SGX Fair Value: Why I'm Waiting for $15.33

The stock is trading 8% above fair value. Should dividend investors panic, or is this simply the price you pay for quality?

If you’re new here, welcome—The Investing Iguana just hit 1.3 million reads and 65,000 likes. We’re thrilled to welcome our growing community of over 48 YouTube Premium subscribers and 22 paid Substack members. We recently landed 8th in Tiger Brokers’ 2024 Influential Tigers ranking.

Since October 2025, I’ve produced over 1,200 videos and more than 600,000 watch hours. If you want deeper context and a sharper edge in Singapore’s markets, you’re right where you need to be.

In This Article:

• The Valuation Puzzle: When Growth Hides in Plain Sight

• The Volume Boom: Real or Temporary?

• SGX’s Business Mix: Which Part Is the Real Winner?

• InvestingPro Reality Check

• The Dividend Question: Is the Income Safe?

• The Investor’s Playbook: What Should You Do?

• The Investing Iguana’s Verdict

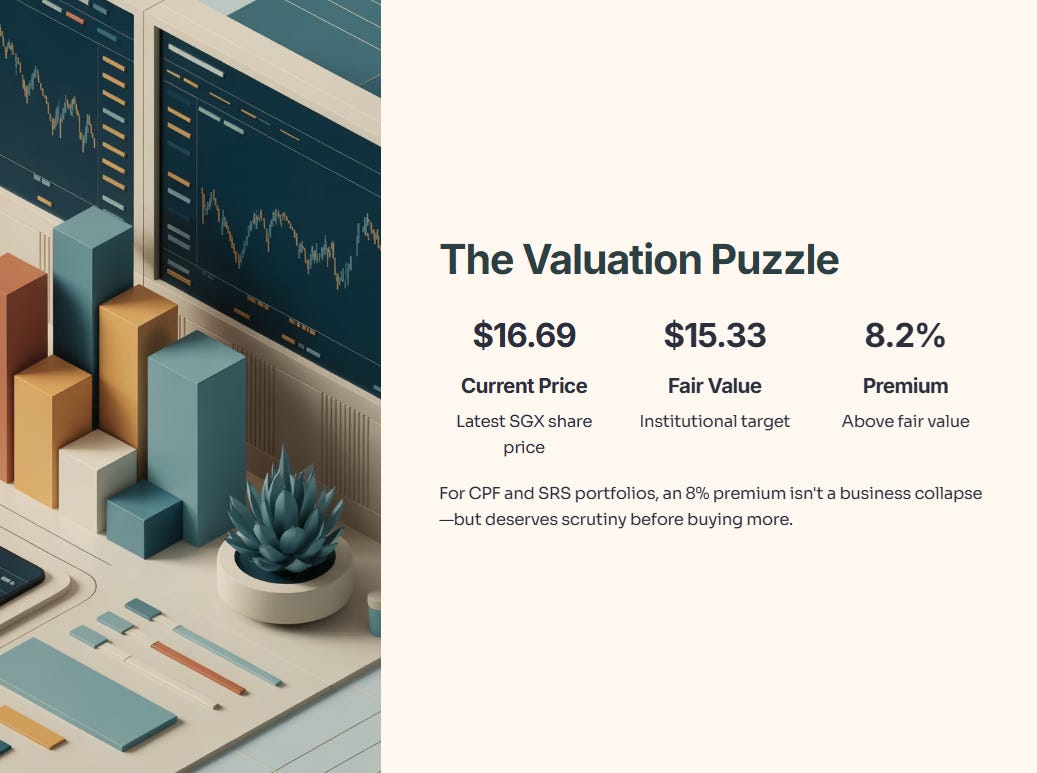

The Valuation Puzzle: When Growth Hides in Plain Sight

Last week, analysts raised questions about SGX’s valuation. The headline sounds alarming: shares currently “screen as overvalued.”

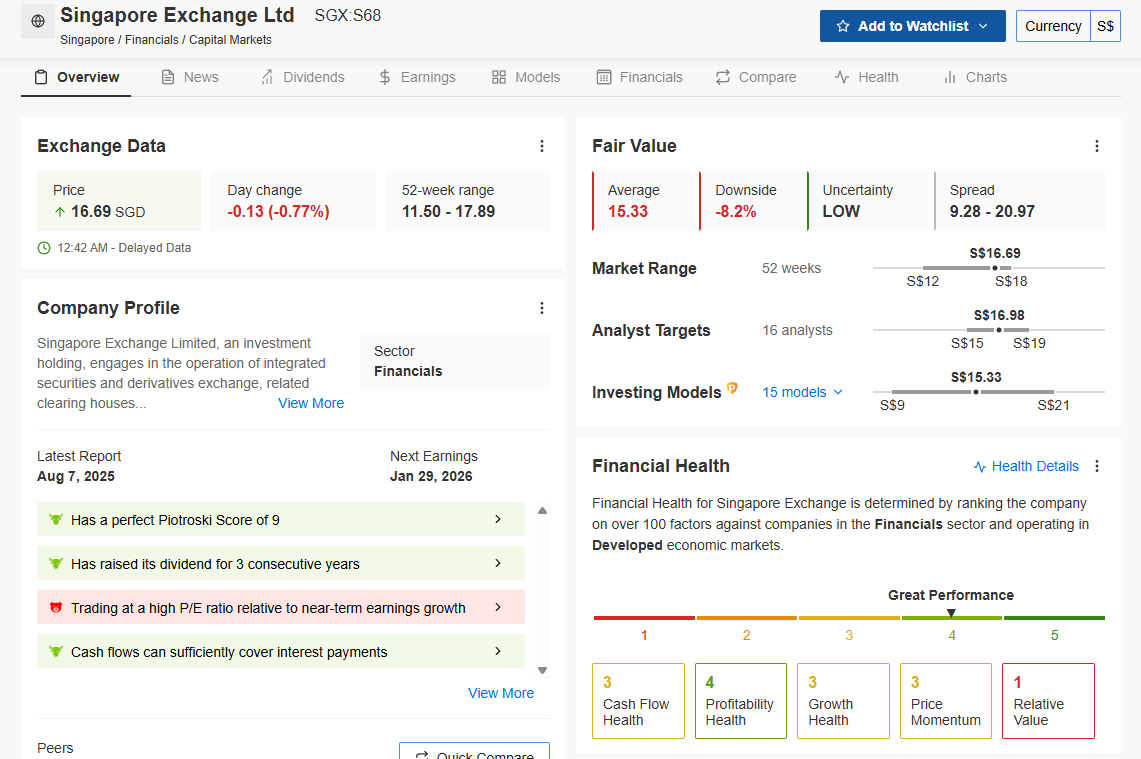

At S$16.69 (as of the latest close), SGX trades approximately 8.2% above the institutional Fair Value target of S$15.33.

For my readers—mostly experienced professionals managing CPF and SRS portfolios—your reaction to this gap matters. If you own SGX strictly for dividends, an 8% premium on valuation is not the same as a red-flag business collapse. However, if you are sitting on cash thinking about buying more, this gap deserves a forensic look.

Iggy’s Insight:

A valuation premium isn’t always a “sell” signal. Often, it’s the “quality tax” the market charges for safety during uncertain times. The question isn’t “Is it expensive?” The question is, “Is the premium justified by the cash flow?”

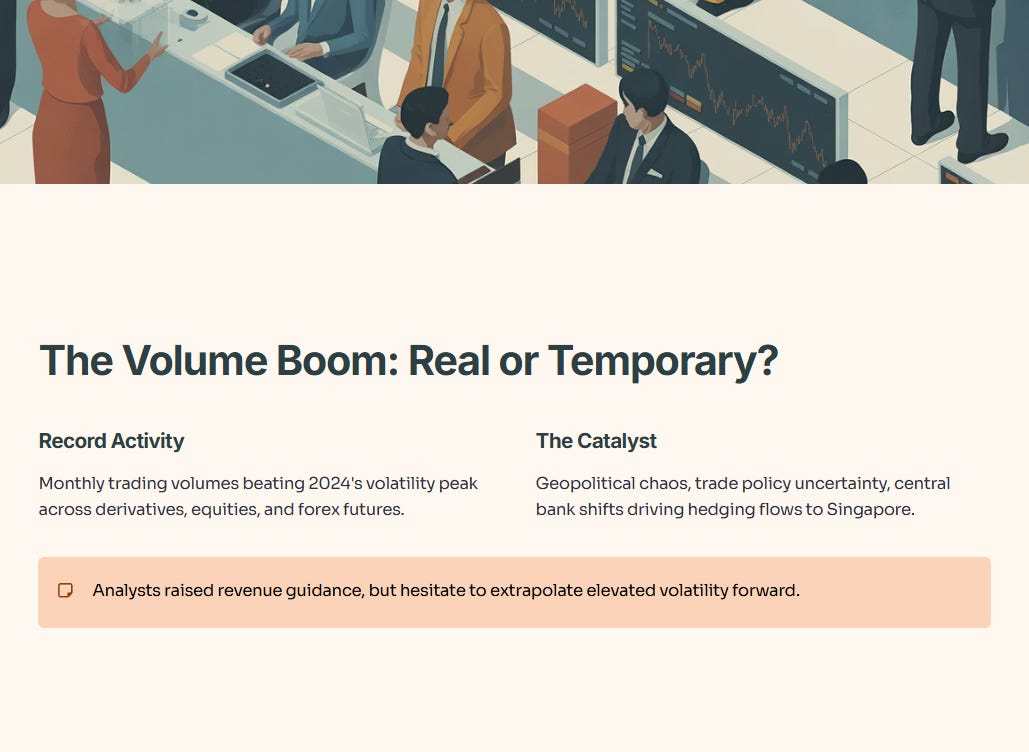

The Volume Boom: Real or Temporary?

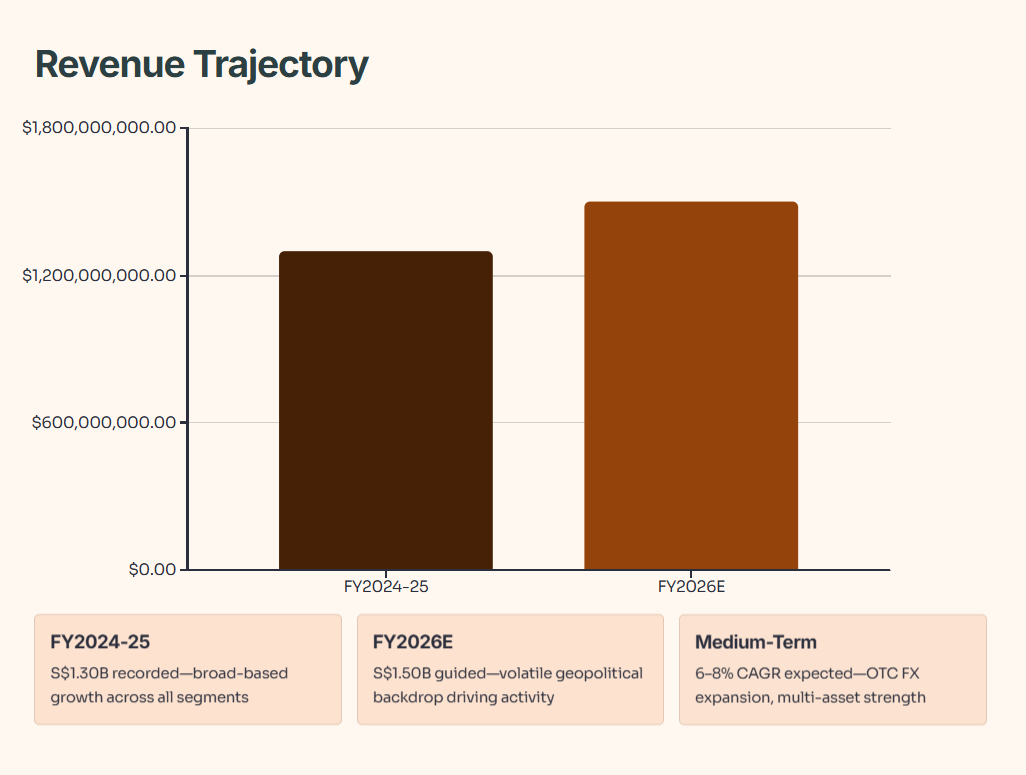

The headline data looks stellar. SGX’s monthly trading volumes in recent weeks have beaten even 2024’s volatility peak. We are seeing record-breaking activity across derivatives, equities, and forex futures.

Why? Geopolitical chaos. Trade policy uncertainty. Central banks shifting their interest rate playbooks. When the world gets nervous, traders hedging their bets flow into Singapore’s exchange.

Analysts have raised revenue guidance because of this activity. But—and here is where the caution creeps in—the market is hesitant to extrapolate this elevated volatility forward.

The reality: SGX’s medium-term growth story (6–8% revenue growth) is solid. But the near-term surge may be masking whether the company can grow sustainably when the global chaos eventually subsides.

SGX’s Business Mix: Which Part Is the Real Winner?

Let’s look under the hood. SGX doesn’t rely on a single revenue stream. That is its actual strength—and why dividend safety matters for your retirement portfolio.

Three of four major segments grew double digits. That’s not a one-hit wonder story. Derivatives, cash equities, and forex are all firing.

Iggy’s Take:

Notice that Derivatives and Forex thrive on volatility and hedging demand. This is SGX’s “antifragile” component. When the Straits Times Index (STI) is boring, SGX makes money from traders betting on other markets.

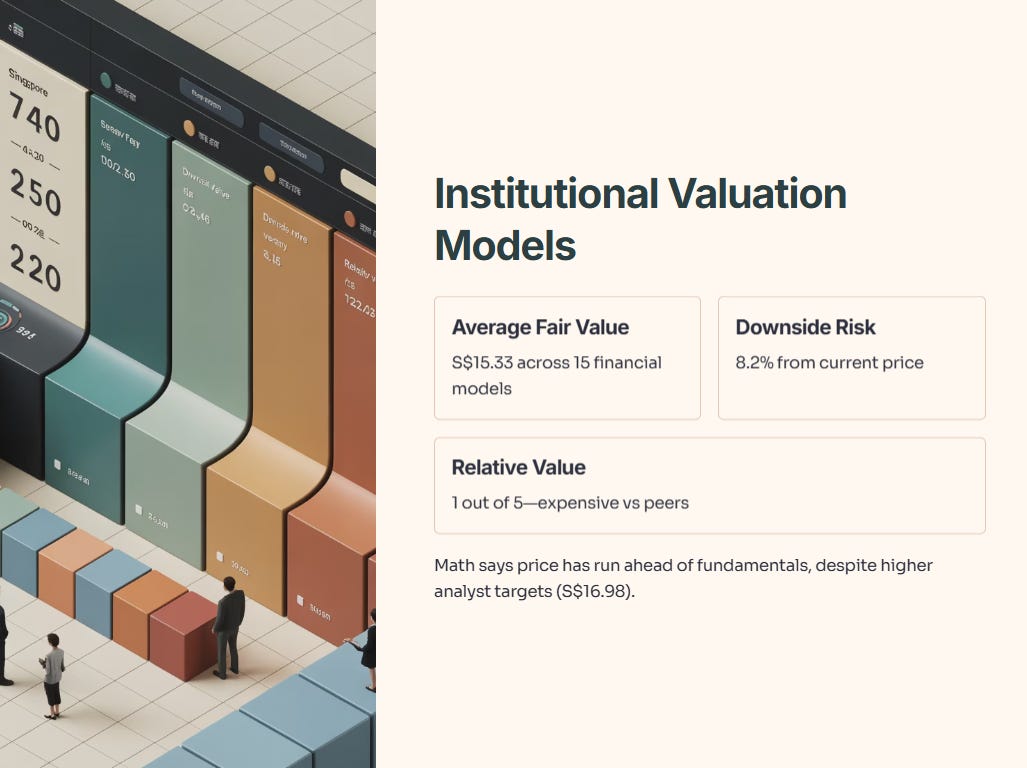

Data Check: Institutional Valuation Models

I don’t just guess at valuations based on feelings. I check the institutional models to see if the math supports the price.

Source: InvestingPro (Data as of December 17, 2025). Premium members can use code INVESTINGIGUANA for up to 50% off.

The Analysis: The models are clear. With an **Average Fair Value of S$15.33**, the stock has an **8.2% downside risk**.

Look specifically at the **Investing Models** breakdown—15 separate financial models are converging on this lower price target. While analyst targets are slightly higher (S$16.98), the math says the price has run ahead of the fundamentals. Note the “Relative Value” score of 1 out of 5 in the health section—this confirms the stock is expensive relative to its peers.

The Dividend Question: Is the Income Safe?

For dividend investors in their 40s and 50s eyeing CPF/SRS allocations, this is the only question that truly matters.

While the market buzzes about valuation, the income story remains rock solid. The company has been consistently raising payouts, and the latest data confirms that this growth is supported by real earnings, not just debt.

Here is the math on safety:

Recent Payout Trend: The dividend has stepped up from S$0.09 quarterly (early 2025) to **S$0.1075** in the most recent declaration.

Yield: Approximately 2.33% (Trailing).

Consistency: A confirmed 3-Year Growth Streak.

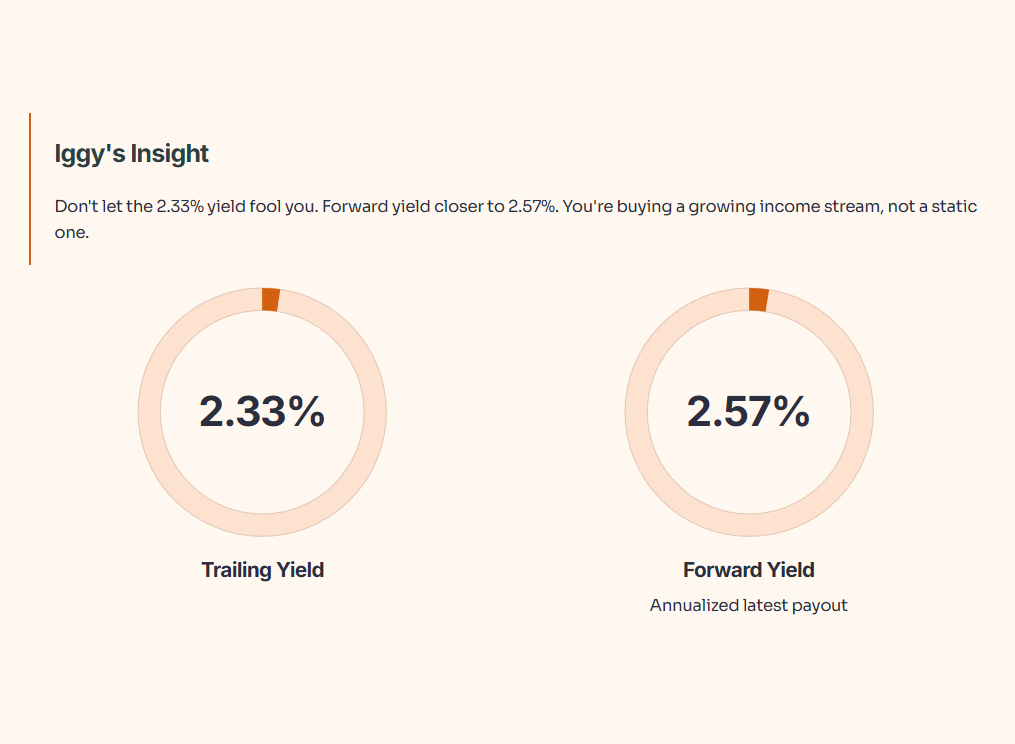

Iggy’s Insight:

Don’t let the 2.33% yield fool you. That is the trailing yield. If you annualize the latest S$0.1075 payout (S$0.1075 x 4), the forward yield is actually closer to 2.57%. You are buying a growing income stream, not a static one.

Data Check: Dividend Safety & Payout Ratio

I don’t just guess at sustainability. I check the payout ratios to ensure the company isn’t bleeding cash to pay you.

Source: InvestingPro (Data as of December 17, 2025). Premium members can use code INVESTINGIGUANA for up to 50% off.

The Analysis: The data is even better than expected.

Payout Ratio: SGX is paying out 59.47% of its earnings. This is arguably safer than the 62% we estimated earlier. It means for every dollar SGX earns, it keeps roughly 40 cents for reinvestment or future buffers.

Growth Streak: The “3 Years” growth streak badge confirms that management is committed to progressive hikes, even during market volatility.

Hard Numbers: The annualized payout sits at S$0.3925, but with the latest quarterly check coming in at S$0.1075, the trajectory is clearly pointing upward.

The P/E Reality: Expensive or Justified?

SGX trades at a P/E ratio of approximately 27–28x.

For context, the Singapore market average P/E is closer to 13–15x. SGX is essentially priced at a 2x premium to the broader market.

Is that justified? Partially.

SGX should trade at a premium because it is a monopoly exchange with a unique competitive moat. But a 2x premium assumes that the volatility we saw in 2024–2025 will last forever.

Iggy’s Take:

If volatility normalizes and trading volumes settle back to pre-2024 levels, earnings growth will slow, and the P/E multiple will compress. That is the specific risk the data is warning about. You are paying a “Growth” price for a “Yield” stock.

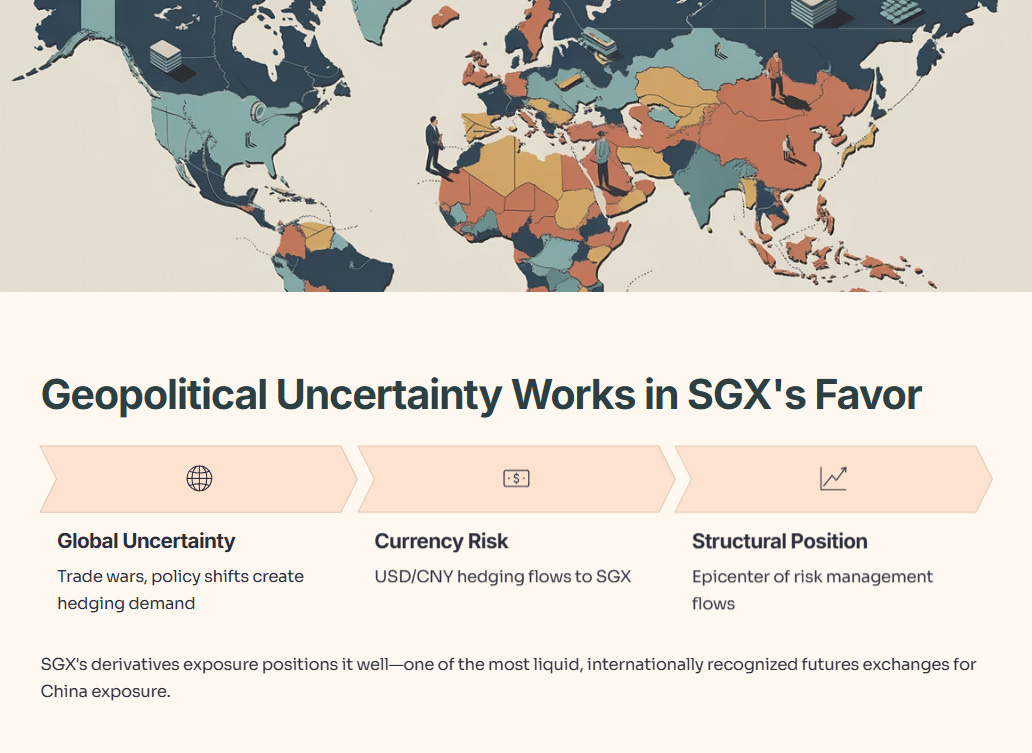

The Bigger Picture: Why Geopolitical Uncertainty Works in SGX’s Favor

Analysts acknowledge that SGX’s outsize exposure to derivatives positions it well even if broader geopolitical stability returns.

Why? Because when institutions and traders worldwide need to hedge currency risk (USD/CNY) or commodity exposure, they come to SGX. It is one of the most liquid, internationally recognized futures exchanges for China exposure.

This is structurally bullish. SGX isn’t just riding a wave; it is positioned at the epicenter of where risk management flows when the world is uncertain.

The Investor’s Playbook: What Should You Do?

We have a stock that is fundamentally strong (Perfect Piotroski Score!) but statistically expensive (8.2% downside risk). Here is how a logical Singaporean investor should play this: