Stop Hoarding Fixed Deposits (The -1% Return Trap)

The uncomfortable truth: Your CPF alone won’t get you through retirement—and most Singaporeans are planning for the wrong thing entirely.

About Iggy the Investing Iguana

If you’re new here, welcome. I’m Iggy, your Singapore-based market analyst. Since October 2025, we’ve produced over 1,300 videos and 400 articles with 1.1 million watch hours. We are also home to a growing community of over 5,300 subscribers and an ‘Inner Circle’ of 100+ paid members across YouTube and Substack.

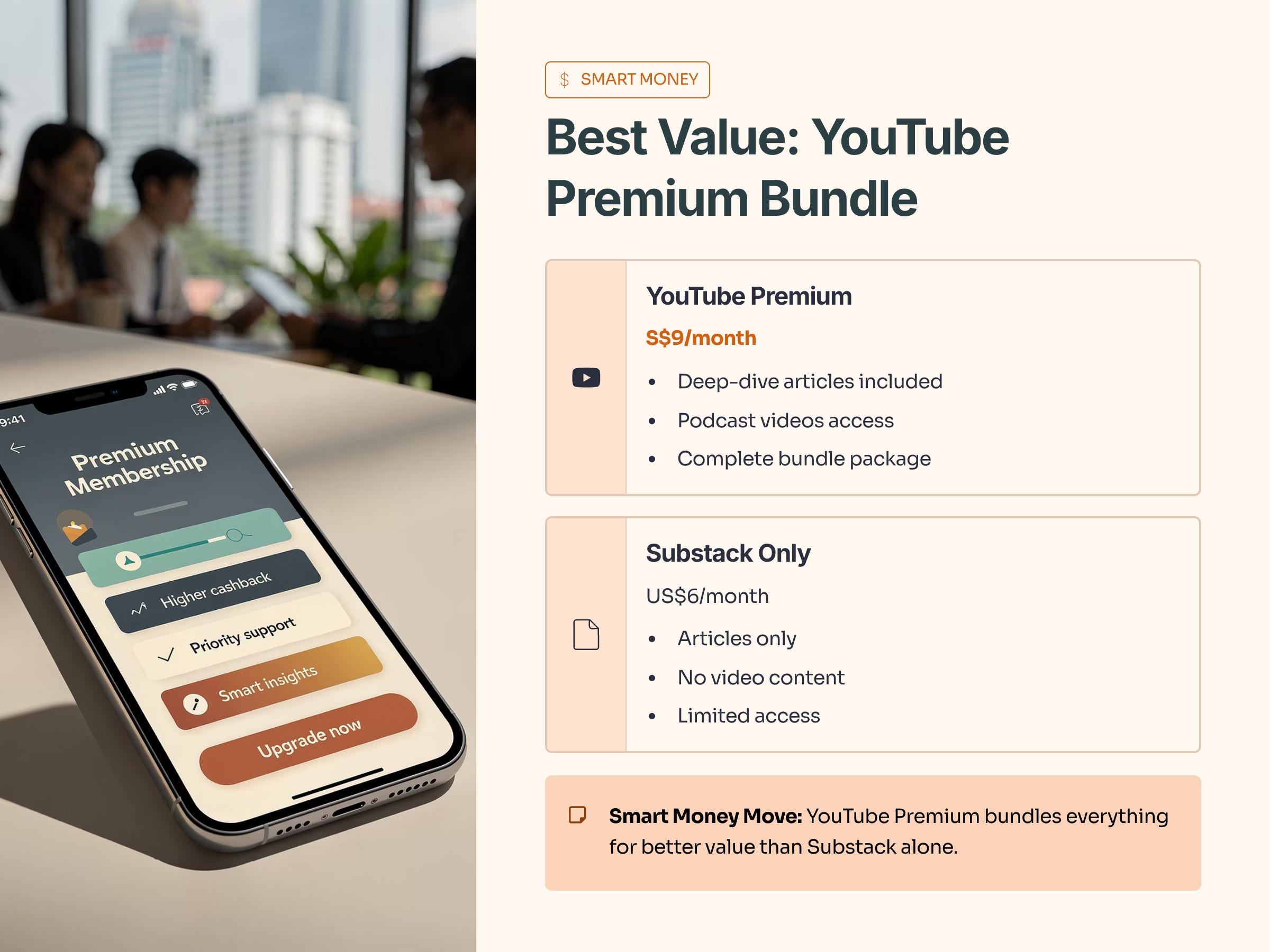

Quick Housekeeping: If you want the best value, the YouTube Premium Membership (S$9/mth) bundles these deep-dive articles with the podcast videos. Substack alone is US$6, so the bundle is the ‘smart money’ move. Now, let’s get to the numbers.

In This Article:

Concept Corner: Nominal vs Real Returns

The Silent Killer: Purchasing Power Decay

The Vehicle Showdown

The Reality of 2026 Numbers

The Retirement Health Checklist

Forecasting Your Future

The Verdict: The Action Plan

The Buy Zone (Allocation Targets)

Final Call: Designing a Life, Not Just a Portfolio

Critical Safety Rails

InvestingPro Reality Check

Iggy's VerdictConcept Corner: Nominal vs Real Returns

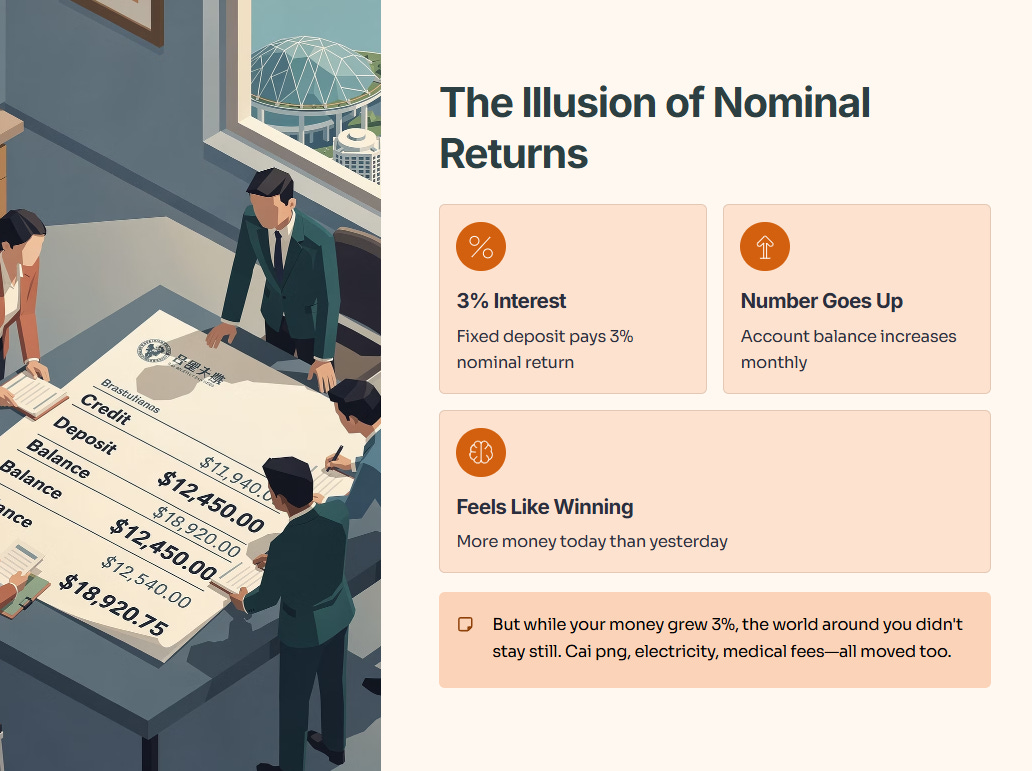

To understand why the traditional “safe” path is actually the most dangerous, we need to unpack one core idea: the gap between Nominal Returns and Real Returns, seen through the lens of purchasing power. Most Singaporeans focus only on the Nominal Return: if a fixed deposit pays three percent, that three percent feels like a win because the number in the bank goes up. You see more dollars, so your brain says, “I am richer today than yesterday.”

But that three percent is often a mirage. While your money grows, the world around you is also getting more expensive: cai png, utilities, clinic visits, even kopi all creep up over time. This is where the Real Return comes in. Real Return is simply Nominal Return minus inflation. If the bank pays three percent but inflation runs at four percent, your Real Return is negative one percent: you did not make money, you lost purchasing power.

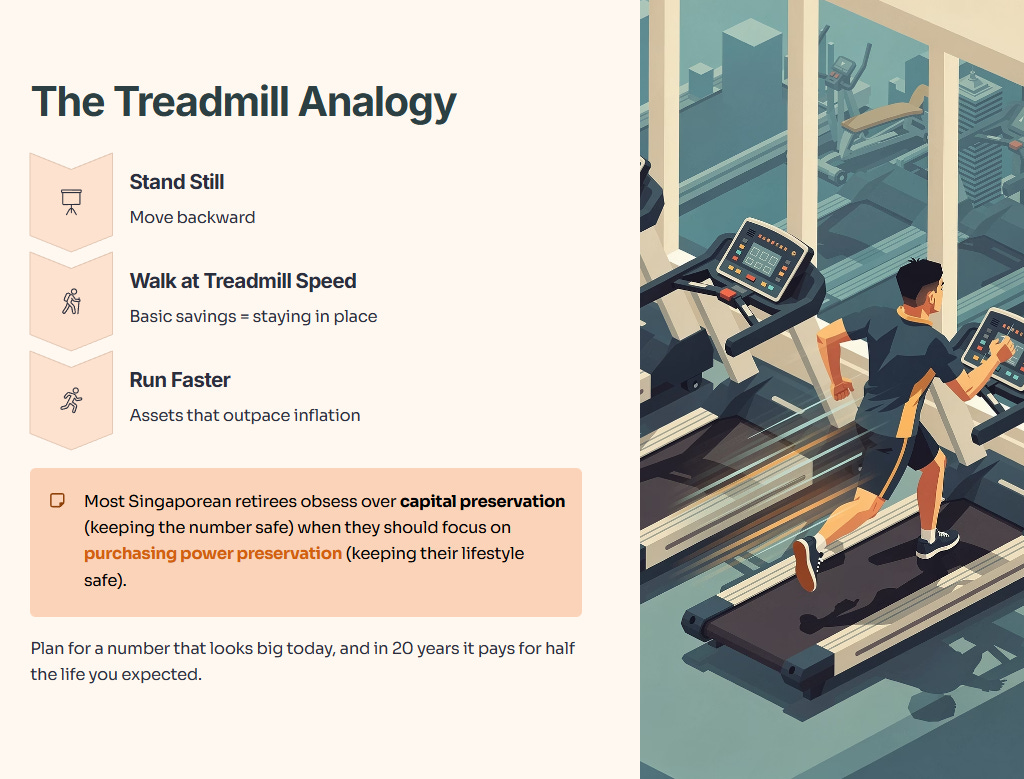

This is what can be called Purchasing Power Decay. Your statement never flashes red, there is no warning on your banking app, but year after year your dollars buy less life. Think of it like running on a treadmill. Inflation is the speed of the belt. Stand still and you drift backwards. Walk at the same speed—as with basic savings and low-yield deposits—and you stay stuck in place, burning energy just to maintain your spot.

To actually move forward, your assets must run faster than the treadmill. You need investments that outpace that erosion instead of just preserving a number on a screen. This is the crucial mindset shift: most retirees are obsessed with capital preservation—keeping the account value “safe”—when they should be obsessed with purchasing power preservation—keeping their lifestyle safe. If you ignore this distinction, you can hit your “target number” at 65, only to discover twenty years later it buys you half the life you planned for.

1. The Silent Killer: Purchasing Power Decay

The yield looks safe, but the payout ratio is screaming danger. Most retirees look at the nominal amount in their CPF account and feel safe. They forget that cash is a melting ice cube.

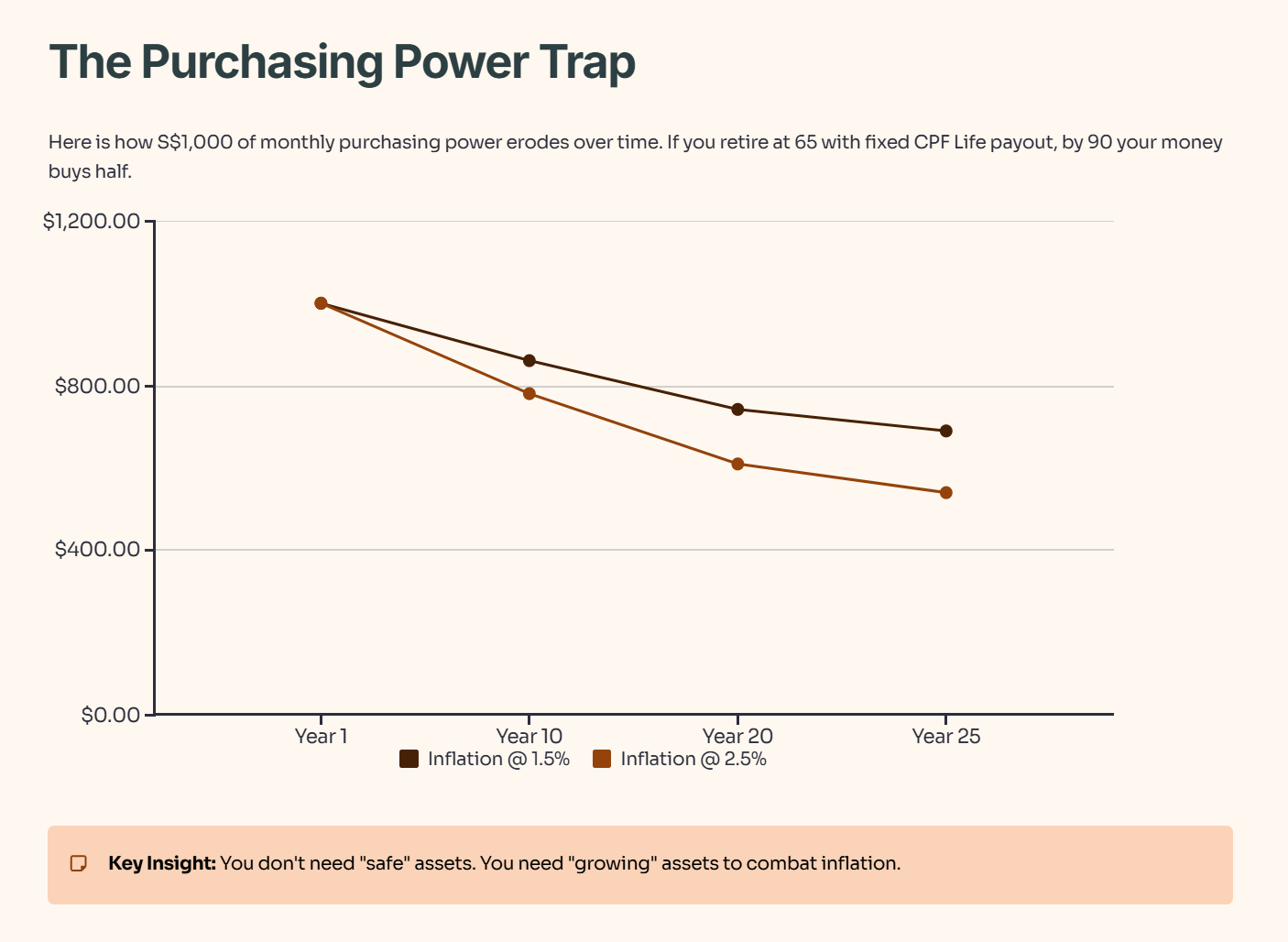

In 2026, Core Inflation is projected to be in the 0.5–1.5% range, with private forecasts around 1.3%, but lifestyle inflation (food, services, healthcare) often runs higher. Below is the visual proof of why “safe” cash is actually a guaranteed loss.

The Purchasing Power Trap

Here is how S$1,000 of monthly purchasing power erodes over time:

If you retire at 65 with a fixed CPF Life payout, by the time you are 90, your money buys half of what it does today. You don’t need “safe” assets; you need “growing” assets.

2. The Vehicle Showdown

We need to compare the typical Singaporean retirement “Standard Operating Procedure” (Property + CPF) against a diversified approach. Property is often viewed as the holy grail, but for retirement income, it can be a liquidity trap.

Peer Comparison: Asset Classes

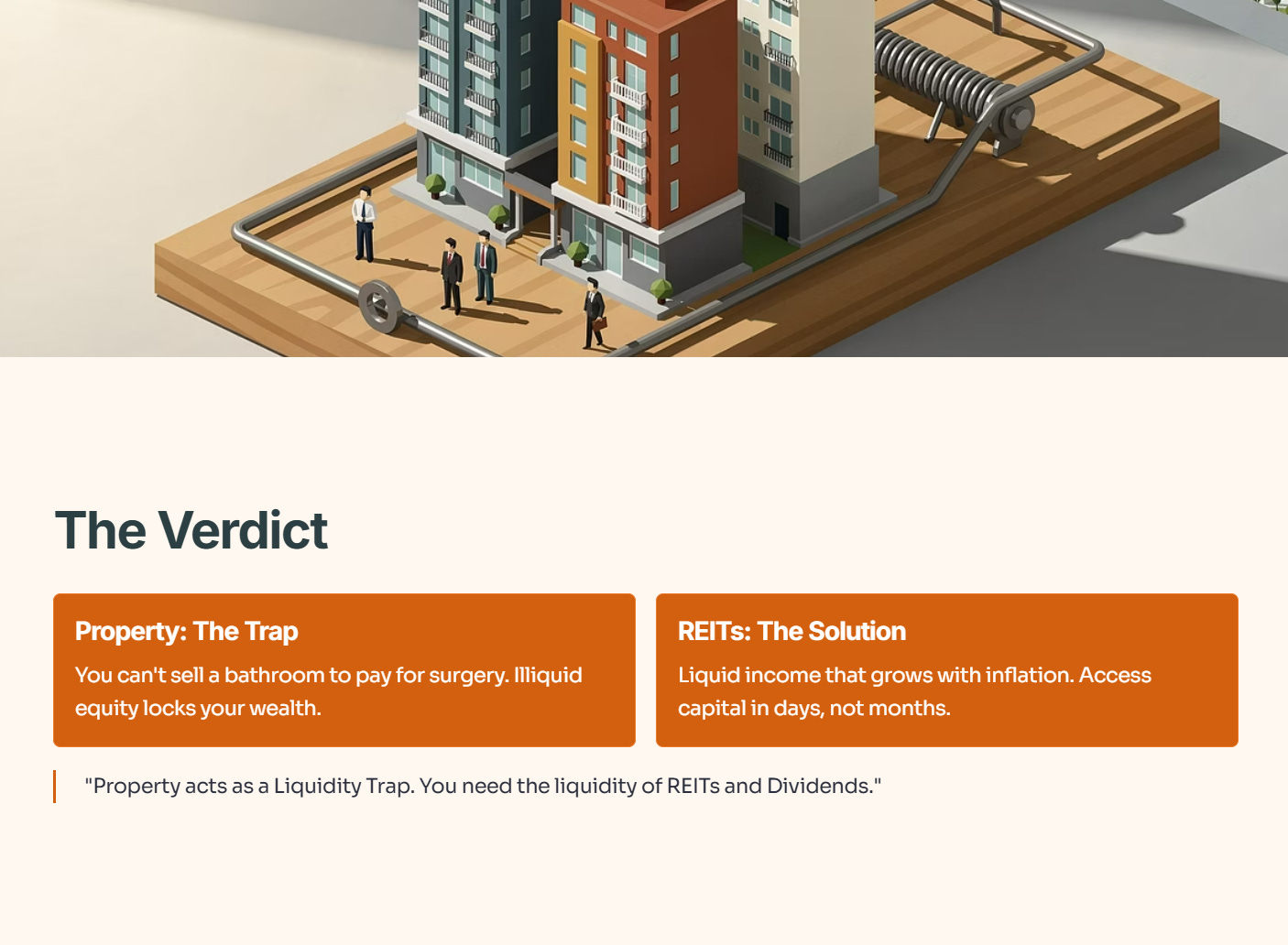

The Verdict: Property acts as a “Liquidity Trap.” You can’t sell a bathroom to pay for a surgery. You need the liquidity of REITs and Dividends.

3. The Reality of 2026 Numbers

Let’s look at the hard numbers for 2026. The CPF Board bumped the retirement sums this year. Does it cover you?