Is CPF 2028’s 0% Fee Plan the Only Way to Stop S$180K Fee Bleed | 🦖EP1585

When 55 million Indians secure pensions for S$0.67/month but a typical Singapore ILP quietly drains S$175,000 from your retirement

Section 1: The Contrarian Introduction

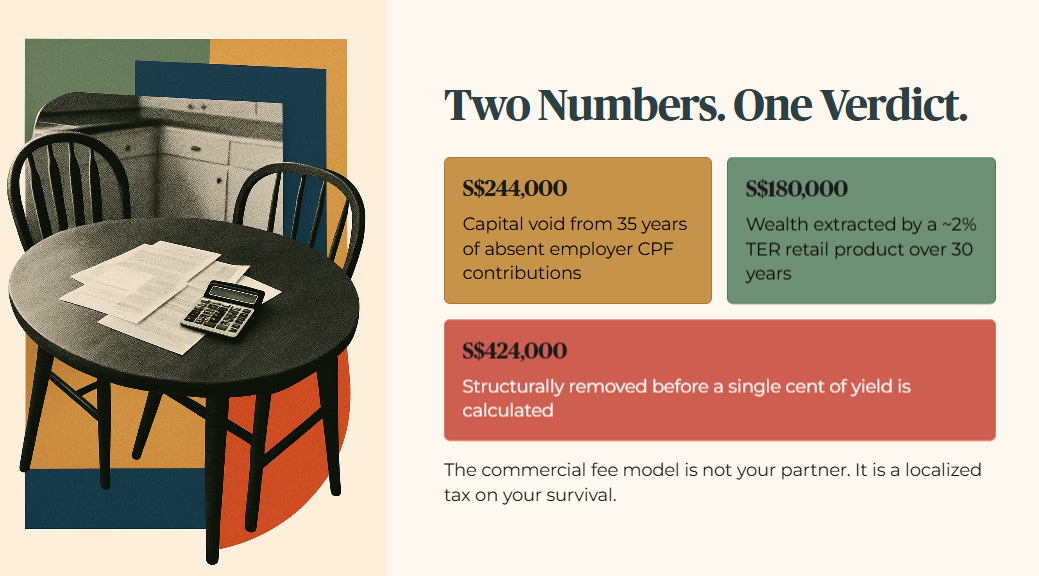

Two numbers decide whether a self-employed professional in Singapore retires with dignity or works until they collapse. The first is S$244,000. That is the exact capital void created by thirty-five years of absent employer CPF contributions for an independent contractor earning S$6,000 a month. The second number is S$180,000. That is the wealth quietly extracted by a standard retail wealth product carrying a ~2% Total Expense Ratio over a thirty-year horizon.

We are not discussing market volatility or bad stock picks. We are looking at a mathematical certainty where S$424,000 is structurally removed from the kitchen table before a single cent of yield is calculated. If you are operating outside the corporate safety net, the commercial fee model is not your partner. It is a localized tax on your survival.

🦎 Iggy’s Insight Block

Institutional capital flows through Asia on a highly curated narrative of rising middle classes and domestic consumption booms. The financial centers price regional growth as an absolute certainty. Yet the underlying data tells a fundamentally different story about capital retention at the ground level.

We are tracking a psychological gap between offshore fund managers selling the Asian century and the localized reality of a continent aging without a safety net. The infrastructure built to manage wealth is actively accelerating its depletion through frictionless fee extraction. The greatest threat to regional stability is not geopolitical tension. It is the mathematical certainty of demographic insolvency.

In This Article:

The Regional Timebomb

Indias Proof of Concept

The Singapore Gap

CPF 2028 Admission

Forensic Stress Test

Infrastructure Contrast Table

Why Self Employed Bleed First

The 0 Fee Fortress

Iggys Bottom Line

Iggys Forensic Disclaimer

Section 2: The Regional Timebomb

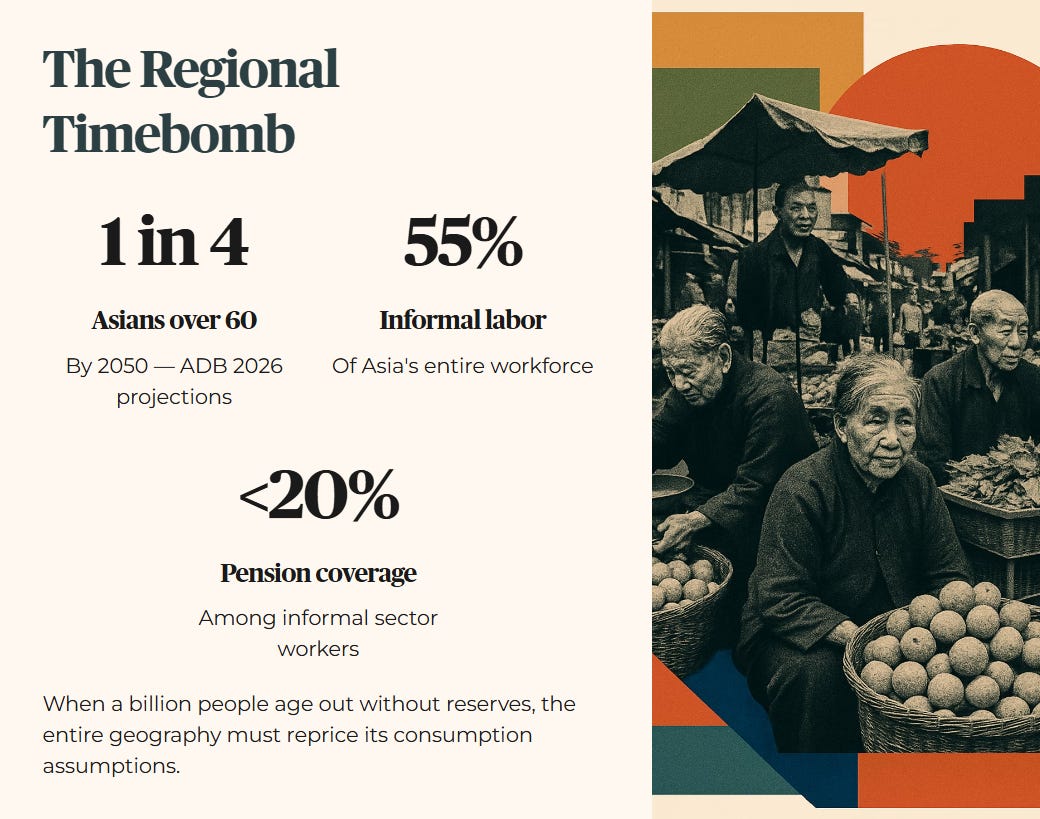

The broader macro context begins with a demographic shockwave that fundamentally alters the cost of capital. According to the Asian Development Bank 2026 projections, one in four Asians will be over the age of sixty by the year 2050. We are looking at a vast, interconnected economic zone where fifty-five percent of the labor force operates in the informal sector. Less than twenty percent of these workers possess any form of structured pension coverage. When a billion people age out of the workforce without accumulated reserves, the entire geography must reprice its consumption assumptions. Capital will be forced to redirect from discretionary growth engines into basic survival infrastructure.

But we do not deal in abstract regional theories. We deal in direct kitchen-table consequences. For a household in Toa Payoh, the disruption of global labor pools inevitably imports inflation across our borders. We are tracking a specific cost of living impact where basic monthly grocery and utility expenditures for a standard four-room flat have increased by S$315 over a trailing twenty-four-month period. That is S$3,780 a year lost to inflation alone. The demographic trade winds that fueled decades of manufacturing dominance are reversing course. The structural reality is that regional inflation lands squarely on the local retail consumer.

Section 3: India’s Proof of Concept

The math defines the ultimate utility of a sovereign structural bypass. We analyze the Indian framework not as an investment recommendation, but as a proof of concept regarding infrastructural efficiency at pure scale.

Table 1: Atal Pension Yojana Breakdown

(Source: PFRDA 2026.)

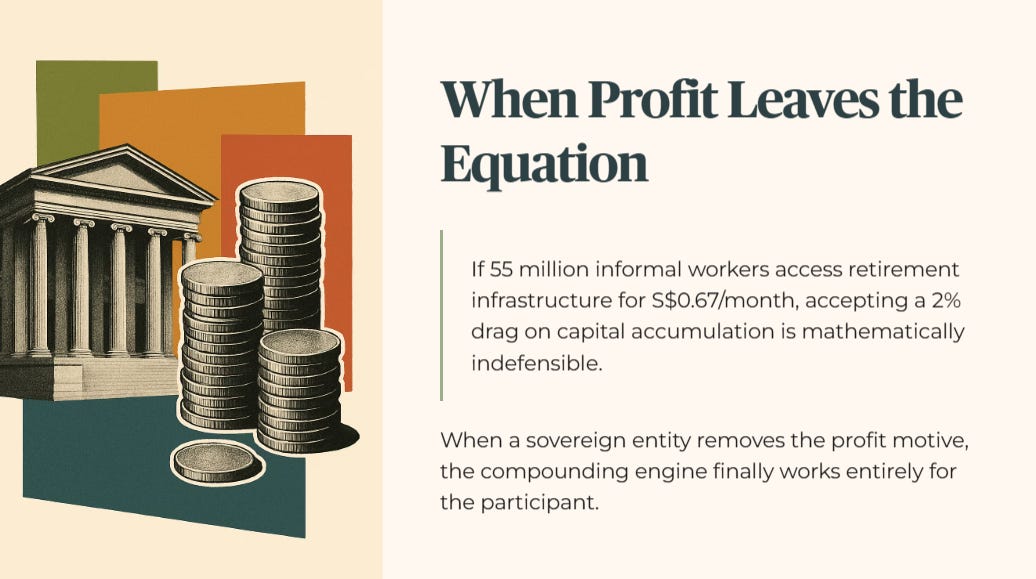

If fifty-five million informal workers can access baseline retirement infrastructure for roughly S$0.67 a month, the localized acceptance of a two percent drag on capital accumulation is mathematically indefensible. The commercial architecture attempts to normalize administrative friction as a necessary cost of doing business. The sovereign micro-pension standard proves that baseline administration can be maintained for pennies. When a sovereign entity removes the profit motive from the accumulation vehicle, the compounding engine finally works entirely for the participant.

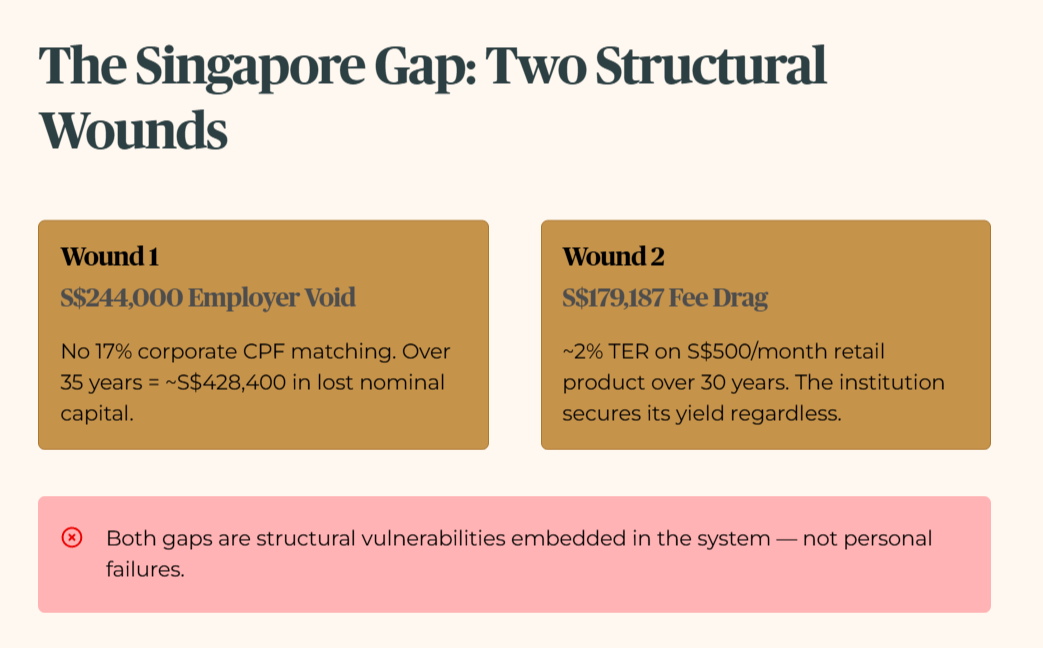

Section 4: The Singapore Gap

The structural disadvantage for the self-employed operates on two distinct fronts. Both gaps represent structural vulnerabilities embedded in the system, not personal failures of the individual.

The first is the S$244,000 employer void. Without mandatory employer CPF contributions, an independent contractor earning S$6,000 a month misses out on the standard seventeen percent corporate matching. Over a thirty-five-year timeline, that absence equals roughly S$428,400 in lost nominal capital before compounding is even modeled. We baseline this immediate structural deficit at a S$244,000 void in the primary base. It is a massive hole dug on day one of a career.

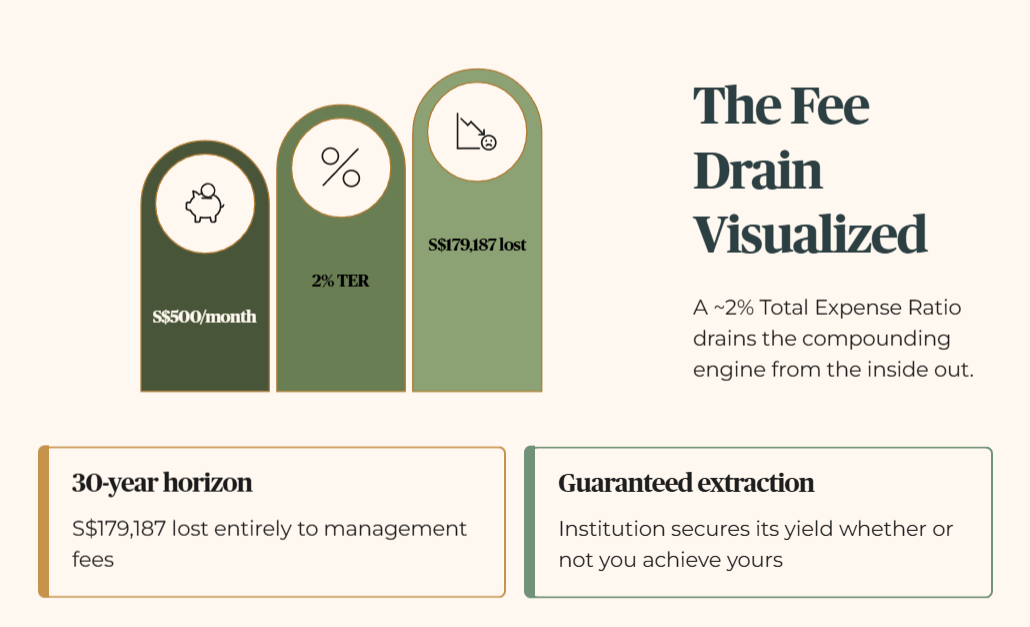

The second vulnerability is the S$180,000 fee drag. When self-employed individuals attempt to bridge their CPF deficit by routing S$500 a month into standard retail retirement products, the architecture actively works against them. A product carrying a ~2% Total Expense Ratio systematically drains the compounding engine from the inside out. Over a thirty-year horizon, forensic framework shows that S$179,187 is lost entirely to management fees. The fee structure guarantees that the institution secures its yield regardless of whether the retail investor achieves theirs.

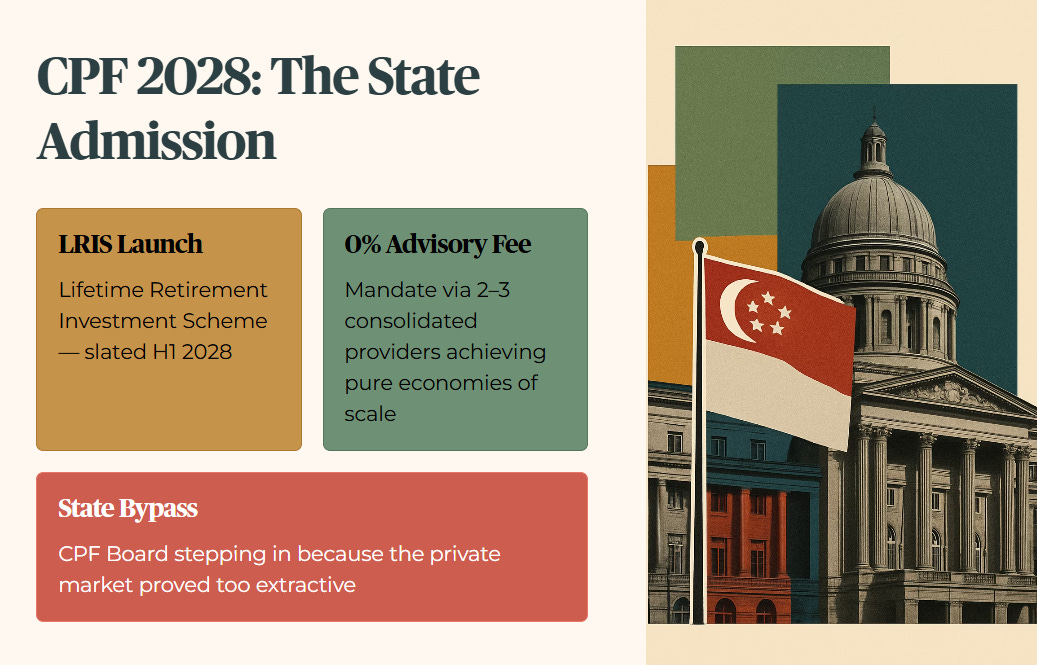

Section 5: CPF 2028 Admission

Data indicates that the administrative state recognizes the mathematical failure of the commercial fee model. The CPF Board has officially signaled the launch of the Lifetime Retirement Investment Scheme, slated for the first half of 2028. This framework introduces a zero percent advisory fee mandate by utilizing two to three consolidated providers to achieve pure economies of scale.

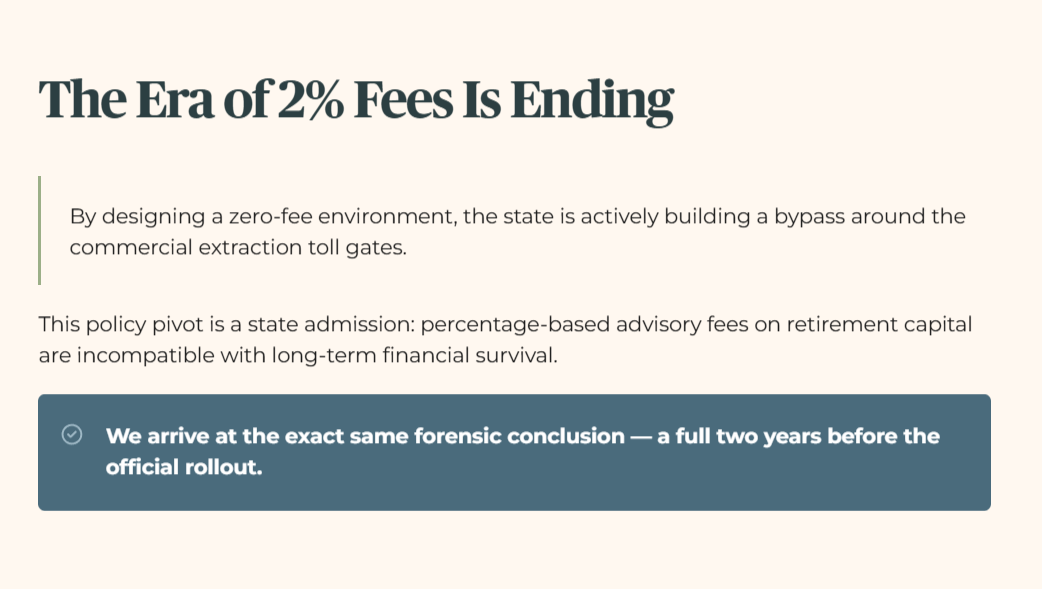

The sovereign apparatus is stepping in because the private market architecture has proven too extractive for baseline retirement security. This policy pivot functions as a state admission that percentage-based advisory fees on retirement capital are incompatible with long-term financial survival. By designing a zero-fee environment, the state is actively building a bypass around the commercial extraction toll gates. We arrive at the exact same forensic conclusion a full two years before the official rollout. The era of paying two percent for access to basic market beta is ending.

🦎 Iggy’s Insight Block

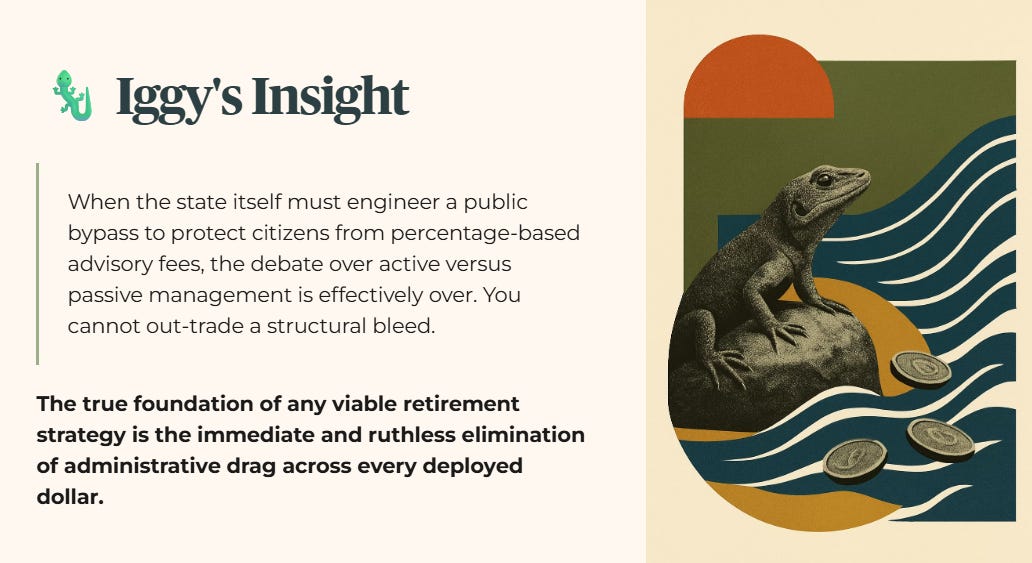

The most dangerous assumption a retail investor can make is that their wealth manager’s interests are perfectly aligned with their own. The commercial imperative is absolute extraction within the bounds of regulatory compliance. When the state itself must engineer a public bypass to protect citizens from percentage-based advisory fees, the debate over active versus passive management is effectively over. You cannot out-trade a structural bleed. The foundation of any viable retirement strategy is no longer asset selection. The true foundation is the immediate and ruthless elimination of administrative drag across every single deployed dollar.

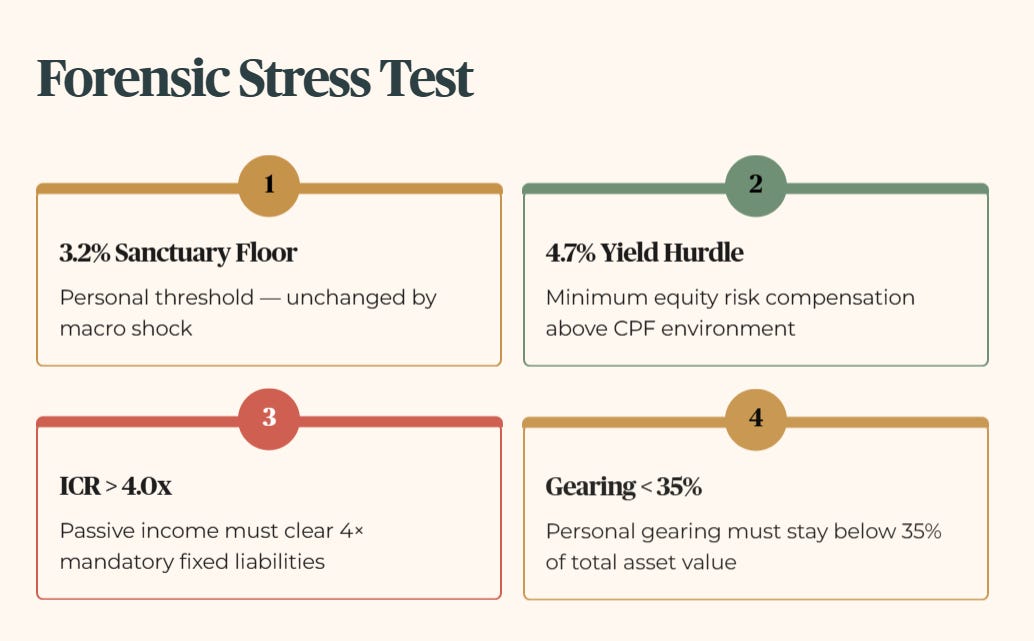

Section 6: Forensic Stress Test

To survive a regional macro shock, a retirement portfolio must operate like an institutional balance sheet. My personal sanctuary threshold remains three point two percent. A sustained macro shock does not change the floor. It changes how many assets can still clear it.

We apply the 4.7% minimum yield hurdle as our baseline for equity risk compensation above the CPF environment. We test personal accumulation using strict corporate governance metrics. An individual’s passive income streams must clear an Interest Coverage Ratio of greater than four times relative to their mandatory fixed liabilities.

Furthermore, their personal gearing must remain below thirty-five percent of total asset value. The Indian Atal Pension Yojana architecture easily passes the 4.0x ICR test for a low-income participant because the structural liability is infinitesimal. Conversely, a retail investment plan carrying a ~2% TER categorically fails the stress test. The compounding weight of the fee structure acts as shadow debt. It breaches the equivalent of a thirty-five percent gearing ceiling by constantly pulling capital away from the principal base before any actual yield can even be generated.

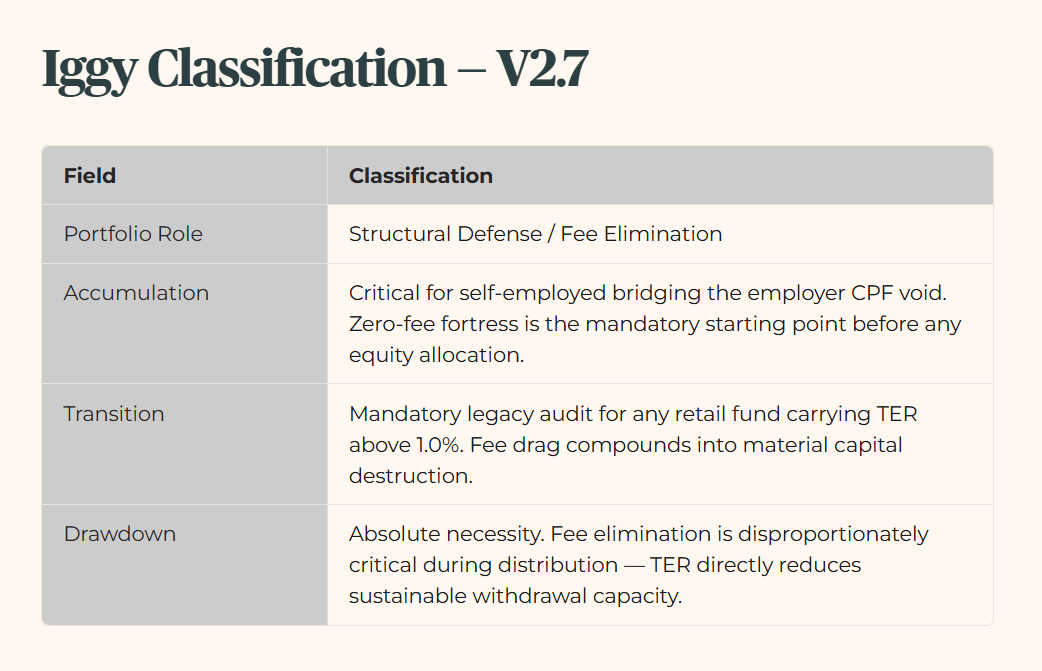

[IGGY CLASSIFICATION — V2.7]

The infrastructure contrast table that follows does not just visualise this bleed — it recalculates the entire S$175,000 gap across a full 30-year horizon and forces you to confront exactly how much of your “retirement plan” is actually funding the fee line, not your future.