Keppel DC REIT: +40% Rental Reversion vs. -21% Downside Risk

With T-Bill yields collapsing to 1.4%, the 4.4% yield on this Data Centre giant looks tempting. But the institutional models are flashing a warning sign you can’t ignore.

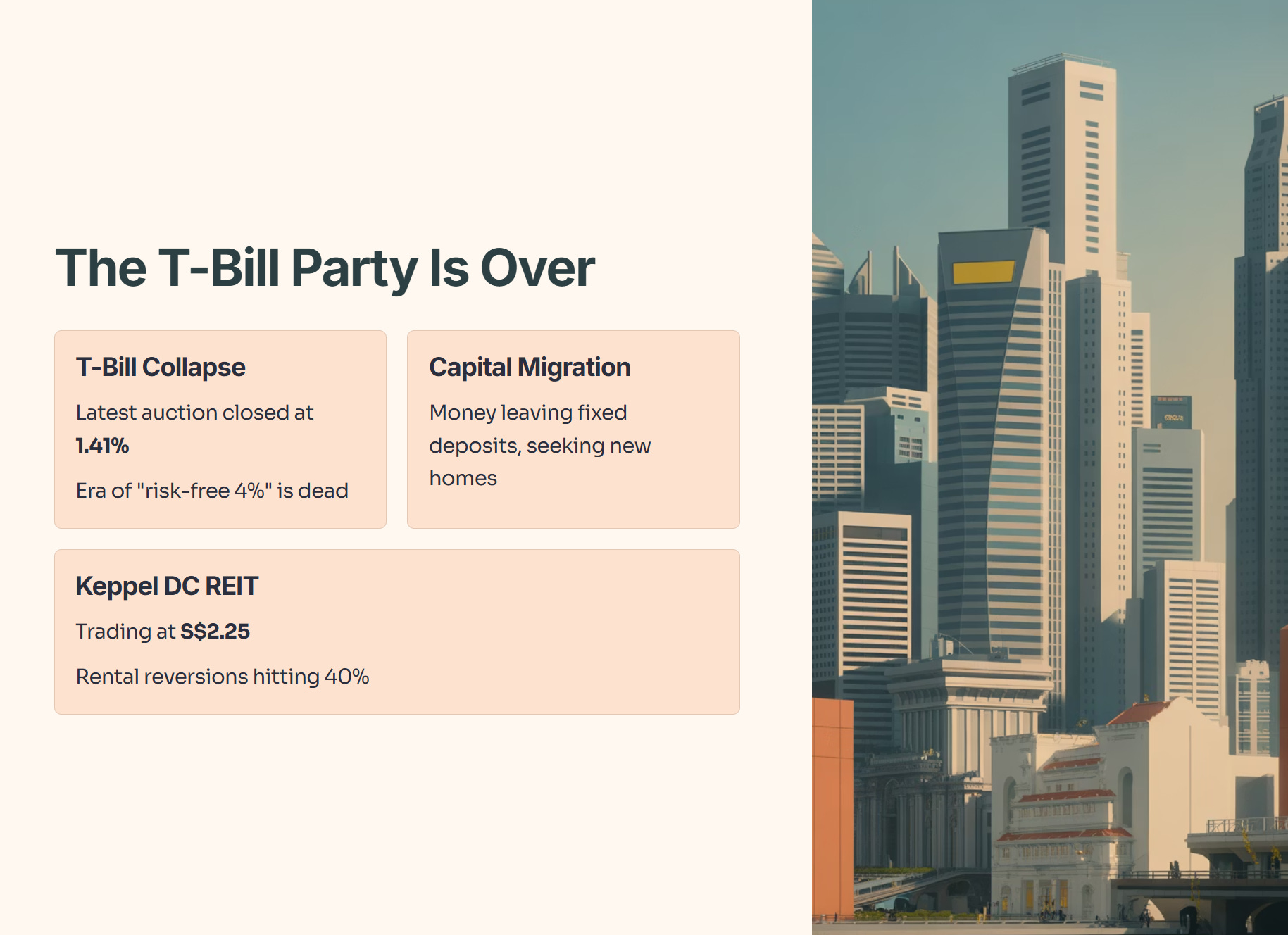

If you’ve been parking your cash in Singapore T-Bills for the last two years, the party is officially over. The latest auction just closed at a depressing 1.41%. The era of “risk-free 4%” is dead, and the capital that was hiding in fixed deposits is waking up and looking for a home.

Naturally, eyes are turning to Keppel DC REIT (SGX: AJBU). It’s the darling of the SGX—pure-play data centres, AI tailwinds, and a chart that’s finally waking up. At S$2.25, it’s not cheap, but with rental reversions hitting nearly 40%, the growth story is intoxicating.

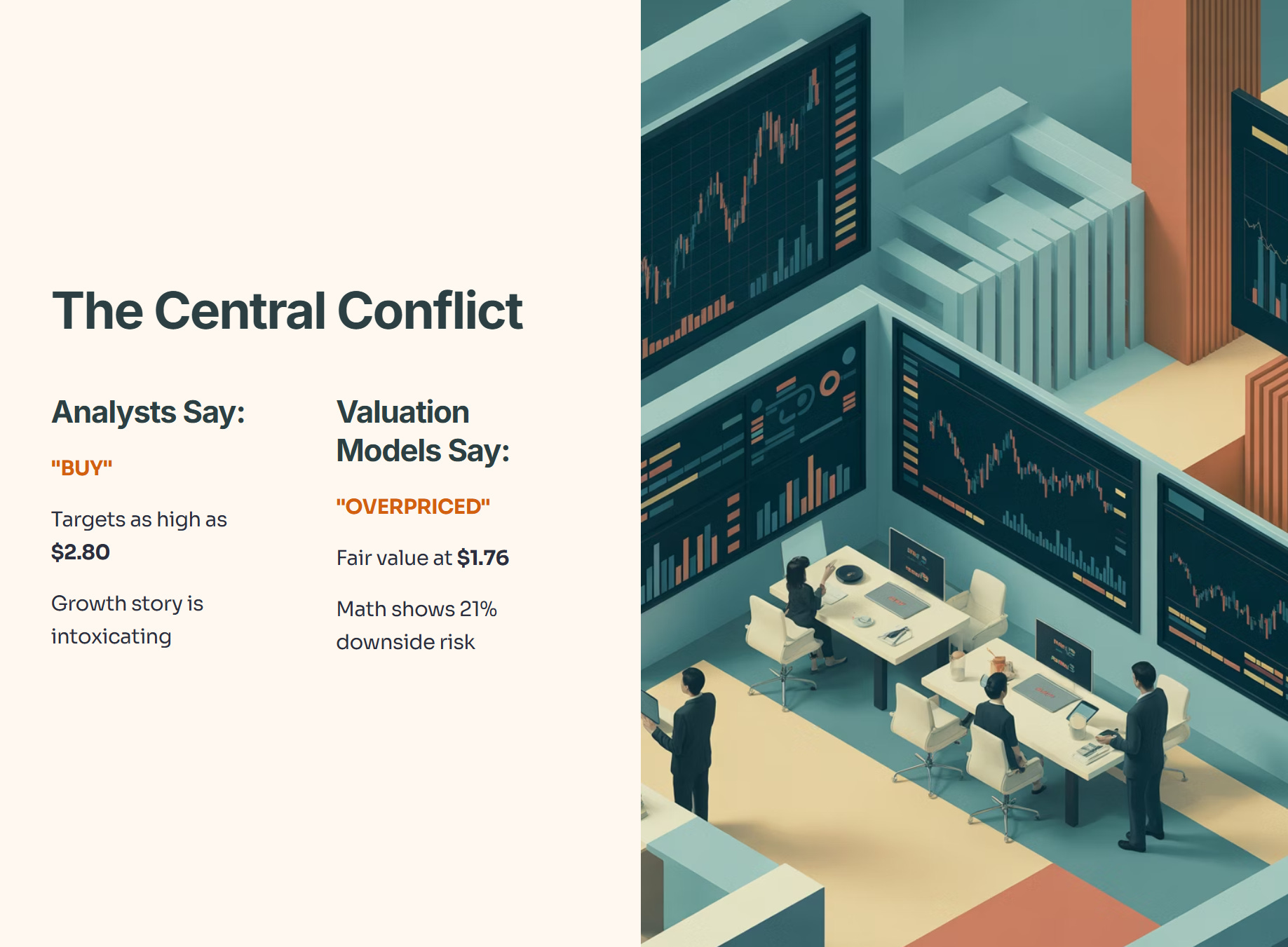

But here is the conflict: The analysts are screaming “Buy” with targets as high as $2.80, while the valuation models are screaming “Overpriced.”

Who is right? The growth-hungry bulls or the math-obsessed bears? Let’s dive into the numbers.

In This Article:

• The Bull Case: Why The Market Is Paying a Premium

• 1. The “AI” Rental Reversion is Real

• 2. A Fortress Balance Sheet in a Falling Rate World

• The Bear Case: The “Valuation Trap”

• 1. The “Fair Value” Disconnect

• 2. The Hidden “Land Lease” Risk

• 3. The China Drag

• The Investor’s Action Plan

• Iggy’s Final Verdict

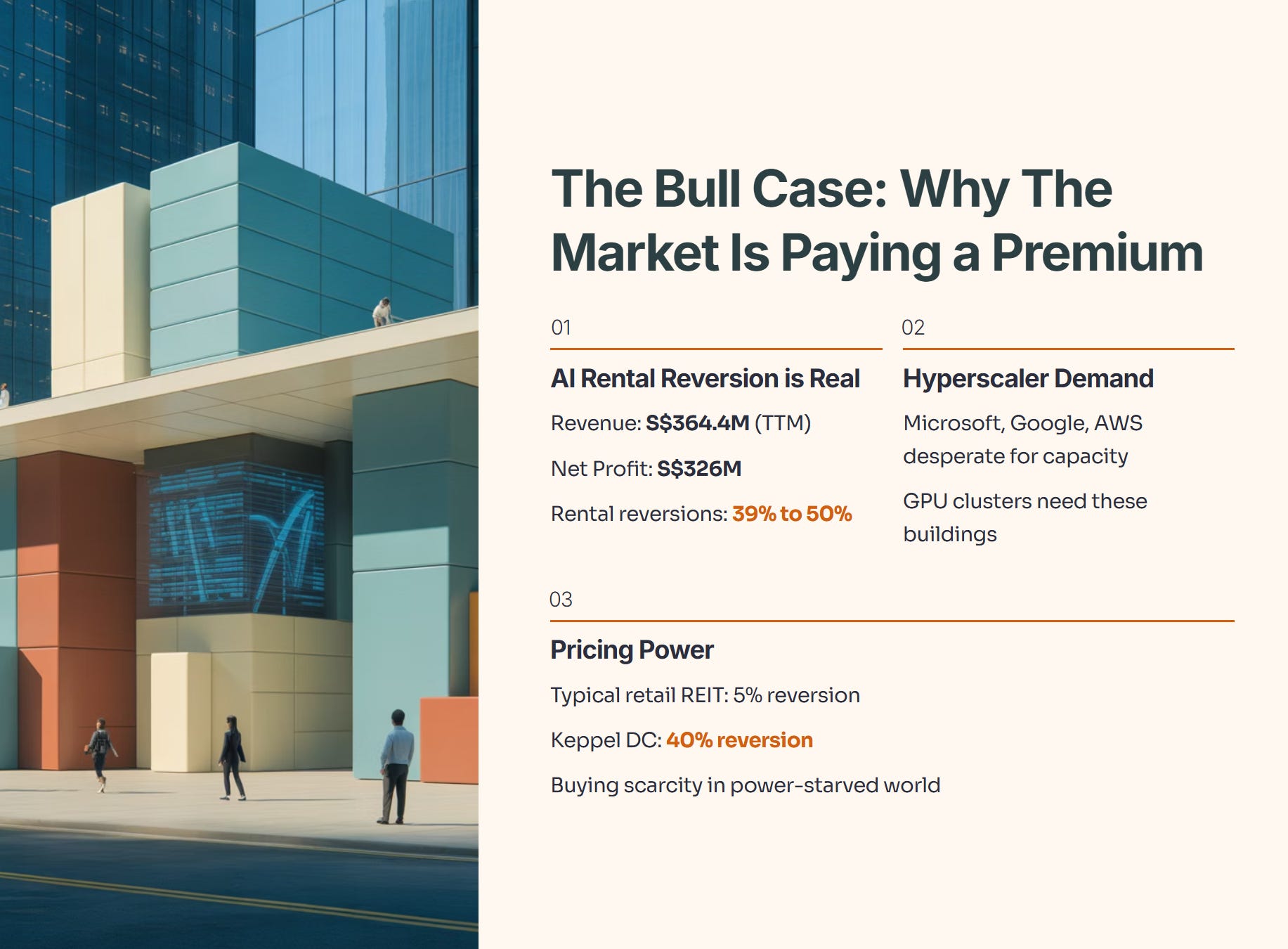

The Bull Case: Why The Market Is Paying a Premium

Keppel DC REIT isn’t just a landlord; it’s a toll booth on the AI superhighway. The latest financials (Snapshot 1) paint a picture of a company firing on all cylinders.

1. The “AI” Rental Reversion is Real

Revenue has jumped to S$364.4M (Trailing 12M), and Net Profit is up to S$326M. But the real story isn’t the top line; it’s the pricing power.

We are seeing rental reversions—the increase in rent when a lease renews—hitting 39% to 50% in key markets. This confirms that hyperscalers (think Microsoft, Google, AWS) are desperate for capacity. They need these buildings for their GPU clusters, and they are willing to pay up.

Iggy’s Insight:

This is what “pricing power” looks like. In a typical retail REIT, you pray for a 5% reversion. Keppel DC is getting 40% because supply is constrained. You aren’t just buying real estate here; you are buying scarcity in a power-starved world.

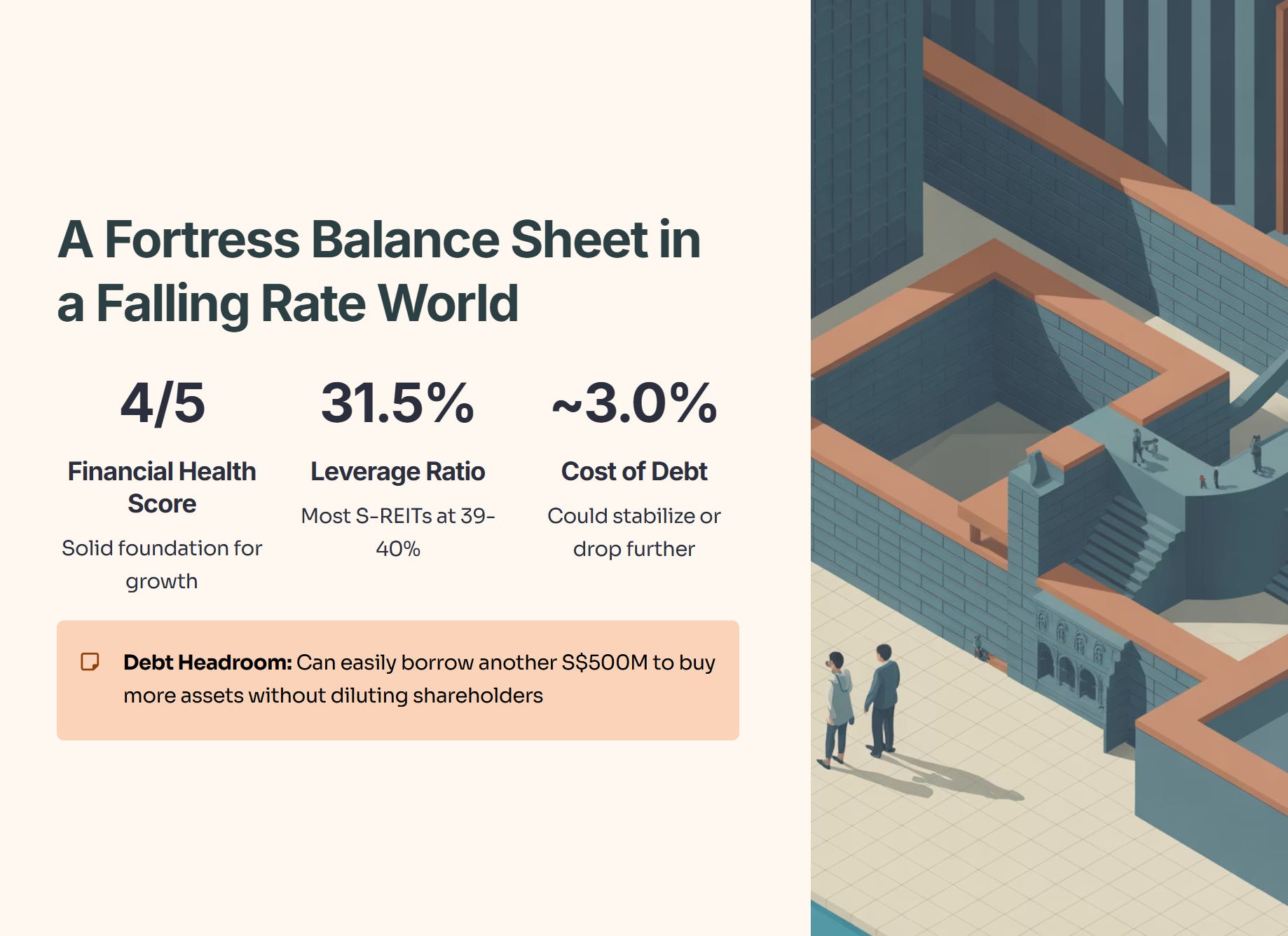

2. A Fortress Balance Sheet in a Falling Rate World

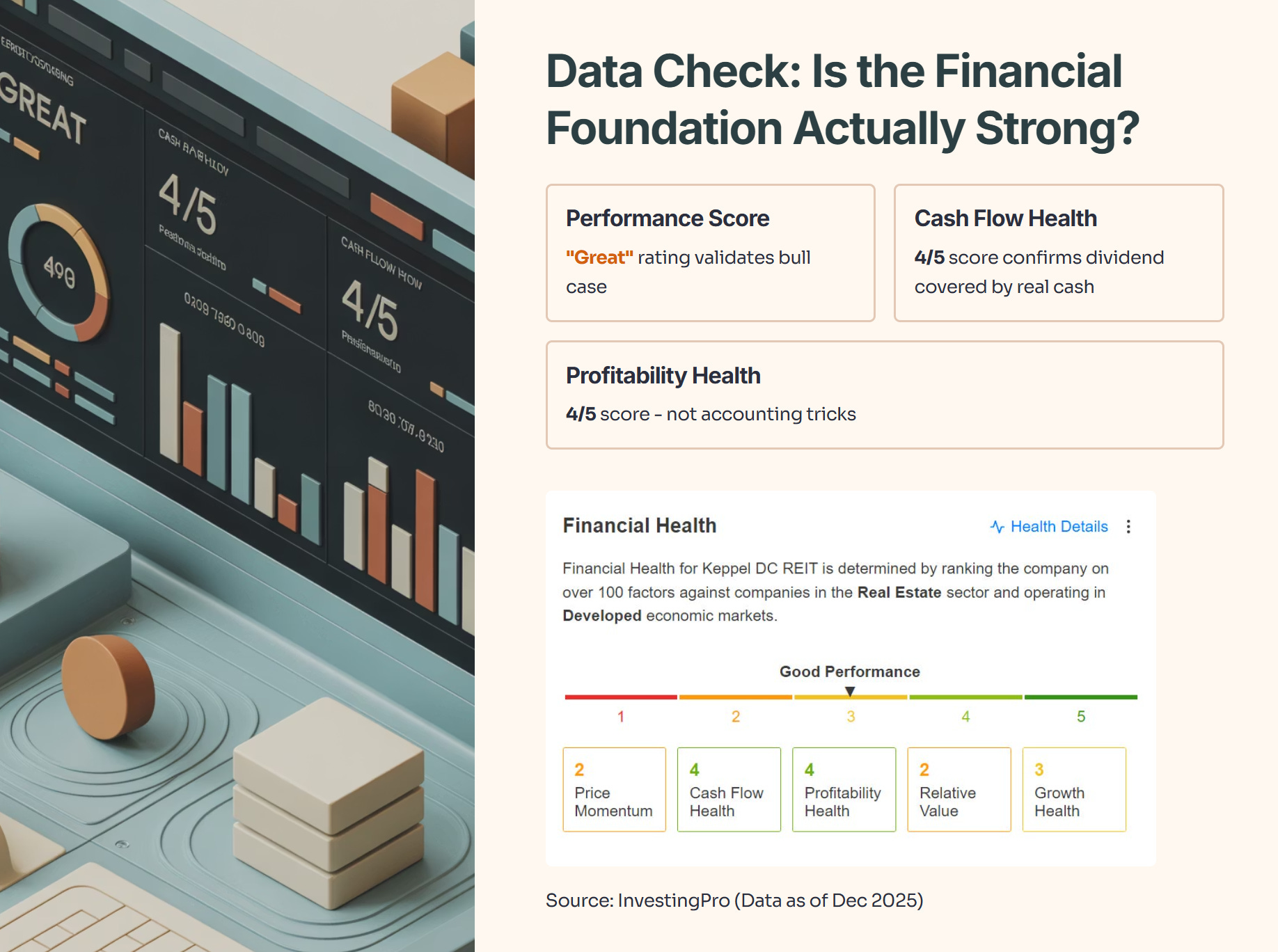

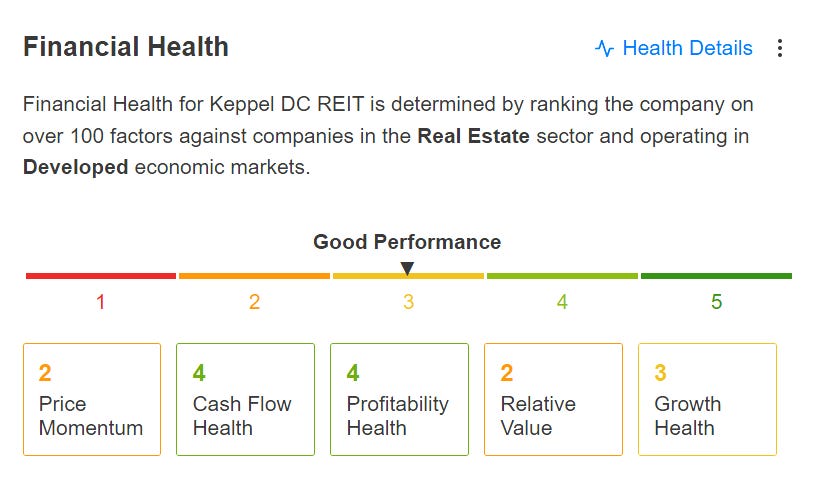

Look at the Financial Health score in our data (Snapshot 2). It’s a solid 4/5.

Why? Because their leverage is sitting at a very comfortable 31.5%.

In the REIT world, 31.5% is practically zero. Most S-REITs are sweating at 39-40%. This gives Keppel DC massive “debt headroom.” They can easily borrow another S$500M to buy more assets without diluting shareholders. With global interest rates falling, their cost of debt (currently ~3.0%) could stabilize or even drop, widening their margins.

Data Check: Is the Financial Foundation Actually Strong?

I don’t just trust the narrative; I check the raw health metrics.

Source: InvestingPro (Data as of Dec 2025). Premium members can use code INVESTINGIGUANA for up to 50% off.

The Verdict: The “Great” performance score validates the bull case. The Cash Flow Health and Profitability Health scores (both 4/5) confirm that the dividend is covered by real cash, not accounting tricks. This is a high-quality machine.

The Bear Case: The “Valuation Trap”

If everything is so perfect, why am I worried? Because price matters.

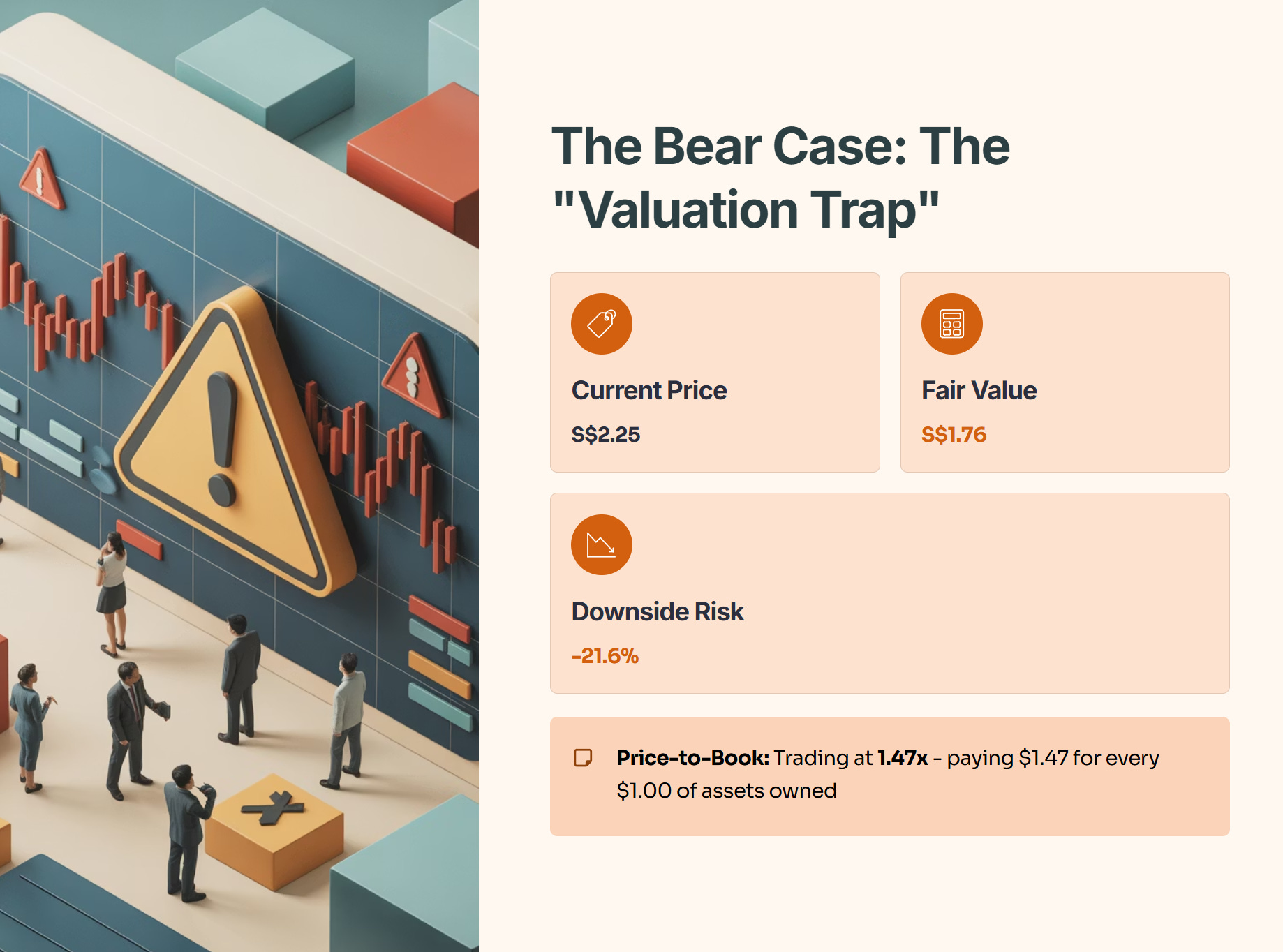

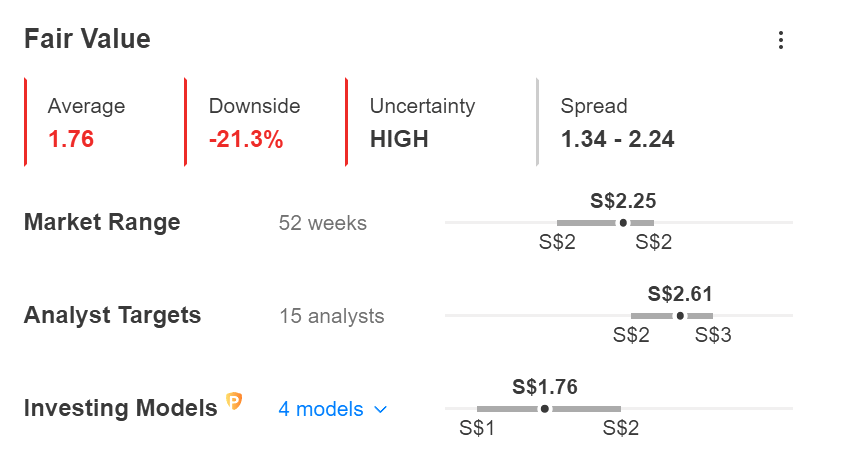

1. The “Fair Value” Disconnect

This is where the rubber meets the road.

Current Price: S$2.25

InvestingPro Fair Value: S$1.76

Downside Risk: -21.6%

The algorithms (which look at Price-to-Book, P/E, and discounted cash flows) think the stock is expensive. It is trading at 1.47x Price-to-Book. In plain English, you are paying $1.47 for every $1.00 of assets they own.

Iggy’s Take:

A 21% downside warning is significant. The market is pricing Keppel DC REIT for perfection. If they miss earnings by even a cent, or if AI capex slows down slightly, that premium evaporates. You are paying for growth that hasn’t happened yet.

Data Check: The Valuation Reality

Let’s look at the specific model output that suggests the stock is overvalued.

Source: InvestingPro (Data as of Dec 2025). Premium members can use code INVESTINGIGUANA for up to 50% off.

The Analysis: Notice the spread. The Analyst Targets (Grey line) are optimistic at S$2.61, betting on future growth. The Fair Value Models (Red line) are grounded in current math at S$1.76. When these two diverge this widely, volatility usually follows.

2. The Hidden “Land Lease” Risk

There is a structural issue with Keppel DC REIT that many new investors miss. A large chunk of their Singapore portfolio (including the crown jewels SGP 7 & 8) sits on short land leases.

Some assets have less than 20 years remaining.

Extending these leases costs money—a lot of money.

We know they need to pay ~S$350M to extend the leases for SGP 7 & 8.

While they have the debt headroom to pay for this, it is effectively a “maintenance cost” that eats into returns. It means a portion of that 4.4% yield is actually just your own capital being returned to you before the asset depreciates to zero.

3. The China Drag

While Singapore is booming, their China assets (Guangdong) have faced issues with tenant payments and loss allowances. It’s a small part of the portfolio, but it’s a drag on DPU that prevents the stock from flying even higher.

The Investor’s Action Plan