Stop Chasing ESR-REIT: The Valuation Trap Explained

The turnaround is real, but the price has detached from reality. I’m ignoring the FOMO—here is the exact math behind my wait-and-see strategy.

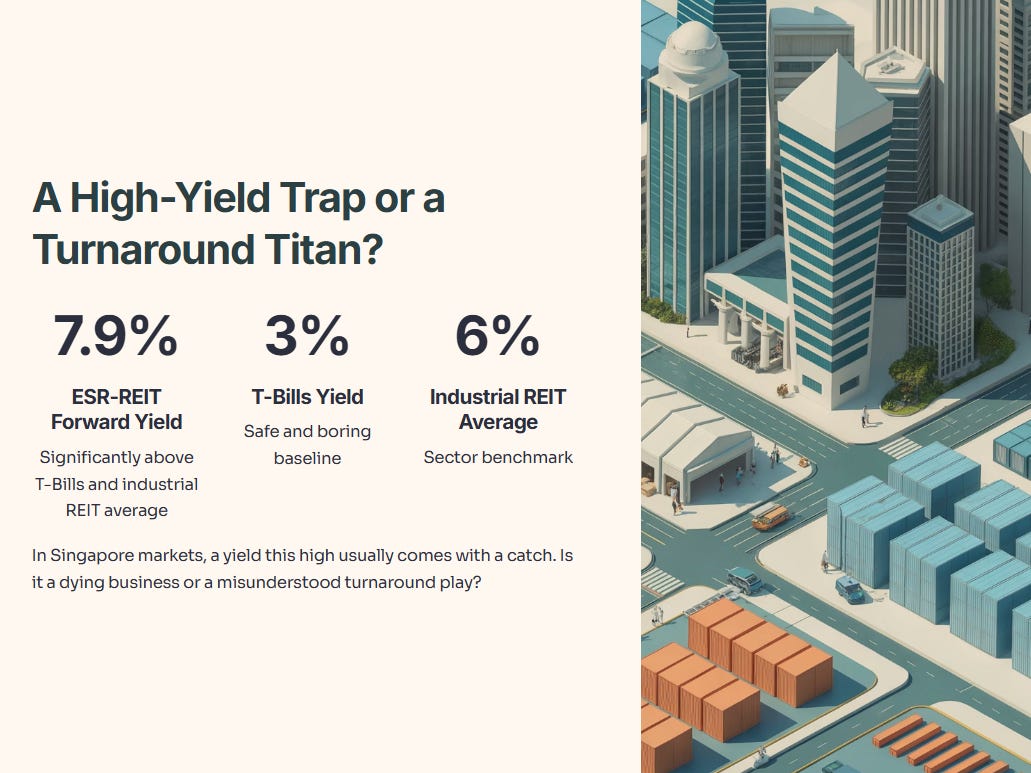

A High-Yield Trap or a Turnaround Titan?

If you are screening for yield on the SGX right now, ESR-REIT (SGX: 9A4U) has likely flashed on your radar. With a forward yield touching 7.9%, it is sitting comfortably above the “safe and boring” 3% you get from T-Bills and significantly higher than the industrial REIT average of around 6%.

But in the Singapore market, a yield that high usually comes with a catch. Is it a dying business paying out its last reserves, or is it a misunderstood turnaround play that the market has mispriced?

The headline numbers look spectacular: Revenue is up 23%, and Net Property Income (NPI) has surged 30%. Yet, the stock price has been volatile, and the gearing ratio is uncomfortably close to the ceiling.

Today, we aren’t just reading the press release. We are digging into the debt maturity profile, the “New Economy” pivot, and looking at what the algorithmic models say versus the human analysts.

In This Article:

• Section 1: The Hard Numbers (The Financial Snapshot)

• Section 2: The Dividend (The “Meat” for SG Investors)

• Section 3: The “3 Good” (Bull Case Arguments)

• Section 4: The “3 Red Flags” (Bear Case Risks)

• Section 5: The Singaporean Context & Verdict

• Section 6: The Iggy Playbook: What to do?

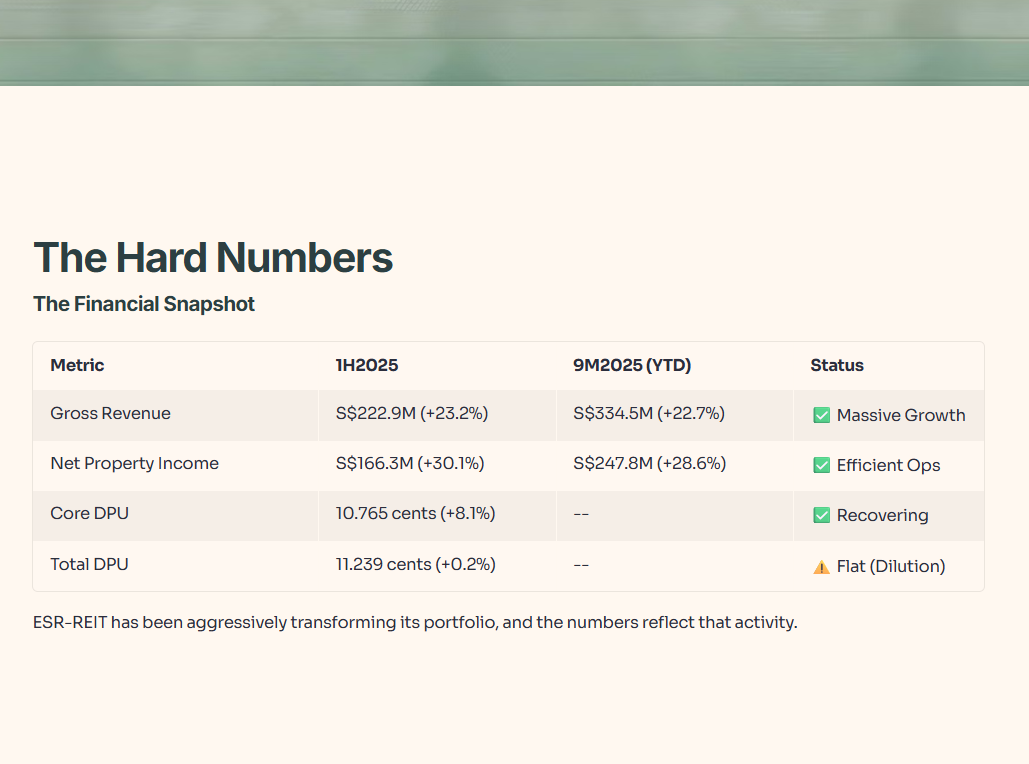

Section 1: The Hard Numbers (The Financial Snapshot)

Let’s look at the engine room. ESR-REIT has been busy transforming its portfolio, and the 1H2025/9M2025 numbers reflect that aggressive activity.

The Growth Story (YoY)

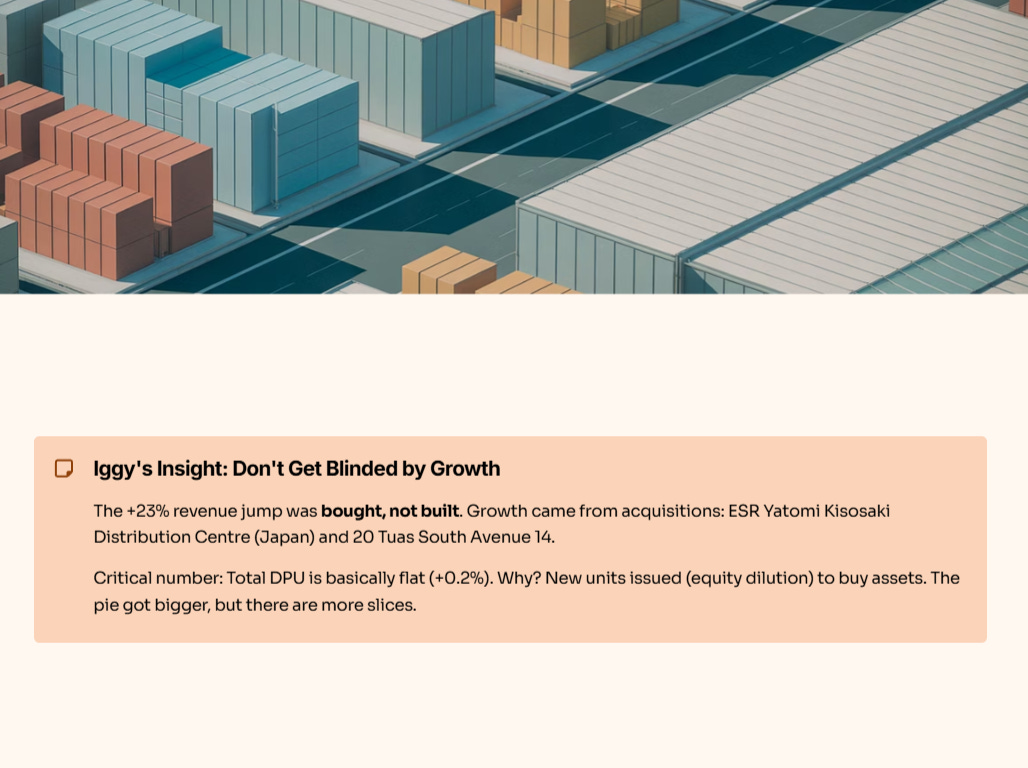

Iggy’s Insight:

Don’t get blinded by the +23% revenue jump. That growth was bought, not just built. It comes from the acquisition of the ESR Yatomi Kisosaki Distribution Centre in Japan and 20 Tuas South Avenue 14. The critical number here is the Total DPU, which is basically flat (+0.2%). Why? Because they issued new units (equity dilution) to buy those assets. The pie got bigger, but there are more slices.

The Valuation Reality Check

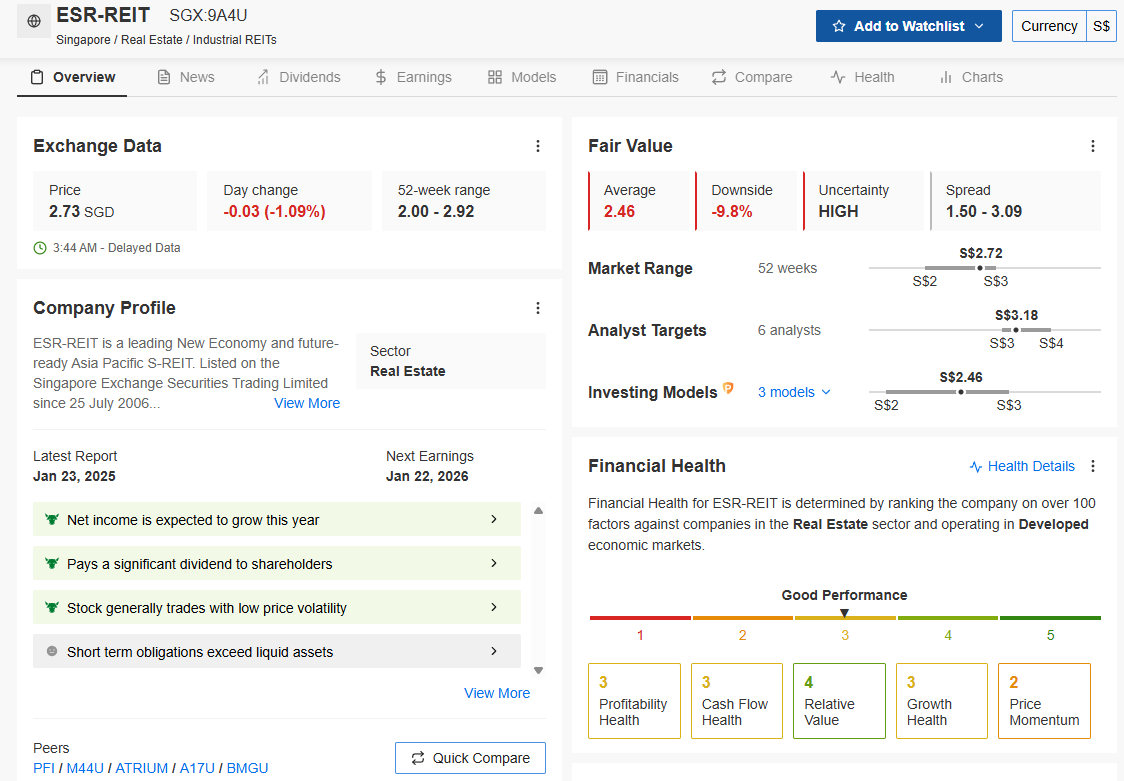

The stock is currently trading around S$2.72. Analyst consensus (human beings) have price targets ranging from S$3.00 to S$3.64, suggesting significant upside.

However, human analysts are often optimistic. I prefer to cross-reference with algorithmic models that look at cash flow and book value without emotion.

I don’t just guess at valuations. I check the institutional models.

Source: InvestingPro (Data as of Dec 2025). Premium members can use code INVESTINGIGUANA for up to 50% off.

Iggy’s Analysis of the Data:

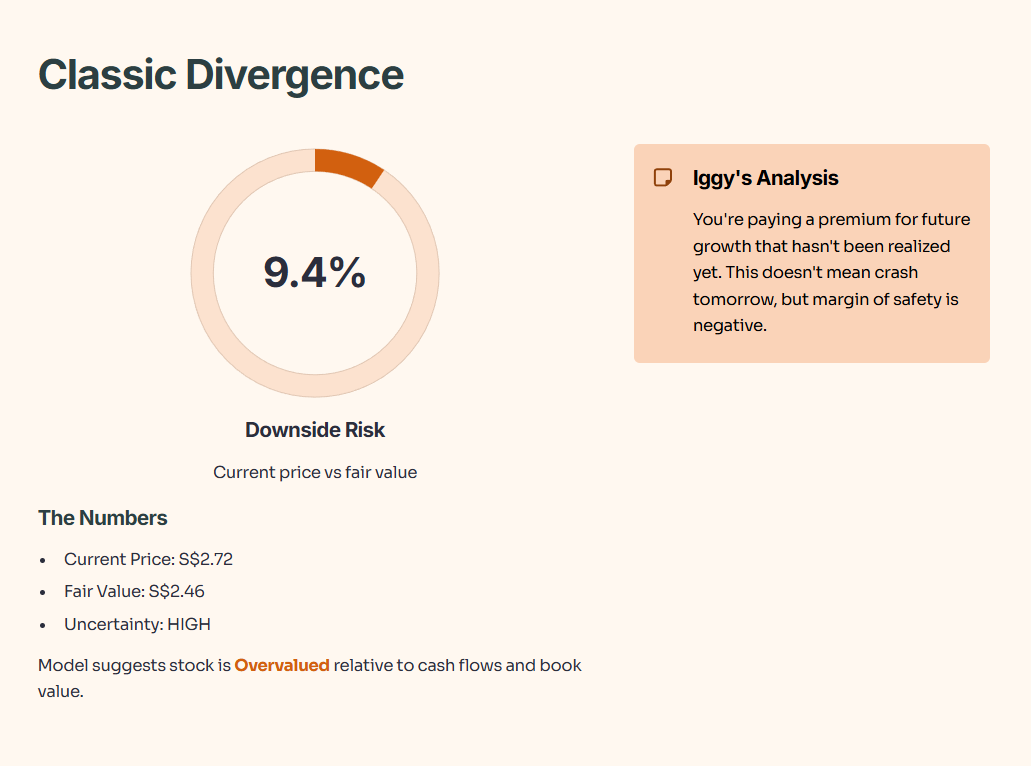

This is a classic “Divergence.” While the market sentiment is bullish, the InvestingPro Fair Value model pegs the intrinsic value at S$2.46.

Current Price: S$2.72

Fair Value: S$2.46

Downside Risk: -9.4%

Uncertainty: HIGH

The model suggests the stock is currently Overvalued relative to its cash flows and book value. This doesn’t mean the price will crash tomorrow, but it means you are paying a premium for future growth that hasn’t been realized yet.

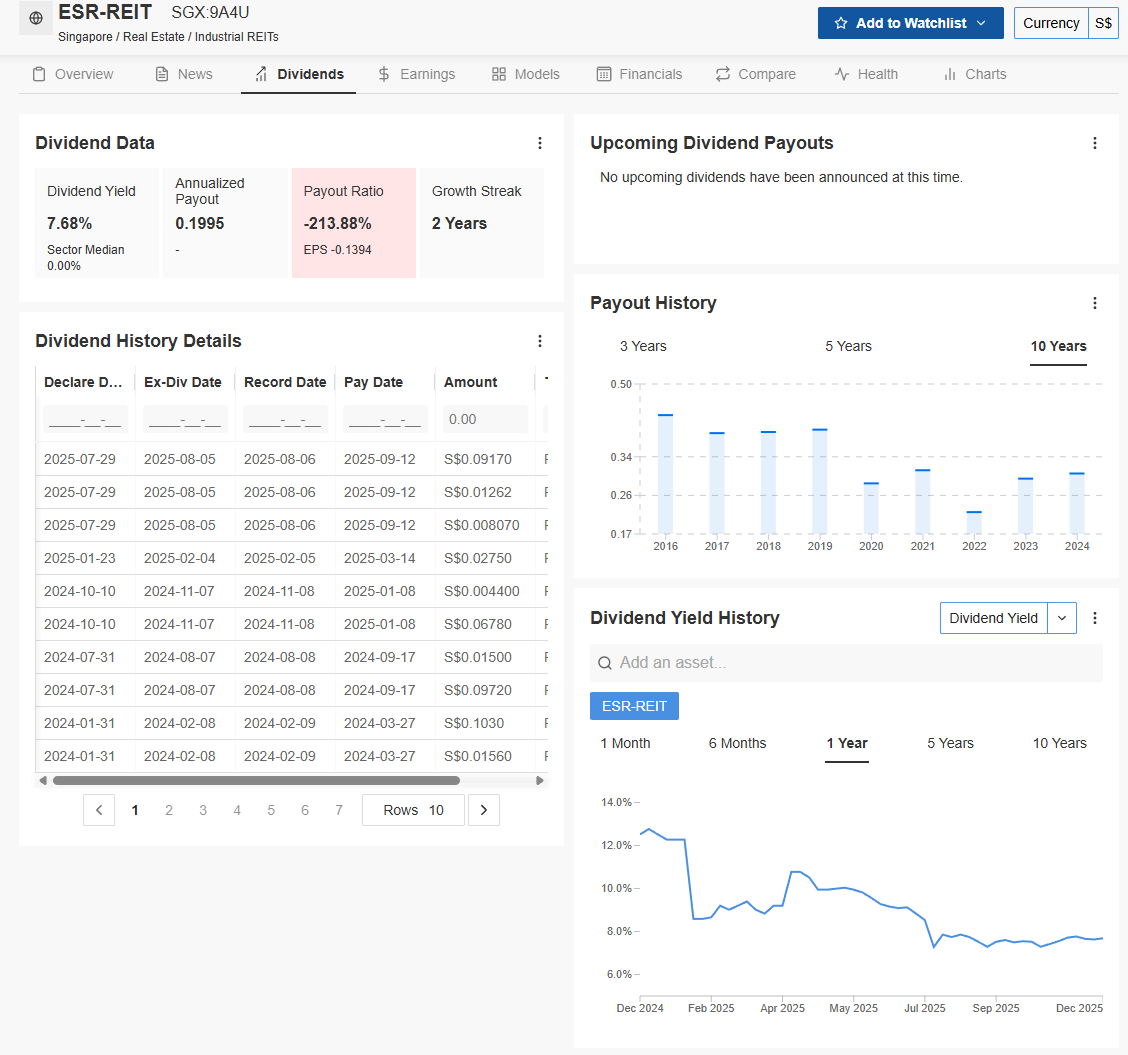

Section 2: The Dividend (The “Meat” for SG Investors)

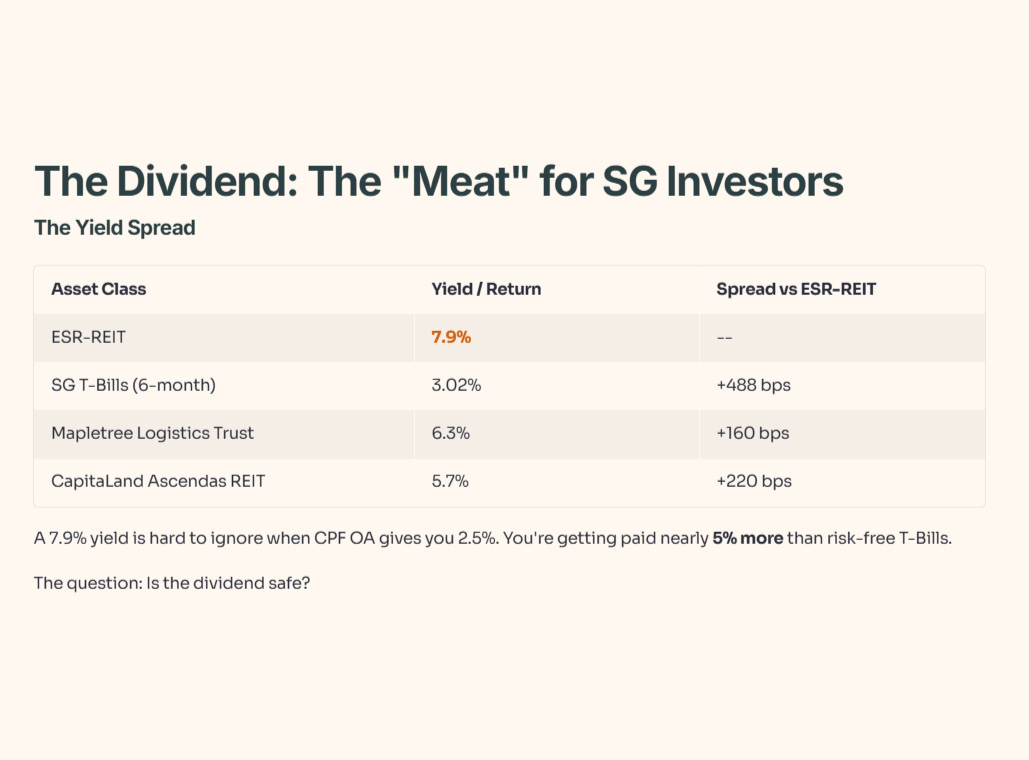

This is why we are here. A 7.9% yield is hard to ignore when CPF OA gives you 2.5%.

The Yield Spread

The spread is massive. You are getting paid nearly 5% more than a risk-free T-Bill to hold this REIT. The question is: Is the dividend safe?

Iggy’s Take:

The payout ratio is supported by “Core” operations (96% of DPU comes from core), which is healthy. However, the NAV per unit has dropped 14% YoY to S$2.61. When a REIT pays a high dividend while its NAV shrinks, you have to be careful—sometimes you are just getting your own capital paid back to you.

Financial Health Check

High yield is often a sign of distress. Is ESR-REIT financially healthy enough to sustain this payout?

Is the dividend actually safe? Let’s look at the health score.

Source: InvestingPro by Investing.com (Data as of Dec 2025). Premium members can use code INVESTINGIGUANA for up to 50% off.

Iggy’s Analysis of the Data:

InvestingPro assigns a Financial Health Score of 3/5 (Good Performance).

Profitability Health: 3/5 (Stable)

Cash Flow Health: 3/5 (Adequate)

Relative Value: 4/5 (This contradicts the Fair Value slightly, suggesting that relative to peers, it might be cheaper, even if intrinsic value is lower).

A score of 3/5 is a “Pass,” but not a “Distinction.” It means the dividend is likely safe for now, but the company doesn’t have a massive buffer to absorb a major shock (like a tenant default).

Section 3: The “3 Good” (Bull Case Arguments)

If you are buying, here is what you are betting on:

The “New Economy” Pivot is Working

Old industrial factories are dying. Logistics and High-Specs buildings are booming. ESR-REIT has aggressively rotated 70% of its portfolio into “New Economy” assets. This is driving positive rental reversions of +9.7% in 1H2025. Landlords have pricing power here.

Debt Cost Management (Surprising Win)

In a high-rate environment, most REITs are seeing interest costs explode. ESR-REIT actually lowered its cost of debt from 3.84% to 3.40% in just 9 months. They refinanced early and smartly. This directly boosts the DPU.

The Japan Angle

The acquisition of the Yatomi facility in Japan gives them exposure to a market with ultra-low interest rates and stable logistics demand. It diversifies them away from the land-scarce limitations of Singapore.

Section 4: The “3 Red Flags” (Bear Case Risks)

If you are avoiding, this is why:

The REC Solar Concentration Risk

Following the Tuas acquisition, REC Solar has become a top tenant. While they have bank guarantees, relying heavily on a single tenant in the manufacturing sector is risky. If REC Solar faces industry headwinds (solar is cyclical), ESR-REIT takes a hit.

Gearing is High (43.3%)

The regulatory limit is 50%, but banks get nervous above 45%. At 43.3%, ESR-REIT has very little “debt headroom” to buy more properties without asking you for more money (Equity Fundraising/Rights Issue).

The “Land Lease Decay” (The Silent Killer)

This is a structural issue with Singapore Industrial REITs. Many assets are on leasehold land (30-60 years). Every year, the land lease ticks down, and the property value theoretically drops. ESR-REIT’s average land lease is 43.5 years. It’s decent, but they have to constantly divest old assets and buy new ones just to run to stand still.

Iggy’s Insight:

This is why the NAV dropped. Fair valuation losses and currency depreciation (AUD/JPY weakness) ate into the book value. You are buying an income stream, but don’t expect the asset value to compound like a freehold property would.

Section 5: The Singaporean Context & Verdict

For the Singaporean investor using SRS or Cash:

Tax Efficiency: As a locally listed REIT, you get the distributions tax-free.

SRS Suitability: High. The 7.9% yield is excellent for tax-deferred compounding in an SRS account, provided you have a long time horizon to ride out volatility.

The Iggy Playbook: What to do?