Why Keppel’s Profit Silence Threatens Your Dividend | SGX Daily Pulse April 23 | 🦖EP1564

When STI tests 5,000 on ceasefire news but Keppel reports “slightly lower” with no figures and 5.1x Net Debt/EBITDA

THURSDAY OPEN

Earnings and dividend season is picking up on the SGX, and Thursday is shaping up to be a reporting day worth paying attention to. A handful of names have crossed my monitoring threshold this week, and today I am running the forensic numbers on Keppel, CapitaLand China Trust, City Developments, and Oiltek.

Some of these updates raise questions I want to work through carefully. Others are cleaner than the headlines suggest. Either way, this is the kind of reporting window where the real story tends to sit one layer below what management puts in the announcement. Let us get into it.

In This Article:

Market Snapshot

The Audit Keppel Ltd SGX BN4 Watchlist Trigger

The Audit CapitaLand China Trust SGX AU8U Yield Trap

The Audit City Developments Ltd SGX C09 Strategic Neutral

The Audit Oiltek International SGX HQU Watchlist Trigger

Analyst Chatter

Watchlist And Yield Spread

Iggys Take The Bottom Line

Iggys Forensic Disclaimer

MARKET SNAPSHOT

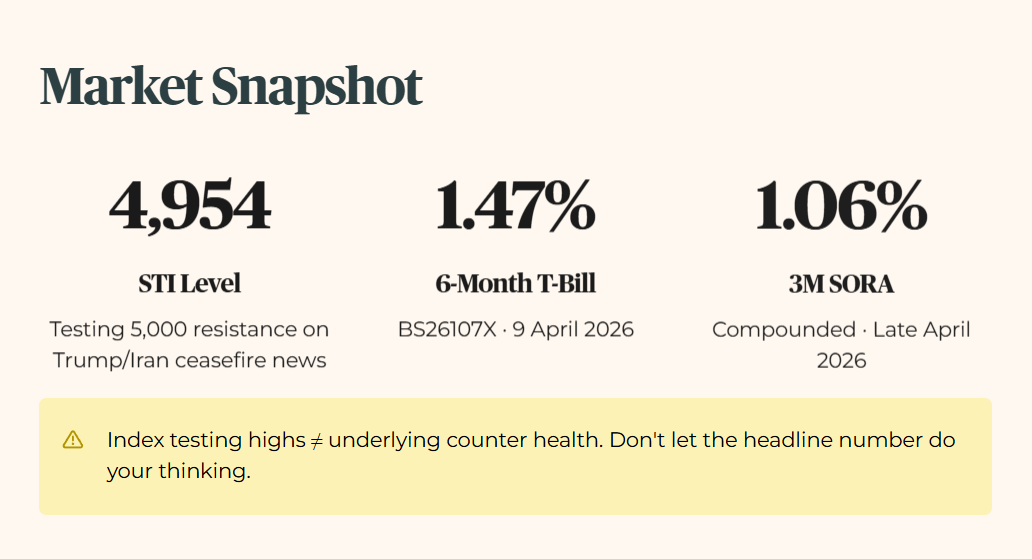

STI Level: 4,953.62 (Live Spot, 23 April 2026). The index is testing the 5,000 resistance zone on the back of Trump/Iran ceasefire news. This creates a potentially dangerous divergence between index price and underlying counter health. Do not let the headline number do your thinking for you.

6-Month T-Bill: 1.47% (BS26107X, 9 April 2026). Today’s BS26108W auction results are still pending at time of publication. I will update the Macro Dashboard once the cut-off yield is confirmed.

3-Month Compounded SORA: approximately 1.06% (Late April 2026 Spot).

iEdge S-REIT Index: Level not confirmed at publication. Last benchmark sat near 1,056. Monitor the Macro Dashboard for the live reading.

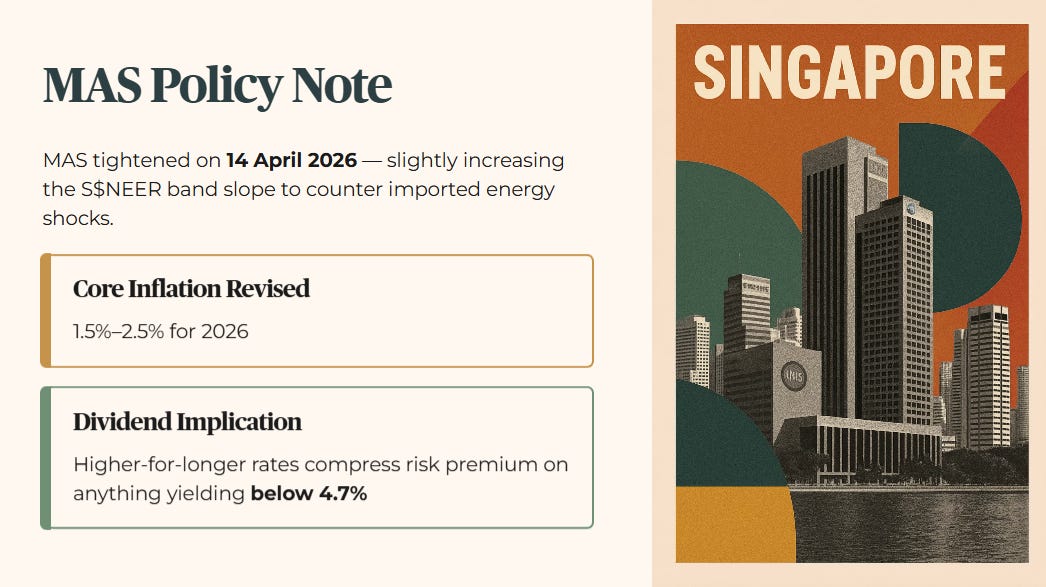

MAS Policy Note: MAS tightened monetary policy on 14 April 2026, slightly increasing the slope of the S$NEER band to counter imported energy shocks. Core inflation forecast has been revised upward to 1.5%–2.5% for 2026. For dividend investors, this matters. A higher-for-longer Singapore rate environment compresses the risk premium on anything yielding below 4.7%.

THE AUDIT

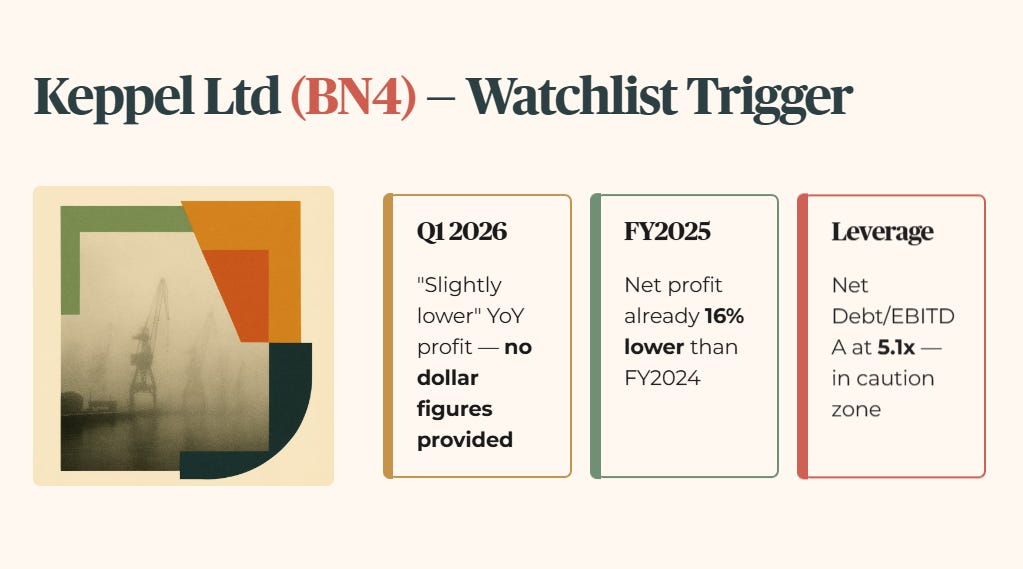

KEPPEL LTD (SGX: BN4) — WATCHLIST TRIGGER

This is where reporting transparency dies and the dividend math gets murky.

Keppel reported “slightly lower” year-on-year net profit for Q1 2026, citing lower real estate contributions and fair value losses from non-core assets. No specific dollar figures were provided in the SGX Business Update.

FY2025 net profit is already 16% lower than FY2024. Net Debt/EBITDA stands at 5.1x, inclusive of the non-core portfolio and discontinued operations. That sits in my caution zone. The absence of hard numbers this quarter suggests continued earnings erosion, not a clean recovery.

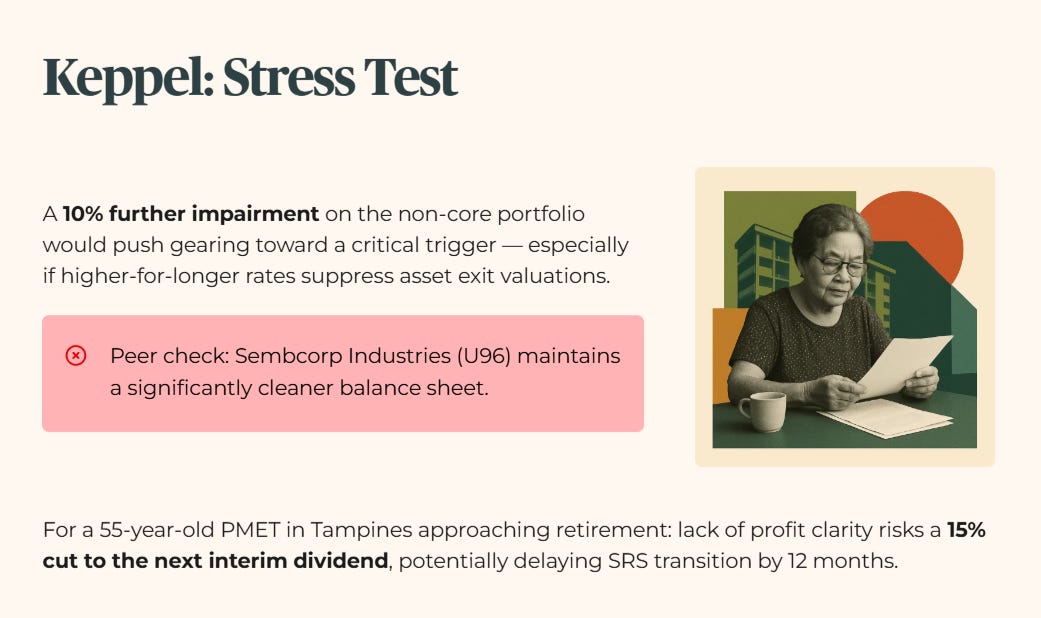

For peer context, Sembcorp Industries (SGX: U96) maintains a significantly cleaner reported balance sheet and passes the forensic floor that Keppel’s current reporting fog is obscuring.

Forward stress test: a 10% further impairment on the non-core portfolio would likely push gearing toward a critical watchlist trigger, particularly if higher-for-longer interest rates continue to suppress asset exit valuations.

For a 55-year-old PMET in Tampines approaching retirement with CPF OA invested in blue chips, the lack of profit clarity means a potential 15% cut to the next interim dividend. That could delay their retirement SRS transition by 12 months.

Forensic Stance: Watchlist Trigger.

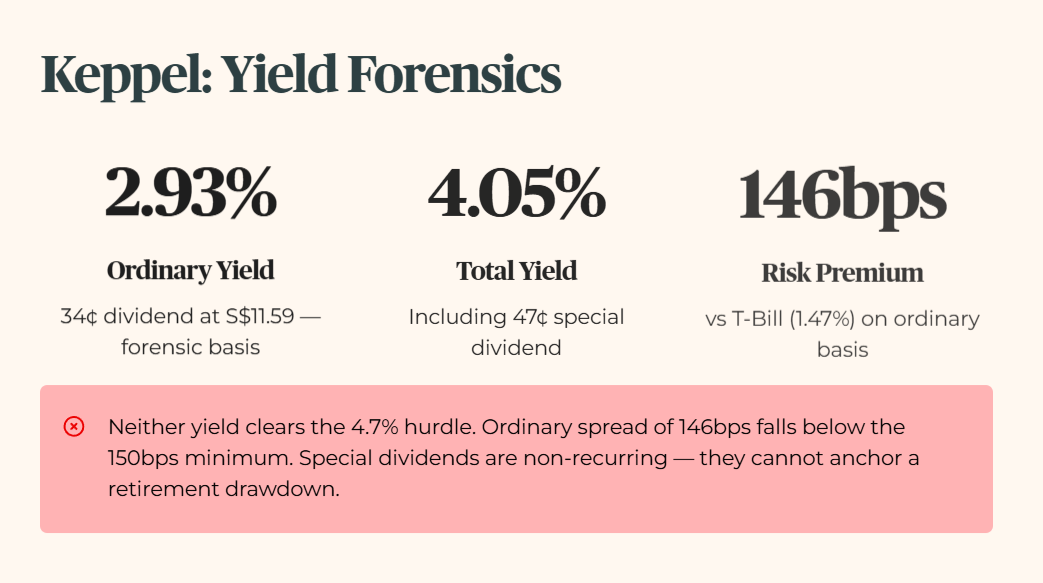

Yield Note: Based on FY2025 ordinary dividend of 34 cents, yield at S$11.59 is 2.93%. Based on total dividend of 47 cents including special, yield is 4.05%. Neither figure clears the 4.7% hurdle. Risk premium against the 6-month T-Bill (1.47%) is 158 basis points on the total dividend basis only. On ordinary dividend, the spread collapses to 146 basis points, which is below my 150 basis point minimum. I apply the ordinary dividend as the forensic basis. Special dividends are non-recurring and cannot anchor a retirement drawdown.

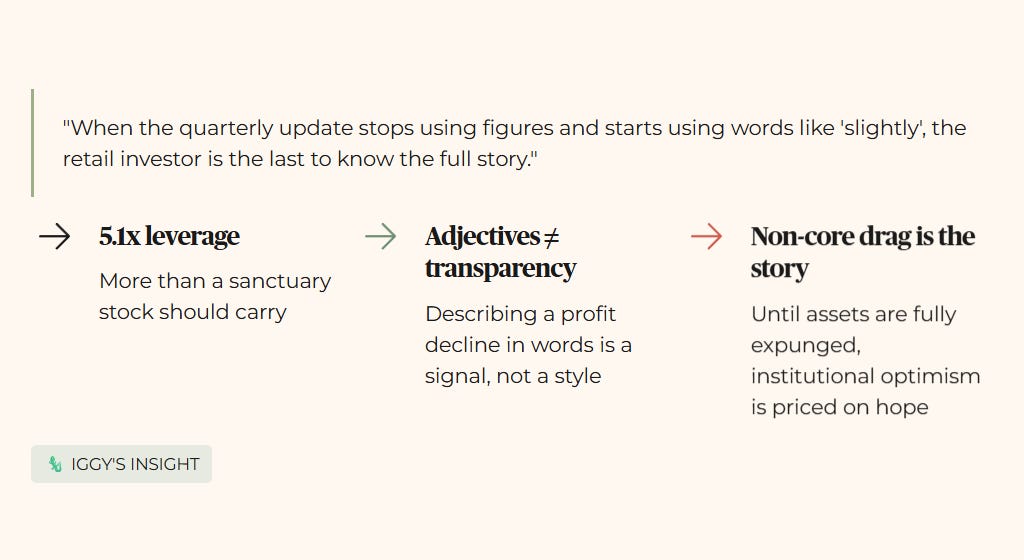

🦎 Iggy’s Insight At 5.1x Net Debt/EBITDA, Keppel is carrying more leverage than a sanctuary stock should. Management’s decision to describe a profit decline using adjectives instead of numbers is not a communication style. It is a signal. When the quarterly update stops using figures and starts using words like “slightly”, the retail investor is the last to know the full story. The non-core drag is not a footnote. It is the story. Until those assets are fully expunged without further fair value hits, the institutional optimism is priced on hope, not forensics.

CAPITALAND CHINA TRUST (SGX: AU8U) — YIELD TRAP

The China recovery narrative has hit the brick wall of reality.

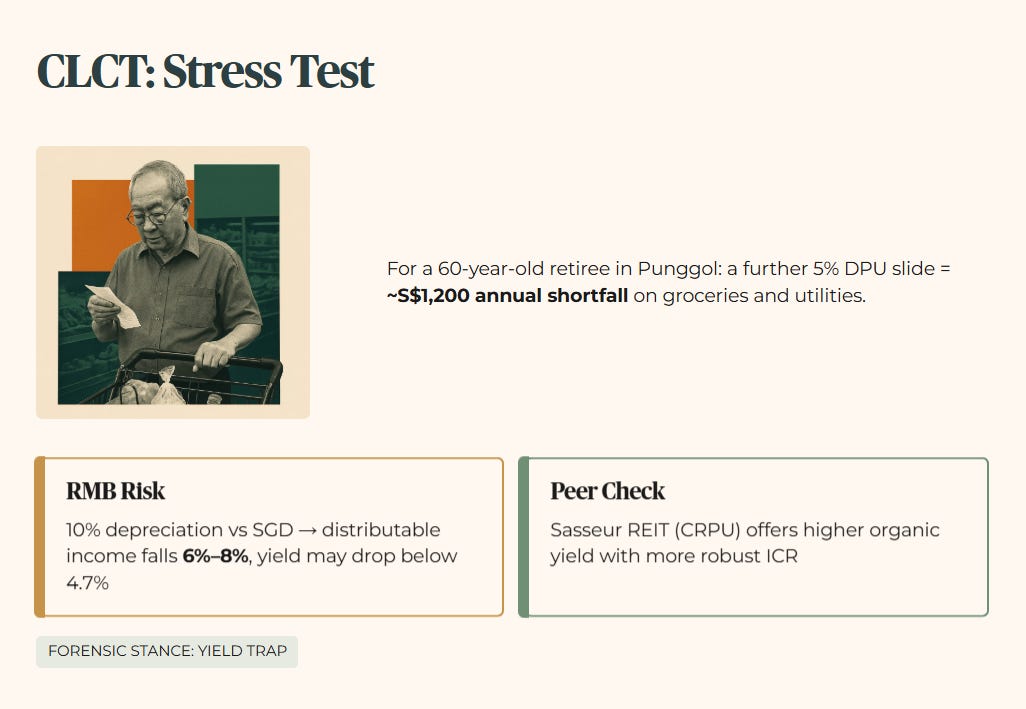

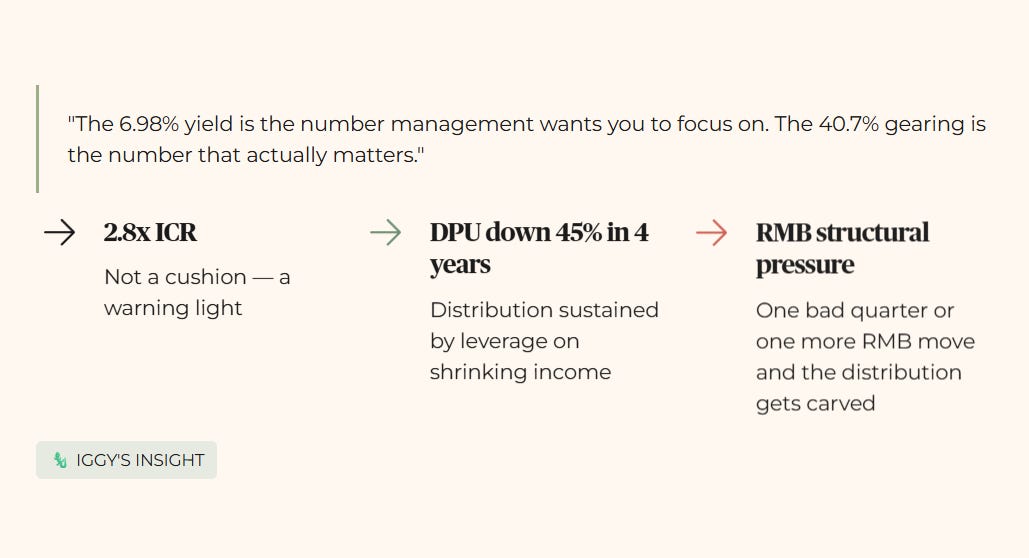

Q1 2026 Net Property Income fell 3.5% year-on-year to 282.4 million yuan, largely due to the absence of income from the divested CapitaMall Yuhuating. FY2025 DPU is confirmed at 4.82 cents, representing a 45% decline from 8.73 cents in 2021. Gearing stands at 40.7%, well above my 35% ceiling. ICR is 2.8x for FY2025, below my 4.0x minimum.

At the live price of S$0.690, yield is 6.98% on FY2025 DPU. That clears the 4.7% hurdle on paper. It does not clear my structural test. Gearing at 40.7% and ICR at 2.8x mean that yield is being paid on a leveraged, currency-exposed base with a deteriorating income floor.

For peer context, Sasseur REIT (SGX: CRPU) currently offers a higher organic yield with a more robust ICR, and passes the 3x safety buffer that CLCT is struggling to maintain.

Forward stress test: a 10% depreciation of the RMB against the SGD would slash distributable income by an estimated 6%–8%, potentially dropping the effective yield below 4.7%, triggered by continued PBOC monetary easing.

For a 60-year-old retiree in Punggol managing an SRS drawdown for living expenses, a further 5% DPU slide represents approximately S$1,200 in annual shortfall against grocery and utility costs.

Forensic Stance: Yield Trap.

🦎 Iggy’s Insight 2.8x ICR is not a cushion. It is a warning light. CLCT’s yield looks attractive until you run the full forensic stack: gearing above ceiling, ICR below floor, DPU down 45% in four years, and the RMB carrying structural depreciation pressure. The distribution is not being earned cleanly. It is being sustained by leverage on assets whose income is shrinking. One bad quarter or one more RMB move and the distribution gets carved. The 6.98% yield is the number management wants you to focus on. The 40.7% gearing is the number that actually matters.

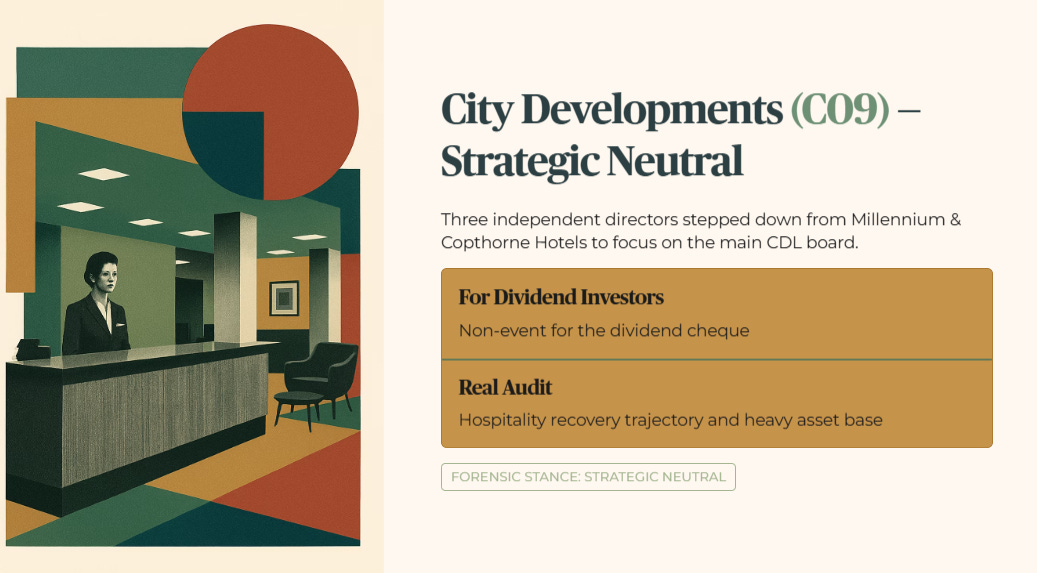

CITY DEVELOPMENTS LTD (SGX: C09) — STRATEGIC NEUTRAL

Three independent directors stepped down from the board of Millennium & Copthorne Hotels to focus on the main CDL board. For a 45-year-old HDB owner in Jurong supplementing salary income with dividends, this is a non-event for the dividend cheque. It is a necessary step for management focus. The real audit remains on the hospitality sector’s recovery trajectory and the group’s heavy asset base.

Forensic Stance: Strategic Neutral.

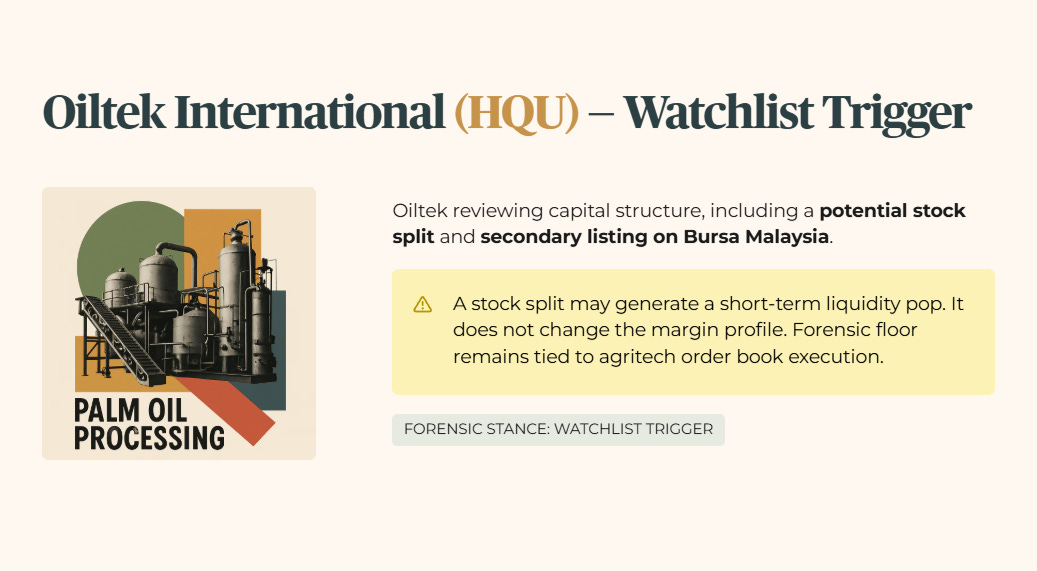

OILTEK INTERNATIONAL (SGX: HQU) — WATCHLIST TRIGGER

Oiltek is actively reviewing its capital structure, including a potential stock split and secondary listing on Bursa Malaysia. For a 50-year-old investor in Ang Mo Kio managing an SRS portfolio, a stock split may generate a short-term liquidity pop. But the forensic floor remains tied to the execution of the agritech order book. A capital structure review does not change the margin profile. Forensic Stance: Watchlist Trigger.

ANALYST CHATTER

Several institutional houses remain Neutral on Keppel, citing the transition to a global asset manager as a long-term play.

Iggy’s filter: the long-term play cannot be audited while Net Debt/EBITDA sits at 5.1x. Until the non-core assets are fully expunged without further fair value hits, the institutional optimism is ignoring the forensic drag.

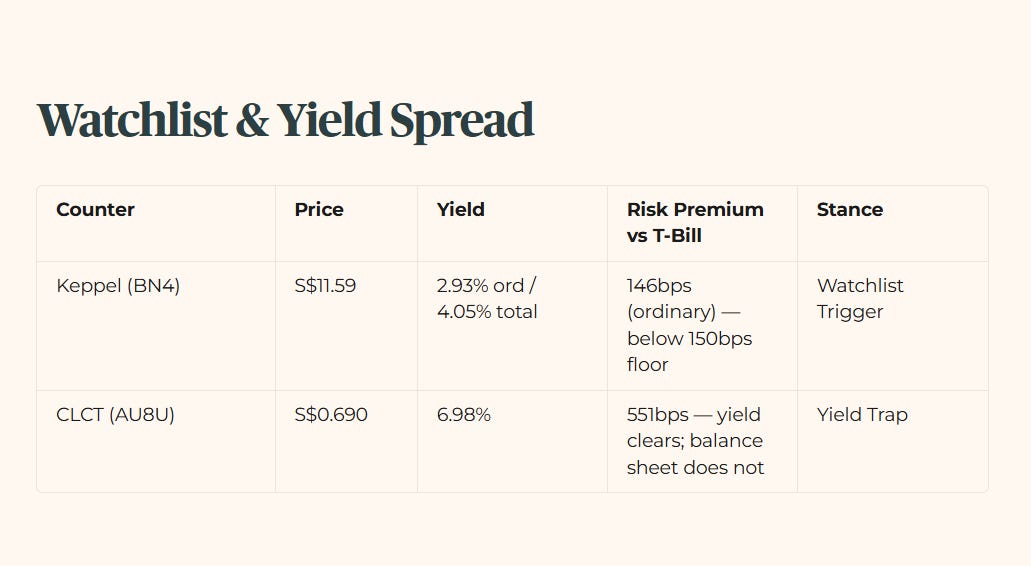

WATCHLIST AND YIELD SPREAD

Keppel Ltd (SGX: BN4): Live price S$11.59. Ordinary dividend yield 2.93%. Total dividend yield 4.05%. Forensic basis: ordinary yield. Risk premium against T-Bill (1.47%): 146 basis points on ordinary basis. Below my 150 basis point minimum.

CapitaLand China Trust (SGX: AU8U): Live price S$0.690. FY2025 DPU 4.82 cents. Yield 6.98%. Risk premium against T-Bill (1.47%): 551 basis points. Yield clears the hurdle. The balance sheet does not.

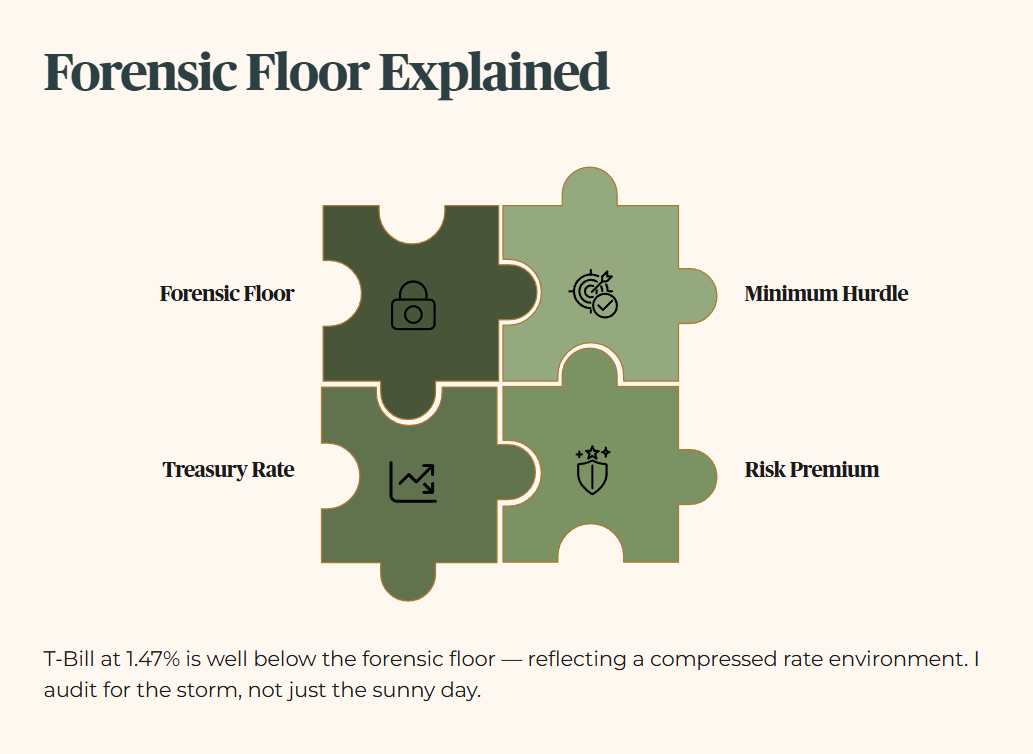

Stress-Test Note: My forensic floor holds at 3.2%. The T-Bill at 1.47% is well below that floor, which reflects a compressed near-term rate environment. I audit for the storm, not just the sunny day. The minimum yield hurdle remains 4.7%, being the 3.2% floor plus 150 basis points of mandatory risk premium.

The Window Is Already Open

The Window Closes Fast. In this market, the difference between a “Sanctuary” and a “Yield Trap” is decided in a single trading session. By the time this analysis reaches you as a free subscriber, the entry window Iggy identified has already opened — and often closed..

Iggy’s Elite Investors don’t just get the report earlier. They get it when the numbers still matter — zero-day forensic breakdowns, the full “Red Zone” watchlist, and institutional-grade cheatsheets at the moment the setup is live, not after the market has already priced it in.

For S$9/month — less than a kopi and kaya toast set at Raffles Place — you stop being the Exit Liquidity and start being the Analyst.

IGGY’S TAKE: THE BOTTOM LINE

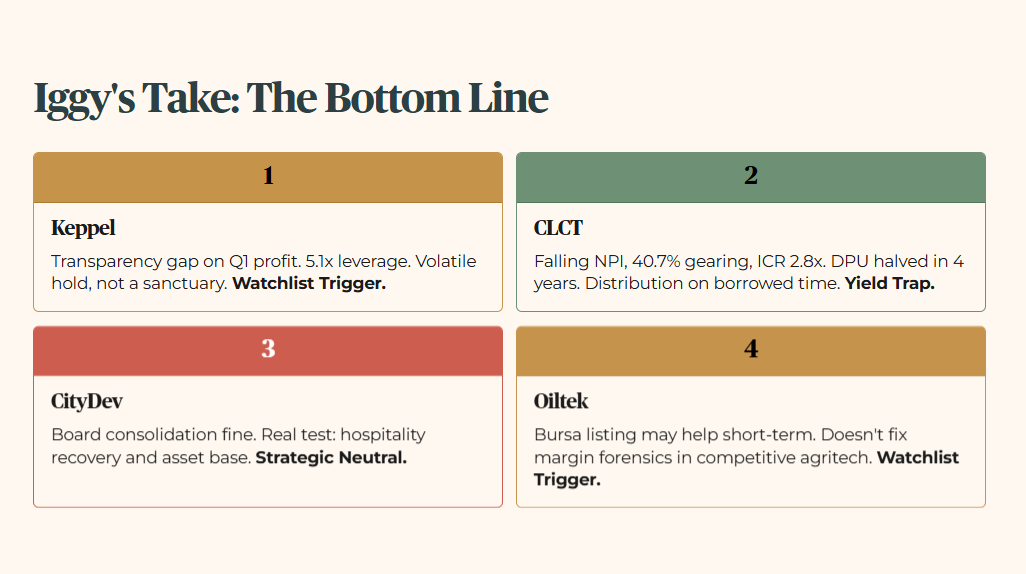

Keppel: the transparency gap on Q1 profit is a major concern. When management stops using numbers and starts using adjectives, it is time to tighten the monitoring. At 5.1x Net Debt/EBITDA, this is a volatile hold, not a sanctuary. Watchlist Trigger.

CLCT: a textbook yield trap. Falling NPI, 40.7% gearing, and an ICR of only 2.8x. The DPU has halved in four years. The distribution is being paid on borrowed time. Yield Trap.

CityDev: board consolidation is fine. The real test remains on hospitality recovery and the asset base. Strategic Neutral.

Oiltek: a potential Bursa listing may help the share price short-term. It does not fix the forensic requirement for higher margins in a competitive agritech market. Watchlist Trigger.

Heartland Pairing: compare the stability of a mature Tampines flat to a Punggol BTO with rising service and conservancy charges. Tampines is the sanctuary. Punggol is the high-leverage growth bet. That is what CLCT has become. The day the numbers disappear from a quarterly update is the day you tighten your forensic grip.

Iggy’s Forensic Disclaimer

This content is produced for educational and informational purposes only. I am not a financial advisor — I am a retail investor who applies forensic analysis to my own portfolio and shares that process publicly. Nothing here constitutes a recommendation to buy, sell, or hold any security, and no specific target prices or personalised financial advice are offered. Stocks assessed under Iggy’s Forensic Yield Standard are benchmarked against a 4.7% minimum yield hurdle; stocks flagged as Growth Watch fall below this threshold but demonstrate clean balance sheet metrics and an identifiable growth catalyst — these carry a materially different risk profile and are not suitable as yield replacements for income-dependent investors. All data is sourced from public filings and verified sources; where data is unverified it is explicitly flagged. All investments carry risk, including the potential loss of principal, and past performance is not indicative of future results. If you are making investment decisions involving CPF, SRS, or personal capital, please conduct your own due diligence or consult a MAS-licensed financial adviser before committing funds.