Why PLQ Mall Could Be the Game-Changer Lendlease REIT Needs

Unlock why PLQ Mall could become Lendlease REIT’s real growth engine—discover the strategic move that smart investors won’t want to miss, and how it could reshape your income strategy in Singapore’s m

Most Singapore investors are missing the bigger picture with Lendlease REIT's potential PLQ mall acquisition. While they see another property deal, smart money recognizes this as a strategic portfolio transformation. It could unlock significant value for patient investors willing to look beyond surface-level metrics.

The recent news that Abu Dhabi Investment Authority (ADIA) is reportedly looking to sell its 70% stake in PLQ mall to Lendlease REIT has caught the attention of DBS analysts. They maintain their "buy" rating and 75 cents target price. But the real question every Singaporean investor should ask isn't whether this deal makes sense. It's whether you understand why this acquisition represents a fundamental shift in how Lendlease REIT positions itself in Singapore's evolving retail landscape.

Most retail REIT analysis focuses on immediate yield metrics and occupancy rates. However, the PLQ mall opportunity reveals something far more compelling. It is a chance for Lendlease REIT to build a dominant retail portfolio. This portfolio would combine prime Orchard Road presence with strategic suburban positioning, just as Singapore's retail market enters a new growth phase.

The Strategic Portfolio Transformation

Lendlease REIT currently trades below its book value, suggesting the market hasn't fully recognized the value embedded in its assets. The potential acquisition of PLQ mall's remaining 70% stake would give the REIT full ownership and control of a property valued at over SGD 1 billion. It features 340,000 square feet of retail space in one of Singapore's fastest-developing transport hubs.

Table: Lendlease REIT Key Metrics (September 2025)

This table summarizes Lendlease REIT's key financial indicators as of late September 2025. The most important takeaway is the gap between its current share price and its Price-to-Net Asset Value (P/NAV) ratio, which sits below 1.0x. This suggests the market is valuing the REIT's assets at less than their book value, creating a potential value opportunity for new investors. Combined with a strong forward dividend yield, these metrics point to a potentially undervalued income-producing asset.

This isn't just another property acquisition. It's portfolio optimization at its finest. Currently, Lendlease REIT's Singapore retail exposure centers on 313@Somerset, a prime Orchard Road asset. Adding PLQ mall creates a powerful one-two punch: prime retail in the city center complemented by necessity-driven suburban retail in the growing Paya Lebar district. The timing couldn't be better. Singapore's retail REIT sector is experiencing a renaissance. Occupancy rates are typically north of 96% and rental reversions are turning positive across well-managed portfolios. Suburban malls are leading this recovery, with some even exceeding pre-COVID revenue metrics.

Financial Strength Creates Acquisition Opportunity

What makes this potential acquisition particularly attractive is Lendlease REIT's improved financial position. This follows the successful divestment of its JEM office stake. This strategic move has strengthened the balance sheet dramatically.

Table: Impact of JEM Divestment on Financial Health

This table illustrates the direct impact of the JEM office divestment on Lendlease REIT's balance sheet. The key insight is the sharp drop in aggregate leverage from a high level to a much more comfortable 35%. This deleveraging strengthens the REIT's financial foundation and gives management the flexibility to pursue growth opportunities like the PLQ Mall acquisition without taking on excessive risk.

The numbers tell a compelling story. With an improved interest coverage ratio and lower cost of debt, Lendlease REIT has created the financial flexibility needed for growth. This positions the REIT perfectly to capitalize on acquisition opportunities like PLQ mall without compromising its conservative capital structure. The dividend sustainability question that concerns many investors becomes clearer when viewed through this lens. While the dividend per share has moderated from its 2022 peak, the current forward yield remains attractive. More importantly, the improved balance sheet provides a solid foundation for stable distributions going forward.

PLQ Mall: The Hidden Suburban Retail Gem

PLQ mall represents exactly the type of asset that's driving outperformance in Singapore's retail REIT sector. Located at Paya Lebar Quarter, this isn't just another suburban mall. It's a transport-connected retail destination anchored by over 200 shops offering quality shopping, everyday conveniences, and dining options.

Table: PLQ Mall Asset Profile

This table provides a snapshot of PLQ Mall's strategic importance. Its large retail space and direct connection to the Paya Lebar MRT interchange are its core strengths, ensuring high footfall from both residents and commuters. For Lendlease REIT, acquiring this asset provides crucial diversification away from the tourist-dependent Orchard Road belt, adding a stable, necessity-driven suburban anchor to its portfolio.

The strategic value becomes apparent when you consider the location advantages. PLQ mall benefits from direct connectivity to Paya Lebar MRT interchange, one of Singapore's major transport hubs. This connectivity supports consistent footfall from both local residents and commuters. This creates a stable customer base that's less dependent on discretionary tourism spending. The tenant mix at PLQ mall reflects the resilience that's driving suburban retail success across Singapore. With a curated mix of retail, food & beverage, and lifestyle tenants, the mall captures both necessity-driven spending and experiential retail trends that keep physical retail relevant in an e-commerce world.

Market Context: Why Retail REITs Are Winning Again

Understanding the broader Singapore retail REIT landscape is crucial for evaluating this acquisition. The sector has transitioned from post-pandemic recovery to modest growth. This is underpinned by resilient consumption patterns and limited new mall supply. Key performance indicators across the sector paint an encouraging picture. Retail rental reversions have turned positive across well-managed portfolios. Some REITs are achieving mid to high-single-digit rent uplifts on lease renewals, clear signs of restored landlord pricing power.

The tourism recovery adds another layer of support. It particularly benefits prime locations like 313@Somerset. Meanwhile, transport-connected suburban assets like PLQ mall benefit from steady local demand. This dual-pronged approach insulates Lendlease REIT from over-dependence on any single demand driver. Interest rate trends provide additional tailwinds. With interest rates expected to moderate, financing costs for quality REITs should continue improving. This environment supports both property valuations and distribution sustainability.

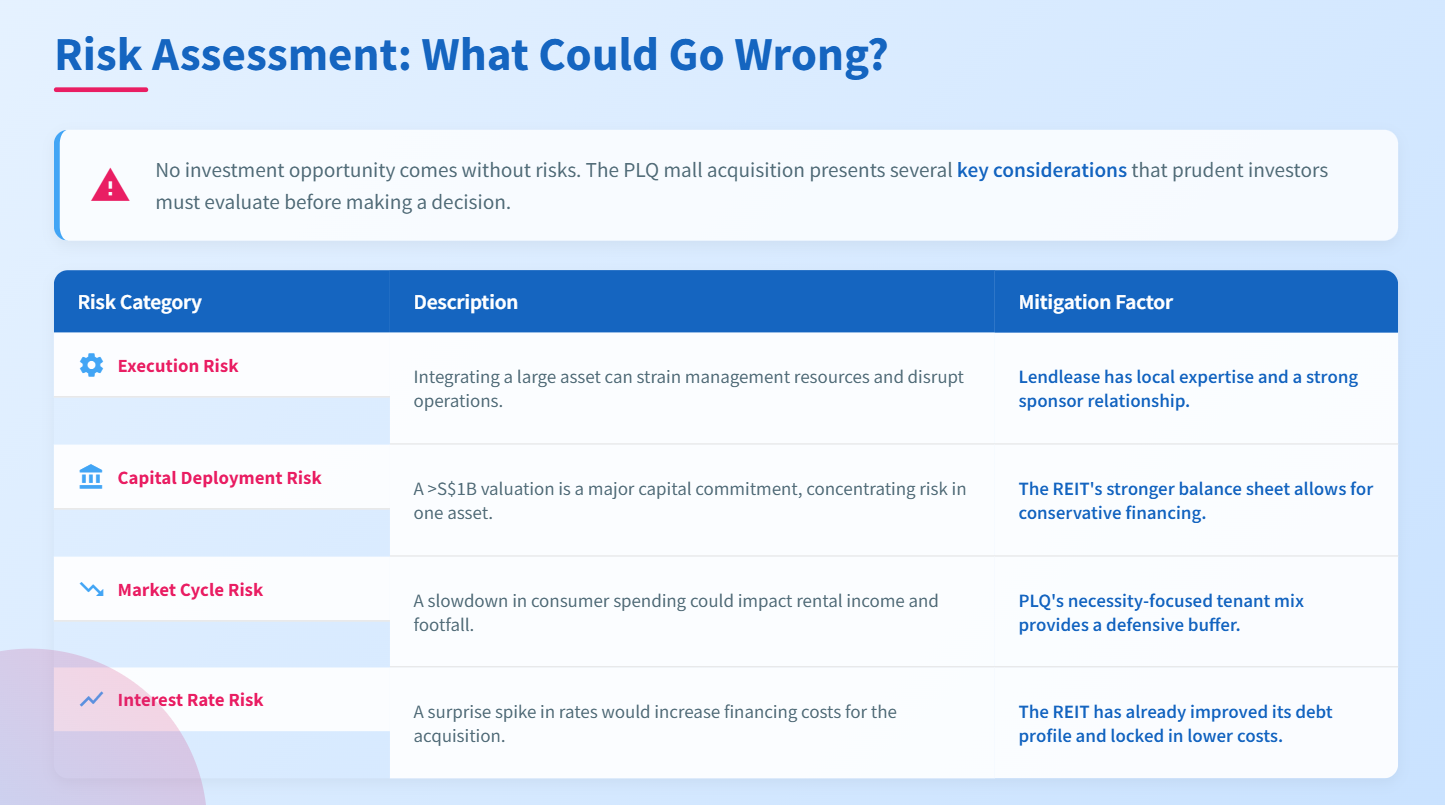

Risk Assessment: What Could Go Wrong?

No investment opportunity comes without risks. The PLQ mall acquisition presents several considerations that prudent investors must evaluate.

Table: Key Risks in PLQ Mall Acquisition

This table breaks down the primary risks associated with the PLQ mall deal. While any large acquisition has execution and financing risks, the key takeaway is that Lendlease REIT has already taken steps to mitigate them. The recent deleveraging and the defensive nature of a suburban mall help cushion the REIT against market or interest rate shocks, making the risk-reward profile more attractive.

Investment Recommendation: Strategic Buy for Patient Capital

Should investors consider Lendlease REIT as a buy, hold, or sell? The answer depends on your investment horizon and risk tolerance. But the fundamental case points toward a strategic buy for patient investors. The combination of attractive valuation, improved balance sheet strength, strategic portfolio positioning, and supportive market conditions creates a compelling risk-adjusted opportunity. The upside to DBS's target price provides a margin of safety while the forward yield offers attractive income.

This is a 3-5 year strategic holding rather than a short-term trade. The benefits of portfolio diversification and rental growth will compound over time. This requires patience as integration occurs and market conditions evolve. Given the concentration risk of a single REIT position, consider this as a 3-5% allocation within a broader Singapore REIT portfolio. The improved financial metrics support this weighting for income-focused investors.

Critical Considerations for Singapore Investors

Several factors demand particular attention from Singapore-based investors evaluating this opportunity. Lendlease REIT's improved balance sheet metrics and attractive dividend yield make it suitable for CPF Investment Scheme and SRS portfolios focused on income generation. The strengthened capital structure reduces risk while maintaining income. As with most Singapore REITs, distributions are generally tax-exempt for individual investors, making the forward yield particularly attractive on an after-tax basis. With Singapore assets representing the core portfolio, currency risk is minimal for SGD-based investors.

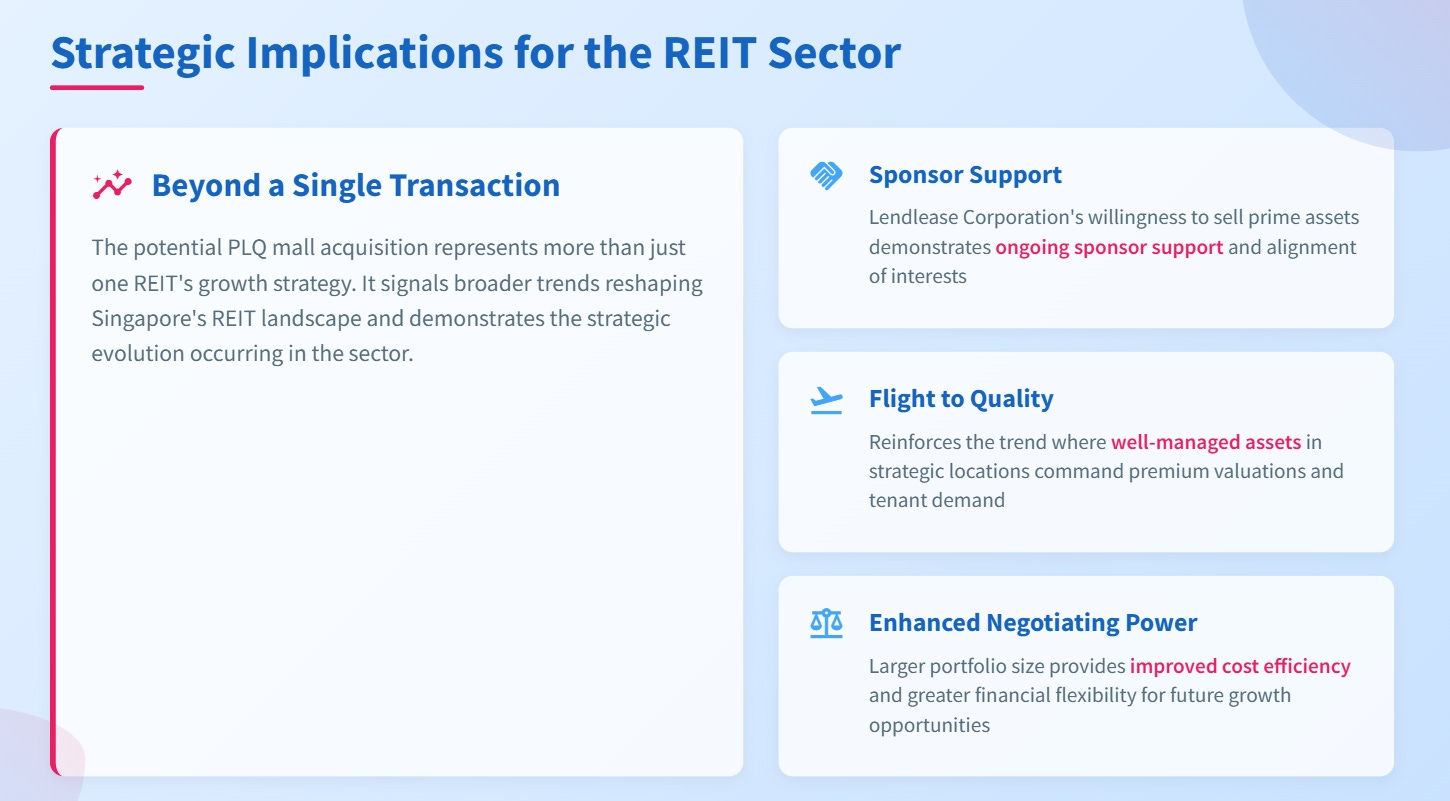

Strategic Implications for the REIT Sector

The potential PLQ mall acquisition represents more than just one REIT's growth strategy. It signals broader trends reshaping Singapore's REIT landscape. Lendlease Corporation's willingness to sell prime assets to the REIT demonstrates ongoing sponsor support and alignment of interests. The transaction reinforces the "flight to quality" occurring across Singapore REITs, where well-managed assets in strategic locations command premium valuations and tenant demand. Finally, a larger portfolio size provides enhanced negotiating power with tenants, improved cost efficiency, and greater financial flexibility for future growth.

Final Recommendation: Lendlease REIT – A Strategic Buy for Patient, Income-Focused Investors