill at 1.40% while the forensic picture clarifies, than chase a 5.24% FCT yield that is one Eurozone quarter away from a gearing repair exercise.

Iggy’s Forensic Disclaimer

This content is produced for educational and informational purposes only. I am not a financial advisor — I am a retail investor who applies forensic analysis to my own portfolio and shares that process publicly. Nothing here constitutes a recommendation to buy, sell, or hold any security, and no specific target prices or personalised financial advice are offered. Stocks assessed under Iggy’s Forensic Yield Standard are benchmarked against a 4.7% minimum yield hurdle; stocks flagged as Growth Watch fall below this threshold but demonstrate clean balance sheet metrics and an identifiable growth catalyst — these carry a materially different risk profile and are not suitable as yield replacements for income-dependent investors. All data is sourced from public filings and verified sources; where data is unverified it is explicitly flagged. All investments carry risk, including the potential loss of principal, and past performance is not indicative of future results. If you are making investment decisions involving CPF, SRS, or personal capital, please conduct your own due diligence or consult a MAS-licensed financial adviser before committing funds.