Why I Disagree With Adam Khoo on 2026 (My "Boring" SG Strategy)

Adam Khoo wants 10% growth. You need 6% reliable cash flow. Here is the mathematical argument for staying home this year.

It is January 2026. The S&P 500 is flirting with valuations that would make a value investor blush. You open YouTube, and the algorithm is screaming at you: “Buy US Tech! Don’t miss the AI Second Wave!”

It is tempting. The Fear of Missing Out (FOMO) is a powerful drug.

But let’s look at the reality of the Singaporean wallet. The cost of living in Singapore isn’t getting cheaper. Your CPF withdrawals are looming. You don’t need a stock that might double in five years but could drop 30% tomorrow. You need a paycheck.

While the media focuses on the glitz of Wall Street, the Straits Times Index (STI) has quietly, defiantly climbed to new highs. The “boring” Singapore market is doing exactly what it was designed to do: generate cash.

If you’re new here, welcome. I’m Iggy, your Singapore-based market analyst. Since October 2025, we’ve produced over 1,300 videos and 400 articles with 1.1 million watch hours. We are also home to a growing community of over 60 YouTube Premium subscribers and 30 paid Substack members.

Quick Housekeeping: If you want the best value, the YouTube Premium Membership (S$9/mth) bundles these deep-dive articles with the podcast videos. Substack alone is US$6, so the bundle is the “smart money” move.

Now, let’s get to the numbers.

In This Article:

• The Two Games: Growth vs. Income

• The Banking Fortress: DBS vs. The Field

• Data Check: Is DBS Too Expensive?

• The REIT Revival: Playing the Rate Cut Lag

• The CPF & Policy Anchor: The S$8,000 Reality

• The 2026 Investor’s Playbook

The Two Games: Growth vs. Income

We need to address the elephant in the room. Adam Khoo is bullish on America, and the data supports him. The US market has tailwinds. Earnings will grow. Rates are projected to fall further in 2026. Single-digit returns are still returns.

Watch his two videos here:

But he is playing a different game than you are.

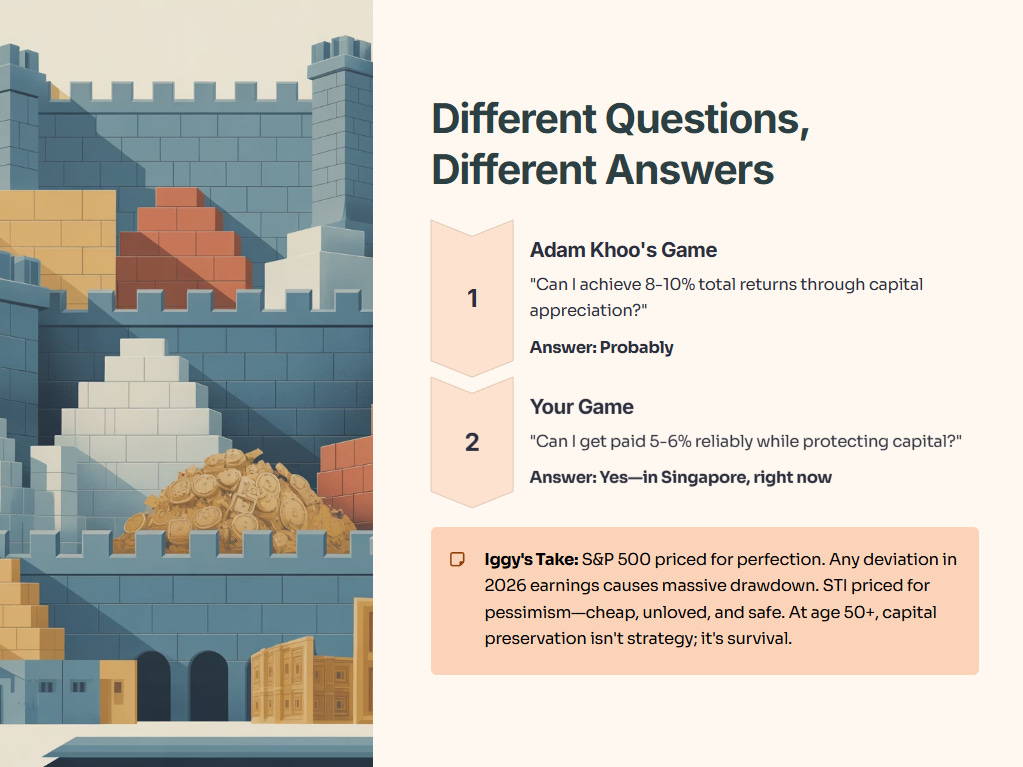

He is asking: “Can I achieve 8–10% total returns through capital appreciation?” You are asking: “Can I get paid 5–6% reliably while protecting my capital?”

For Khoo’s question, the answer is “probably.” For yours, the answer is “yes—in Singapore, right now.”

Iggy’s Take: The S&P 500 is priced for perfection. Any deviation in the 2026 earnings forecast causes a massive drawdown. The STI is priced for pessimism. It’s cheap, it’s unloved, and that is exactly where the safety lies. I am not anti-US, but at age 50+, capital preservation isn’t just a strategy; it’s a survival mechanism.

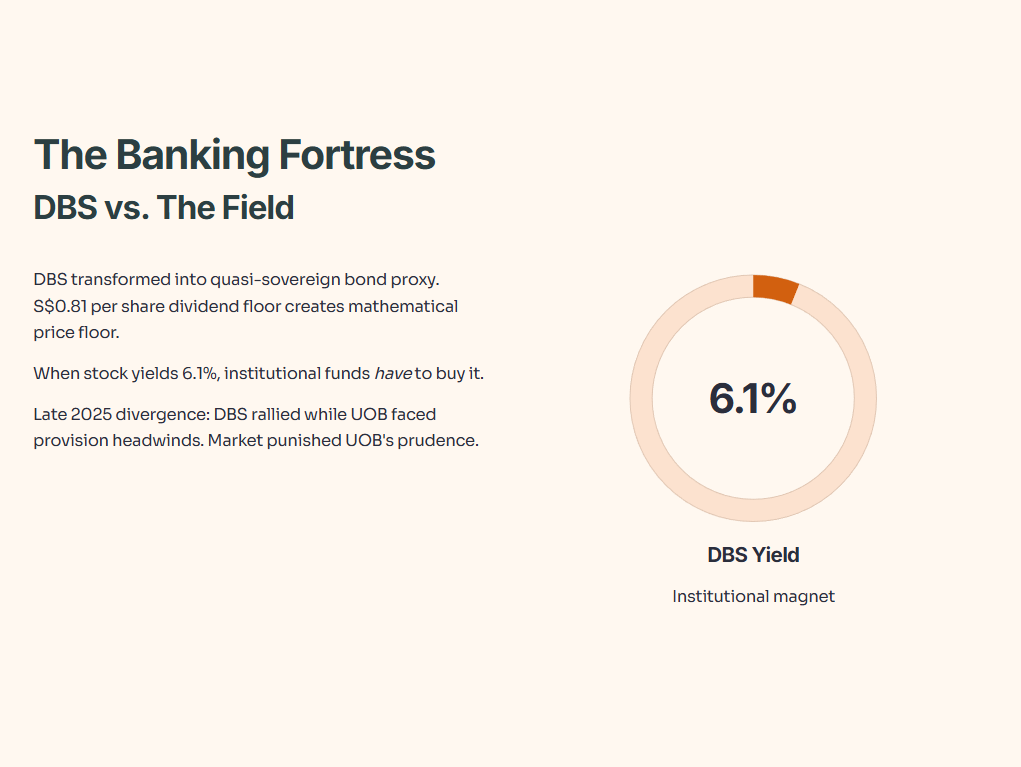

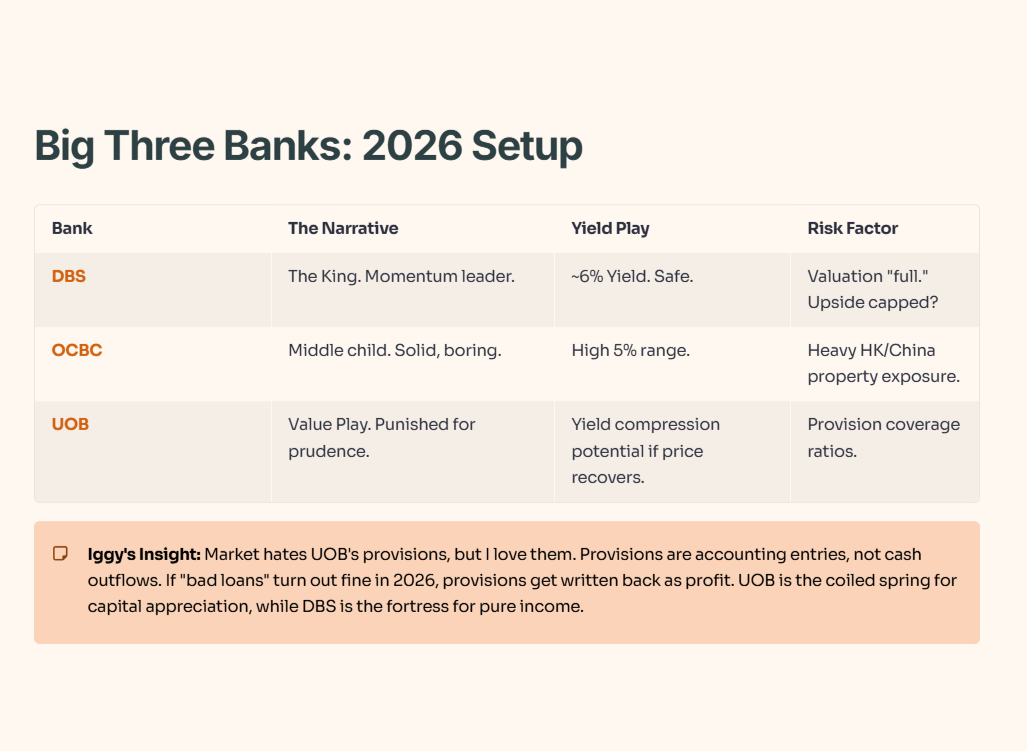

The Banking Fortress: DBS vs. The Field

The cornerstone of the 2026 Singapore portfolio remains the banks. But not all banks are created equal.

DBS has effectively transformed into a quasi-sovereign bond proxy. The commitment to the S$0.81 per share dividend floor (implied annualized) creates a mathematical floor for the stock price. When a stock yields 6.1%, institutional funds have to buy it.

However, we saw divergence in late 2025. While DBS rallied, UOB faced headwinds regarding provisions. When a bank increases provisions, they are essentially setting aside money for loans they fear might go bad. The market punished UOB for this prudence, dragging its price down relative to earnings.

Here is the breakdown of the Big Three setup for 2026:

Iggy’s Insight: The market hates UOB’s provisions, but I love them. Why? Because provisions are accounting entries, not cash outflows. If those “bad loans” turn out to be fine in 2026, those provisions get written back as profit. UOB is the coiled spring here for capital appreciation, while DBS is the fortress for pure income.

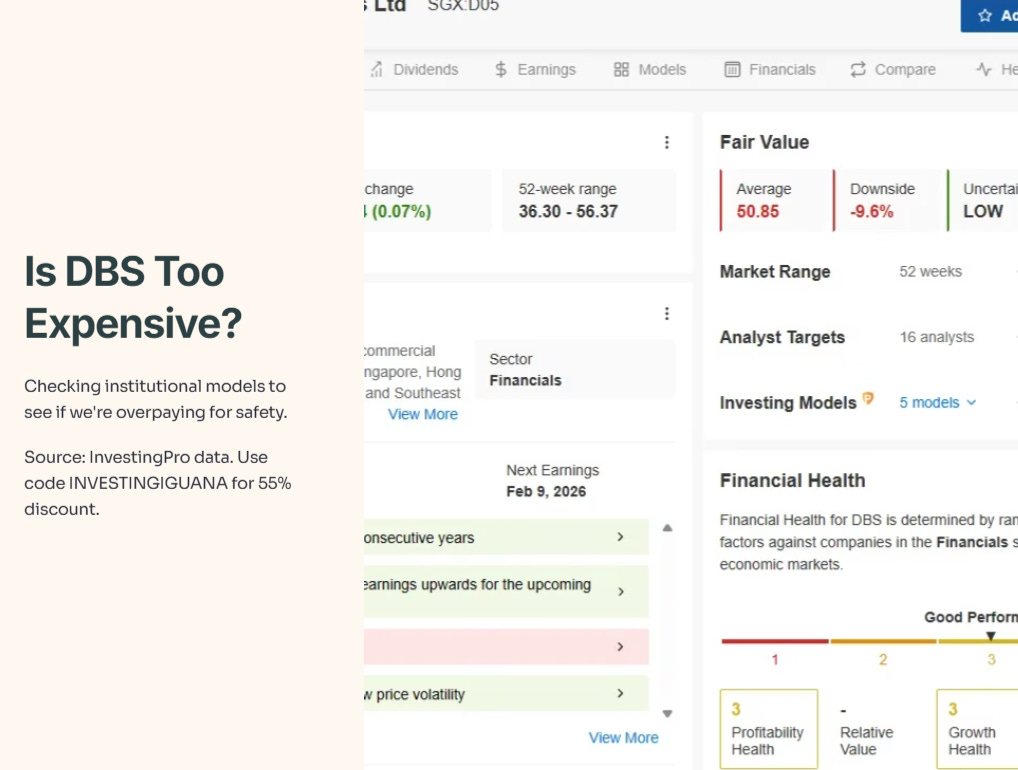

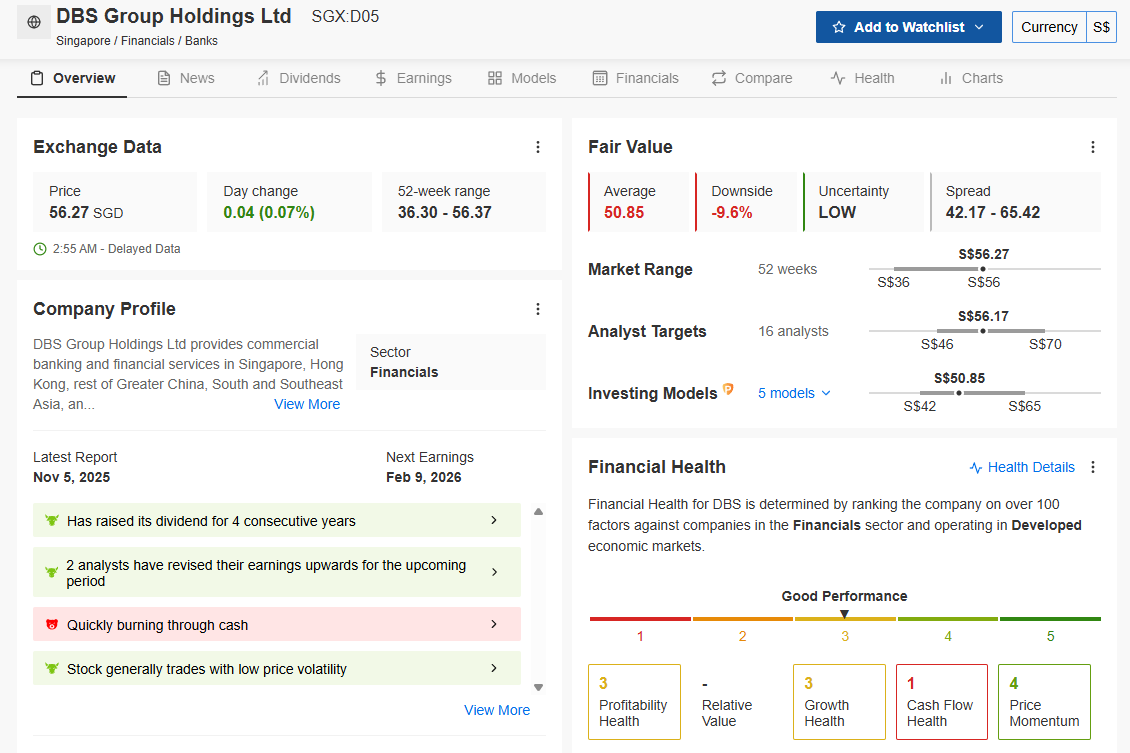

Data Check: Is DBS Too Expensive?

I don’t just guess at valuations. I check the institutional models to see if we are overpaying for safety.

I don’t just guess at valuations. I check the institutional models to see if we are overpaying for safety.

Source: InvestingPro data. Unlock these institutional tools for yourself: Use code INVESTINGIGUANA for an exclusive 55% discount to kickstart 2026.

Iggy’s Analysis: The models are flashing yellow. InvestingPro flags a Fair Value of S$50.85, suggesting nearly 10% downside from the current S$56.27 price.

Also, notice the red flag: “Quickly burning through cash” (Cash Flow Health: 1/5). Don’t panic—this is often a false negative for banks because lending money counts as “cash outflow.” However, combined with the premium valuation, it confirms my thesis: You aren’t buying DBS for a price jump anymore. The “easy money” capital gains are gone. You are holding purely for that dividend safety. If you are looking to enter, you must wait for a pullback closer to that S$50-52 range.

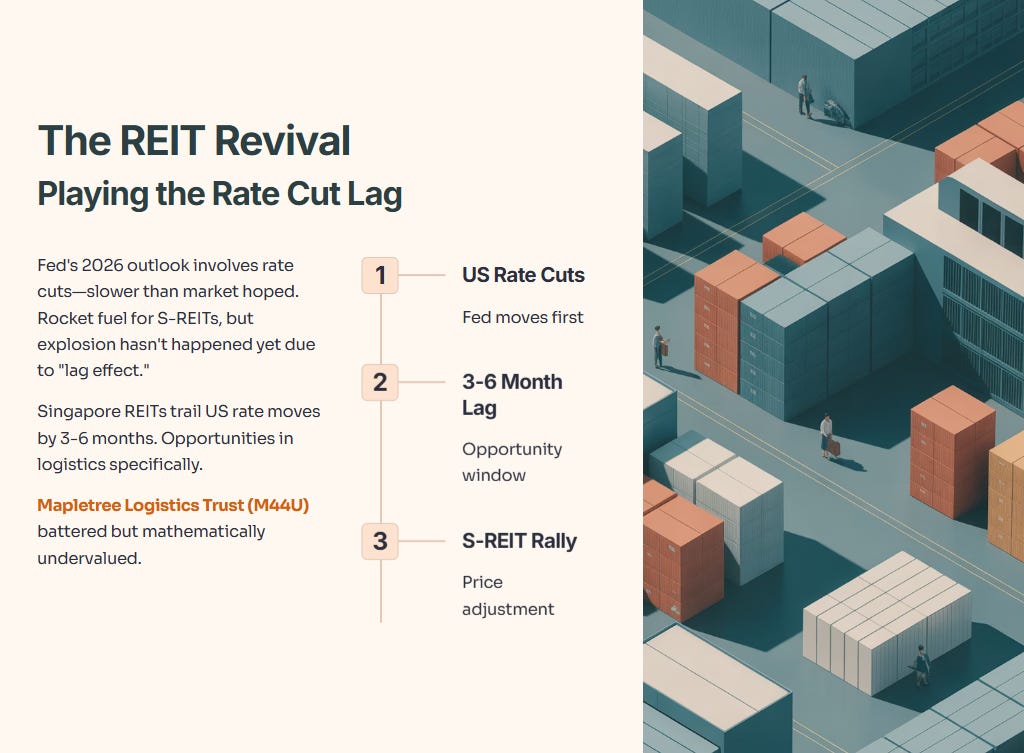

The REIT Revival: Playing the Rate Cut Lag

The Fed’s outlook for 2026 involves rate cuts, albeit slower than the market hoped. This is rocket fuel for S-REITs, but the explosion hasn’t happened yet because of the “lag effect.”

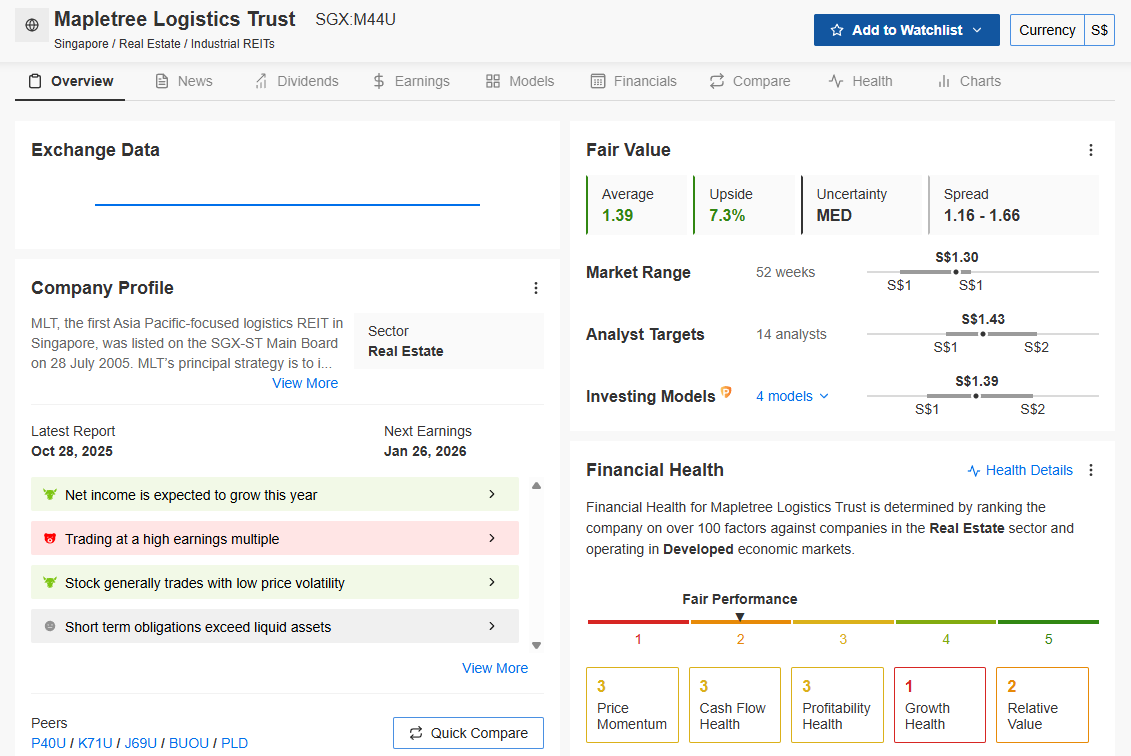

Singapore REITs usually trail US rate moves by 3-6 months. We are seeing opportunities in logistics specifically. Mapletree Logistics Trust (M44U) has been battered, but the math suggests it is now mathematically undervalued.

Data Check: REIT Financial Strength

Are these REITs yield traps, or just on sale? Let’s look at the balance sheets.

Source: InvestingPro data. Unlock these institutional tools for yourself: Use code INVESTINGIGUANA for an exclusive 55% discount to kickstart 2026.

Iggy’s Analysis: This is a classic “Value Play” setup. The model assigns M44U a Fair Value of S$1.39, implying a conservative 6.5% upside from the current S$1.31 level.

But look at the Health Scores. “Growth Health” is a 1 (Red).

Here is the Alpha: The model hates the growth narrative here, and frankly, it’s right. There is no massive revenue explosion coming. We aren’t buying M44U for growth. We are buying it because it is trading below its intrinsic value (Fair Performance score of 2/5 reflects the current struggle). You are buying a dollar for 94 cents, collecting the dividend while you wait for the unit price to drift back up to that S$1.39 fair value anchor.

The CPF & Policy Anchor: The S$8,000 Reality