Why Maybank Loves Sheng Siong (And Why You Should Too): Singapore’s Defensive Supermarket Play That’s Banking on Population Growth

Unlocking the Secrets of Sheng Siong: How This Supermarket Giant Thrives—and Why It’s Becoming a Top Pick for Growth in Singapore

Editor’s Note: This post has been updated on October 19, 2025 to ensure it is fresh and accurate, and now includes the latest analysis on Sheng Siong’s key growth drivers and competitive position.

Maybank’s bullish stance on Sheng Siong isn’t just another analyst call—it’s a calculated bet on Singapore’s changing demographics and the supermarket chain’s ability to capture market share during a competitor’s retreat.

The investment thesis becomes crystal clear when you examine the convergence of three powerful tailwinds hitting Sheng Siong simultaneously. Singapore’s construction boom is drawing foreign workers who need affordable groceries, government vouchers are directly boosting supermarket spending, and a major competitor just sold out to focus elsewhere. For Singapore investors seeking defensive plays with growth potential, this setup deserves serious attention.

In This Article:

• The Foreign Worker Windfall: Construction Boom Meets Grocery Demand

• Government Vouchers: Direct Fuel for Supermarket Sales

• Market Share Opportunity: DFI’s Strategic Retreat Creates Opening

• Financial Performance: Margin Expansion Through Operational Excellence

• Expansion Pipeline: HDB Tenders and Strategic Site Selection

• Competitive Moat: Fresh Produce and Operational Efficiency

• Iggy’s Take: How Sheng Siong Fits in Your CPF/SRS Portfolio

• Valuation and Investment Outlook

• The Bottom Line: Defensive Growth in an Attractive MarketThe Foreign Worker Windfall: Construction Boom Meets Grocery Demand

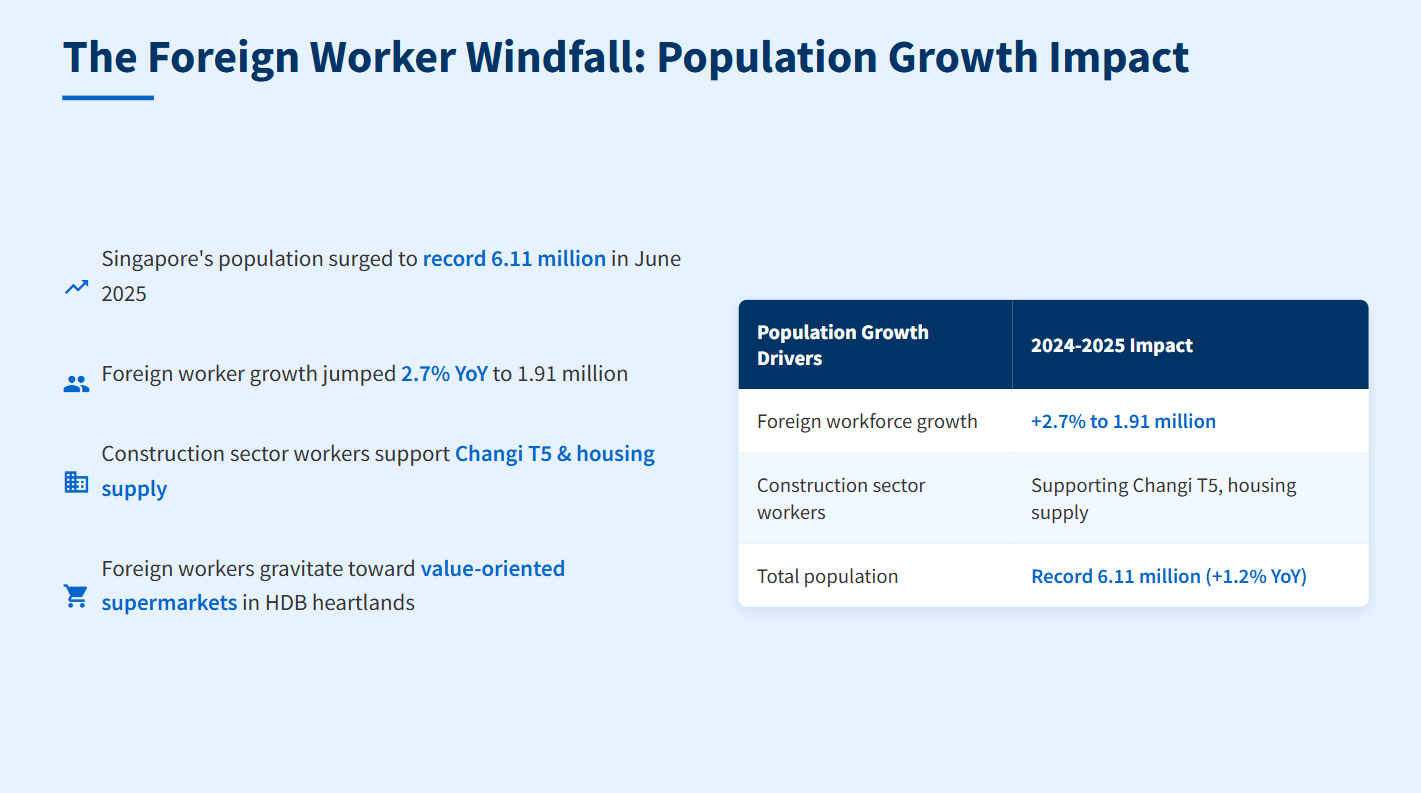

Singapore’s population surged to a record 6.11 million in June 2025, driven primarily by foreign worker growth that jumped 2.7% year-over-year to 1.91 million. This isn’t random population growth—it’s strategically targeted expansion in construction, marine shipyard, and processing sectors supporting mega-infrastructure projects like Changi Terminal 5 and the ramping up of housing supply.

Here’s why this matters for Sheng Siong’s bottom line: foreign workers, particularly those in construction earning moderate wages, gravitate toward value-oriented supermarkets located in HDB heartlands—exactly Sheng Siong’s sweet spot. The supermarket operator has built its business model around serving these heartland communities with affordable groceries and fresh produce, positioning itself perfectly to capture this demographic expansion.

The construction sector itself is projected to grow 6.5% in 2025, up from 4% in 2024, with contracts awarded surging 55% in the third quarter of 2024. This sustained construction activity ensures continued foreign worker influx, creating a reliable customer base for Sheng Siong’s expansion strategy.

Government Vouchers: Direct Fuel for Supermarket Sales

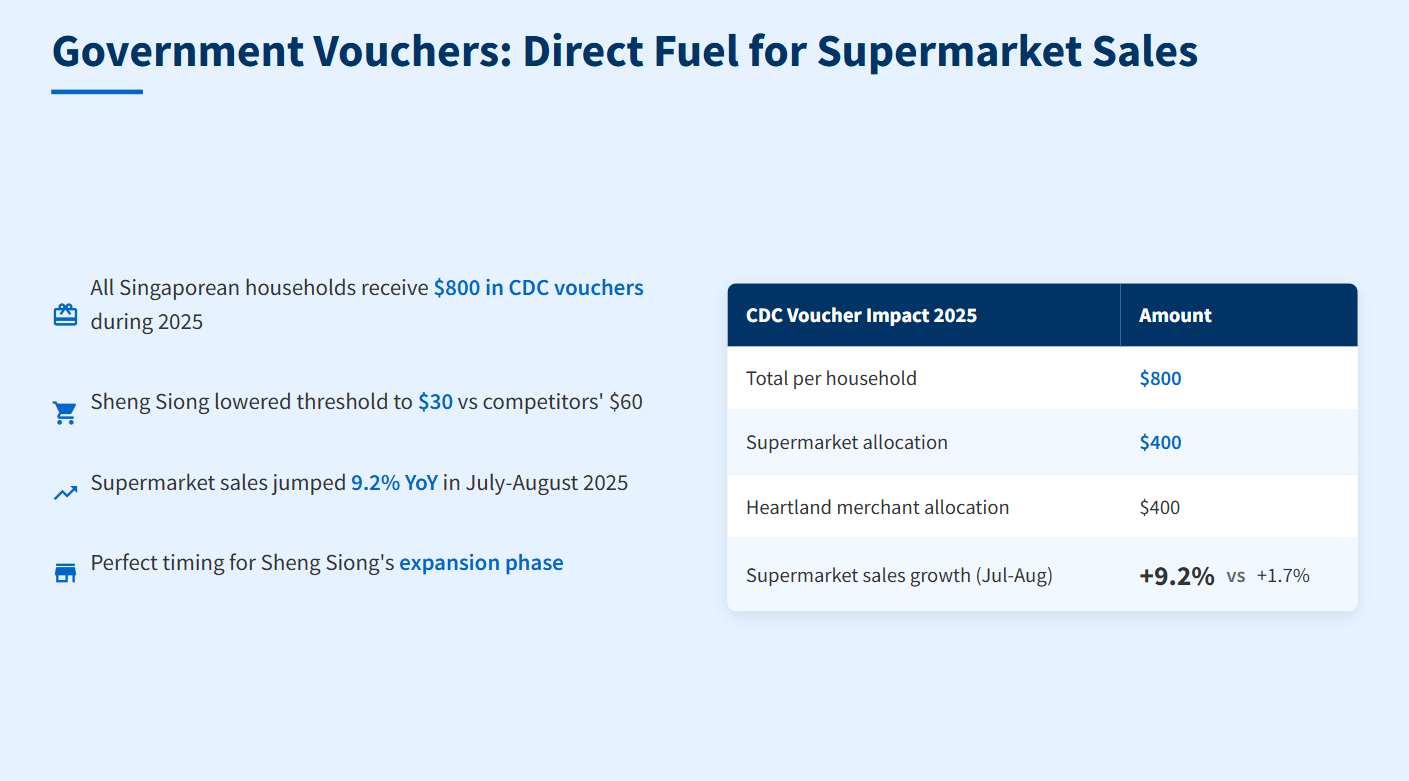

Singapore’s government has essentially handed supermarket operators a gift through the CDC voucher scheme. All Singaporean households receive $800 in CDC vouchers during 2025, with half specifically allocated for supermarket spending. The immediate impact was visible: supermarket sales jumped 9.2% year-over-year in July-August 2025, dramatically outpacing the 1.7% growth seen in the first half of 2025.

Sheng Siong implemented a differentiated CDC voucher strategy that showcases management’s tactical acumen. While competitors required minimum spends of $60 to qualify for promotions, Sheng Siong lowered its threshold to $30, making it more accessible for budget-conscious shoppers using government vouchers. This pricing discipline extends to their core business model—positioning as the value-for-money option while maintaining healthy margins through operational efficiency.

The timing couldn’t be better for Sheng Siong’s expansion phase. With new stores opening throughout 2025 and government vouchers driving increased supermarket spending, the company benefits from both organic growth and market expansion.

Market Share Opportunity: DFI’s Strategic Retreat Creates Opening

The most significant structural change in Singapore’s supermarket landscape comes from DFI Retail Group’s decision to exit traditional grocery retail. Malaysian conglomerate Macrovalue acquired 48 Cold Storage and 41 Giant stores for $125 million, signaling DFI’s strategic pivot toward higher-margin Guardian and 7-Eleven operations.

This retreat creates immediate market share opportunities for remaining players. Maybank analyst Hussaini Saifee specifically highlighted this in his buy rating, noting that DFI’s exit “creates a market share opportunity for Sheng Siong”. The timing is particularly advantageous given that Giant has been shrinking—eleven outlets closed in 2024 alone—while DFI’s food segment only became profitable in 2024 after years of losses.

Sheng Siong’s competitive positioning becomes more attractive when you examine the market structure. Singapore’s top three supermarket operators now consist of NTUC FairPrice (370+ outlets), Sheng Siong (expanding rapidly), and the newly-acquired Cold Storage/Giant network under Malaysian ownership. With DFI focused elsewhere and new foreign ownership potentially disrupting Cold Storage’s premium positioning, Sheng Siong occupies an increasingly valuable middle ground.

Financial Performance: Margin Expansion Through Operational Excellence

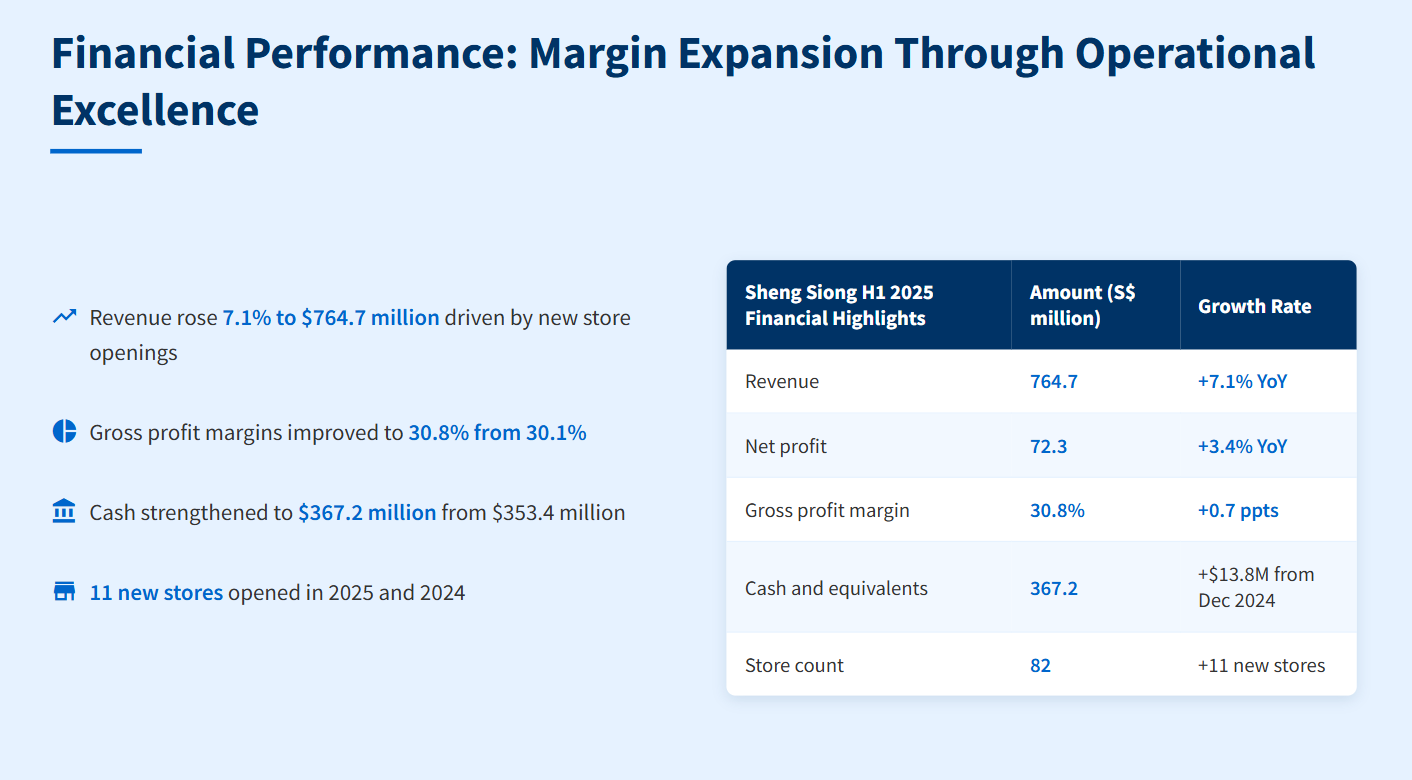

Sheng Siong’s first half 2025 results show the company is successfully turning growth into profitability. The numbers speak for themselves:

Revenue: Rose 7.1% to $764.7 million, driven by the network expansion of eleven new stores.

Gross Profit Margin: Improved to 30.8% (up from 30.1% a year ago). This is a crucial metric, reflecting a better sales mix and successful cost mitigation.

Strong Balance Sheet: Cash and cash equivalents strengthened to $367.2 million, providing a solid “war chest” for continued expansion.

Now, you might see that operating expenses (OpEx) rose 12.2%—faster than revenue. Don’t be alarmed. This is the “cost of growth” in action. This increase is primarily due to new store openings (which have upfront costs before they mature) and variable bonuses paid out for better performance.

What’s impressive is that the company still expanded its gross margins despite these growth investments. This points to strong operational excellence. Sheng Siong is leveraging its increasing scale for better procurement efficiencies, all while its fresh produce focus continues to differentiate it from online-only platforms.

Expansion Pipeline: HDB Tenders and Strategic Site Selection

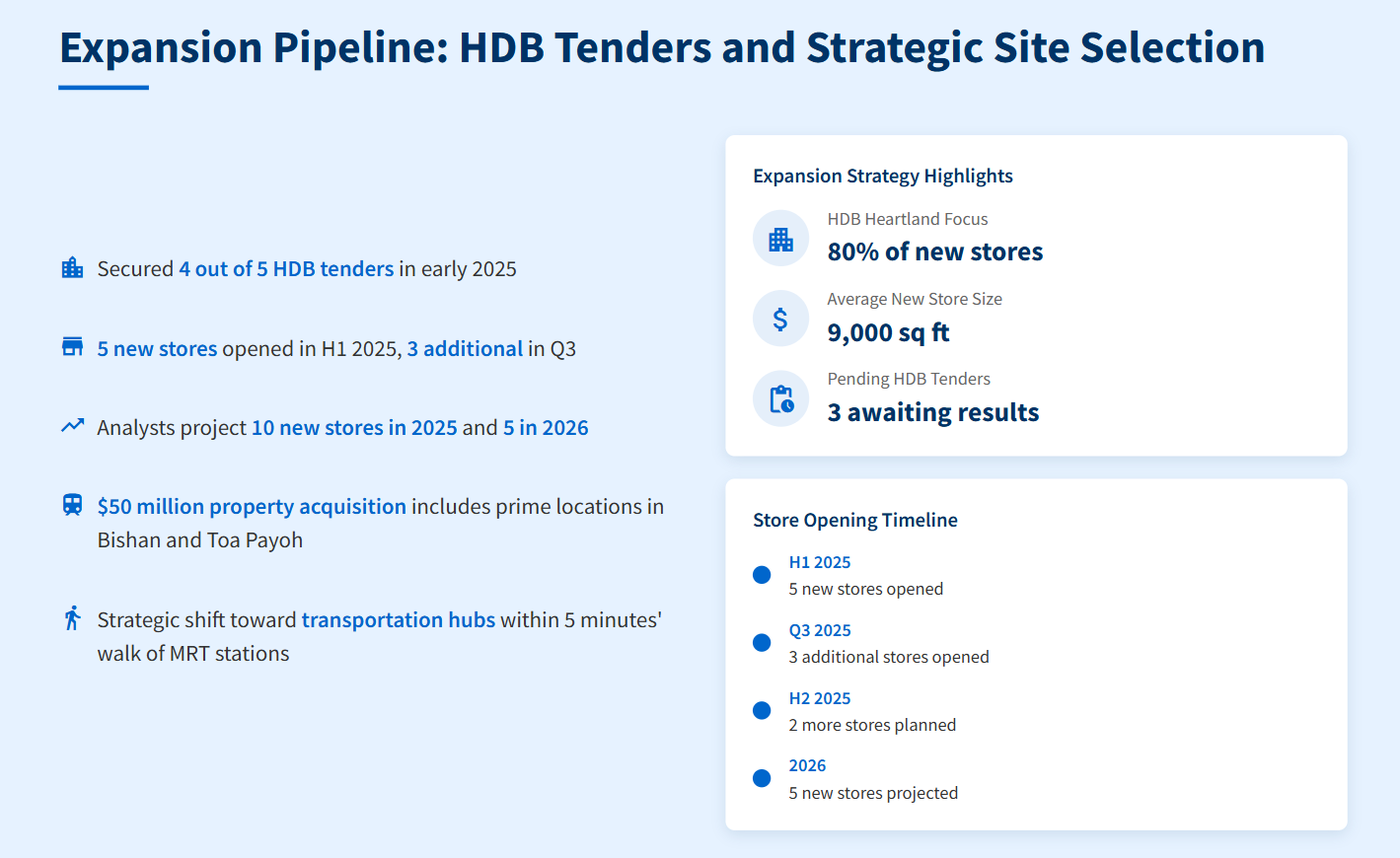

Sheng Siong’s growth strategy focuses on securing prime HDB heartland locations where its value proposition resonates strongest. The company secured four out of five HDB tenders it bid for in early 2025, demonstrating both management’s site selection expertise and the government’s confidence in their operations.

The expansion pipeline looks robust: five new stores opened in the first half of 2025, with three additional stores opening in the third quarter. Management revealed that three HDB tenders await results, with plans to bid for additional sites throughout 2025. Analysts project ten new store openings in 2025 and five in 2026, supporting Maybank’s revenue growth forecasts.

Strategic positioning extends beyond HDB sites. Sheng Siong’s $50 million property acquisition included prime locations in Bishan and Toa Payoh, both within five minutes’ walk of MRT stations. This signals a strategic shift from purely heartland positioning toward transportation hubs while maintaining the affordable grocery focus that drives customer loyalty.

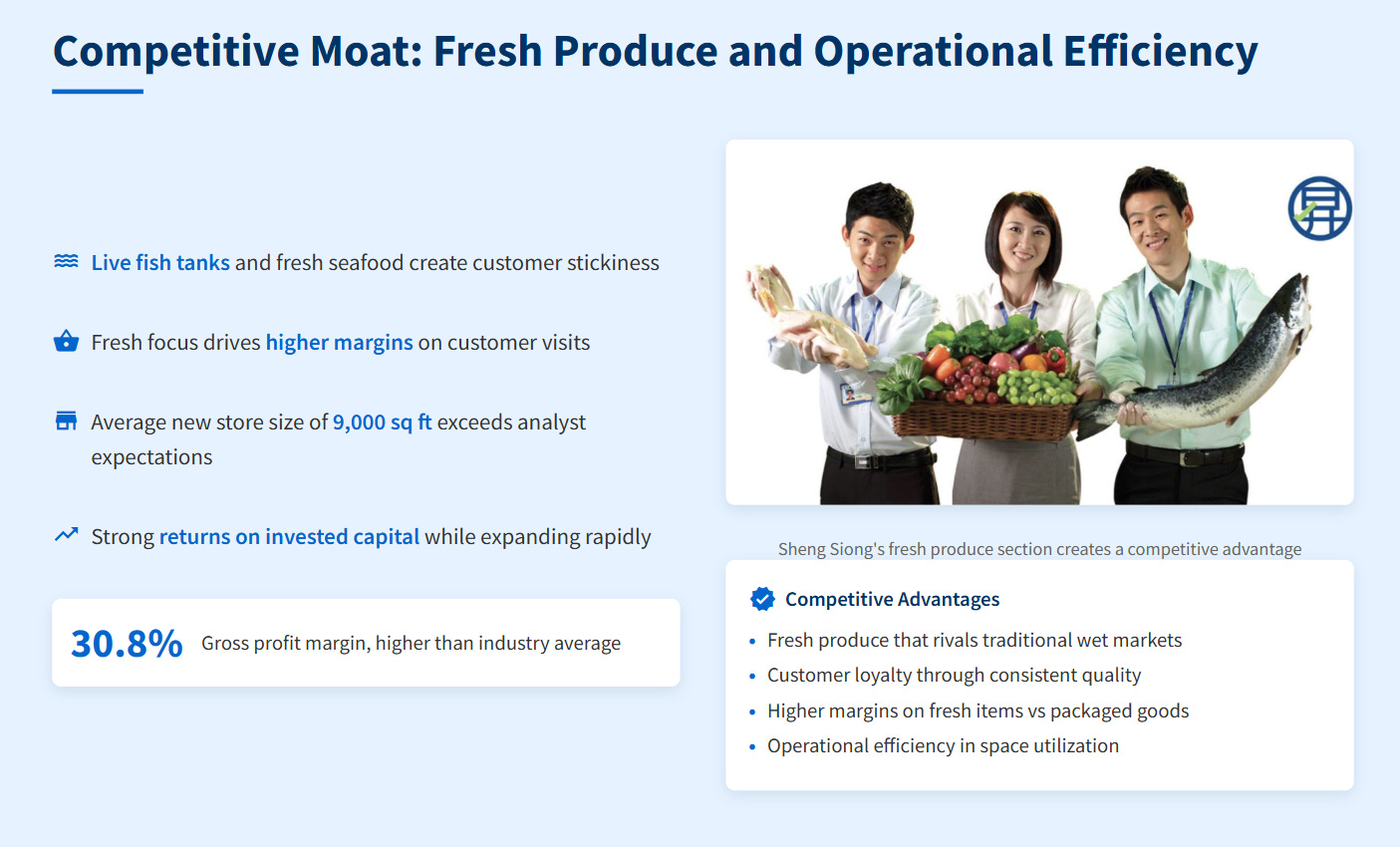

Competitive Moat: Fresh Produce and Operational Efficiency

The most underappreciated aspect of Sheng Siong’s business model is its fresh produce competitive advantage. Walk into any Sheng Siong outlet and you’ll see live fish swimming in tanks, customers queuing for fresh seafood, and produce sections that rival traditional wet markets. This fresh focus creates customer stickiness that online grocery platforms struggle to replicate.

The fresh produce strategy also drives higher margins. While customers initially visit for affordable staples, they often purchase higher-margin fresh items during the same trip. This shopping behavior explains how Sheng Siong maintains industry-leading profitability while competing on price for packaged goods.

Operational efficiency complements the fresh focus. Sheng Siong’s average new store size of 9,000 square feet in the first half 2025 exceeded analyst expectations of 6,000 square feet, indicating improved space utilization and potentially higher revenue per square foot. The company’s ability to generate strong returns on invested capital while expanding rapidly demonstrates management’s execution capabilities.

Iggy’s Take: How Sheng Siong Fits in Your CPF/SRS Portfolio