Why Singapore’s Multi-Billion Dollar Energy Bet Could Reshape Your Portfolio—But Only If You’re Patient Enough

Singapore’s Big Bet: Decoding the Clean Energy Import Surge and How Investors Can Play the Multi-Billion Dollar Transition

You’ve probably heard about Singapore’s push for clean energy, but here’s the confusion: Should you jump into energy stocks now, or is this just another government talking point that won’t move the needle for years? The truth is far more nuanced than most investors realize—and getting the timing right could mean the difference between solid long-term gains and dead money sitting in your account for a decade.

Singapore just granted conditional approval for a massive 1 gigawatt hydropower import from Malaysia’s Sarawak state. This isn’t just another press release. It’s the opening act of a fundamental restructuring of how Singapore powers itself—and how certain companies will profit from that transition. But here’s what the headlines won’t tell you: the revenue won’t start flowing until 2035, the execution risks are substantial, and the stock everyone’s talking about has already dropped 22 percent from its recent peak.

Let me break down exactly what’s happening, which companies stand to benefit, and whether this is a buy-now opportunity or a watch-and-wait situation for Singapore investors.

In This Article:

• Singapore’s Energy Reality Check

• The Bigger Picture: The 6 GW Target

• The Sarawak Hydropower Deal

• Sembcorp Industries: The Stock to Watch

• Is Sembcorp A Buy Right Now?

• Investment Recommendation

• Beyond Sembcorp: Other Ways To Play

• Major Risks That Could Derail The Plan

• Final TakeawaysSingapore’s Energy Reality Check: Why We Can’t Generate Our Own Power

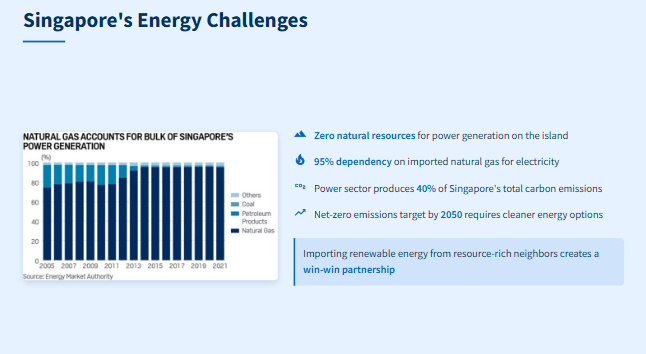

Singapore faces a brutal constraint that shapes every energy decision we make. We’re a tiny island with zero natural resources for power generation. We can’t build massive hydroelectric dams like Malaysia. We don’t have vast deserts for sprawling solar farms. Right now, Singapore relies almost entirely on natural gas—which we import—for about 95 percent of our electricity generation.

Here’s the problem that should concern every investor and citizen: Singapore’s power sector produces roughly 40 percent of our total carbon emissions. That’s a massive chunk. As the nation pushes toward net-zero emissions by 2050, we desperately need cleaner options. Importing renewable energy from neighbors with abundant natural resources becomes the only viable path forward. Malaysia has rivers and land for hydropower. We have the financial capability and demand. It’s a classic win-win partnership driven by geographic necessity.

The current energy landscape tells a stark story. With only 734 square kilometers of total land area, Singapore generates just 5 percent of its electricity from renewables. The government has set a target to import 6 gigawatts of clean power by 2035—which would represent about one-third of our expected energy demand at that time. This isn’t an incremental adjustment. It’s a wholesale restructuring of our energy infrastructure.

Table: Singapore’s Energy Landscape - Current vs. Future

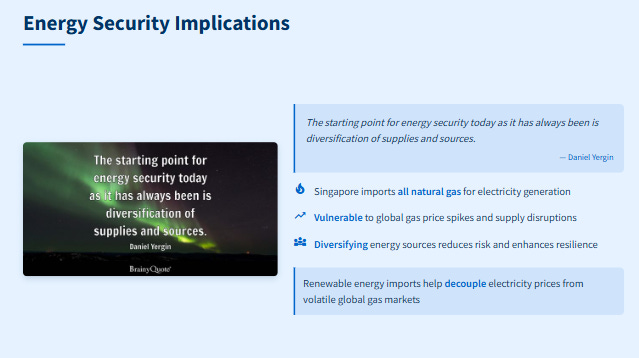

This table reveals the magnitude of Singapore’s challenge. Moving from 5 percent renewable generation to having imports supply 33 percent of total demand requires massive infrastructure investment, complex cross-border agreements, and flawless execution over the next decade. Energy security isn’t just an environmental buzzword—it’s about having reliable access to power at affordable prices. When global gas prices spiked in 2021, Singapore’s wholesale electricity prices jumped more than fourfold by 2022. By diversifying energy sources through regional imports, we reduce exposure to that kind of price volatility.

The Bigger Picture: Singapore’s Expanded 6 GW Target

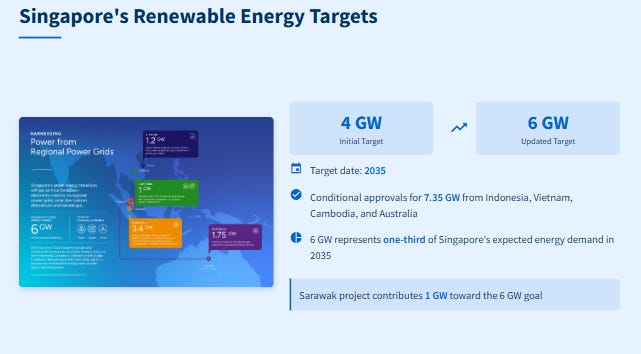

Singapore initially targeted importing 4 gigawatts of clean power by 2035. Due to strong interest from credible parties, the government raised that target to 6 gigawatts in September 2024. The Sarawak project contributes 1 gigawatt toward that 6 gigawatt goal. Singapore has already granted conditional approvals and licenses for 7.35 gigawatts from various sources including Indonesia, Vietnam, Cambodia, and Australia. If all these projects succeed, Singapore could actually exceed its stated 6 gigawatt target.

Here’s what 6 gigawatts means in practical terms: it represents about one-third of Singapore’s expected energy demand in 2035. That’s a significant portion of our power grid coming from clean sources instead of gas. The diversification spans multiple countries and energy types, which provides both opportunities and risk management benefits.

Table: Singapore’s Regional Clean Energy Import Pipeline

On the same day as the Sarawak announcement, three companies—Singapore Energy Interconnections, SP Group, and Tenaga Nasional—signed an agreement to study a new 2 gigawatt electricity interconnection between Singapore and Peninsular Malaysia. This would be the second power link between Singapore and Malaysia. The existing one allows up to 1 gigawatt of bi-directional electricity flows.

Think of interconnections as highways for electricity. They allow power to flow both ways depending on who needs it. During periods when Malaysia has excess renewable energy, they export to Singapore. During times when Singapore has surplus capacity, we could potentially export back. This flexibility strengthens energy security for both nations and creates arbitrage opportunities for power traders.

Table: Singapore’s Clean Energy Import Target Overview

The progression from 4 GW to 6 GW, and now conditional approvals totaling 7.35 GW, shows strong momentum behind Singapore’s regional grid strategy. However, conditional approval is just the first step. Each project must still secure all regulatory approvals from every country the transmission cables pass through. They need to finalize financing structures and complete construction without major delays. Between initial approval and commercial operations lies a gauntlet of technical, commercial, and geopolitical challenges.

What Singapore Just Approved: The Sarawak Hydropower Deal Explained

On October 17, 2025, Singapore’s Energy Market Authority granted conditional approval to Sembcorp Utilities to import 1 gigawatt of hydropower from Sarawak, Malaysia. Think of one gigawatt as enough continuous power to run approximately 250,000 households. This isn’t just any power deal. It’s clean hydropower that will flow through undersea cables stretching over 700 kilometers from Sarawak to Singapore.

The project targets commercial operations around 2035. What makes this deal special is that it represents Singapore’s first large-scale 24/7 power import initiative. Unlike solar power that only works during the day, hydropower provides constant, reliable baseload energy. The electricity will be certified under the Hydropower Sustainability Standard—an international benchmark with specific performance requirements for hydropower infrastructure.

Sembcorp has already signed a preferred supplier agreement with Prysmian, a global leader in high-voltage submarine and underground cable systems. Prysmian will handle the design, installation methodology, and protection requirements for the massive subsea interconnector cable. The technical complexity here cannot be overstated. Building 700-kilometer undersea cables requires enormous engineering expertise, and these cables must survive harsh ocean conditions for decades without failure.

Table: Sarawak Hydropower Project Technical Specifications

This project sits within a much larger regional infrastructure build-out. Research from Rystad Energy suggests that if all proposed interconnections to Singapore materialize, they could unlock up to 25 gigawatts of renewable and energy storage projects worth more than 40 billion dollars across Southeast Asia. We’re talking about hydropower, solar, and offshore wind projects spanning multiple countries. Companies involved in construction, subsea cables, engineering services, and power generation stand to benefit enormously over the next decade.

Sembcorp Industries: The Stock Everyone’s Watching

Sembcorp Industries, through its subsidiary Sembcorp Utilities, is the key player in the Sarawak hydropower deal. The Energy Market Authority granted them conditional approval after assessing that the project is technically and commercially viable. For investors, this announcement matters because Sembcorp is transitioning heavily into renewables. Over 60 percent of their current capacity is already renewable energy.

This Sarawak project adds another major revenue stream starting in 2035. Sembcorp operates across multiple Asian markets with strong operating cash flow of 1.1 billion dollars in the first half of 2025 alone. That cash generation capability is crucial for funding large infrastructure projects. However, the stock has faced headwinds recently. Sembcorp’s share price dropped 22 percent from its July 2025 peak of SGD 7.85 to around SGD 6.37 as of October 21, 2025. The decline stems from currency headwinds affecting its regional operations and weaker-than-expected earnings.

Analysts project earnings growth of approximately 5.6 percent annually over the next three years. That’s decent growth, but it’s notably slower than the Singapore market average of 9.4 percent. The stock trades at a price-to-earnings ratio of 10.9 times, which is relatively cheap compared to most Singapore companies. But there’s always a reason for valuation discounts. The market expects Sembcorp’s growth to lag behind the broader market, and the conditional approval—while positive—doesn’t change the near-term earnings picture.

Table: Sembcorp Industries Financial Snapshot

Sembcorp’s market capitalization of SGD 11.06 billion makes it a substantial player in Singapore’s energy sector. The combination of strong cash flow, renewable energy focus, and below-average valuation creates an interesting setup for long-term investors. However, the gap between conditional approval today and revenue generation in 2035 creates a massive time lag that many investors overlook.

Is Sembcorp A Buy Right Now? The Brutal Truth

Not so fast. The conditional approval is undoubtedly positive for Sembcorp’s long-term prospects, but remember—this project won’t generate a single dollar of revenue until 2035. That’s ten years away. Between now and then, Sembcorp must secure all regulatory approvals from every jurisdiction the cables pass through. The cables cross international waters and potentially territorial waters of other nations. Each approval adds risk and potential delays.

Sembcorp must also finalize the financing structure for what will be a multi-billion dollar infrastructure project. Then comes construction execution. Laying 700 kilometers of subsea high-voltage cables in tropical waters is not a simple engineering task. Weather delays, technical challenges, cost overruns, and unforeseen complications can derail timelines and budgets. For investors buying Sembcorp stock today, you’re betting on management’s ability to deliver this project while simultaneously navigating current challenges like foreign exchange volatility, debt management, and operational performance across their existing asset base.

The company’s relatively cheap valuation—a P/E ratio of 10.9 times—exists for valid reasons. The market is pricing in slower growth, execution risk on major projects, and currency headwinds from regional operations. Consensus analyst price targets around SGD 7.44 suggest roughly 19 percent upside from current levels. That’s reasonable but not spectacular, especially when you consider the multi-year holding period required to see the Sarawak project contribute meaningfully to earnings.

Table: Sembcorp Investment Risk-Reward Matrix

If you’re a long-term investor who believes in Singapore’s energy transition story, Sembcorp offers direct exposure to that structural theme at a reasonable valuation. The company is well-positioned with conditional approvals for 2.2 GW of imports when combining the Sarawak project with their earlier Vietnam approval. That’s a significant chunk of Singapore’s 6 GW target.

But if you need returns in the next year or two, this is probably not your best bet. The stock is unlikely to see major re-rating until concrete progress milestones emerge—final regulatory approvals, construction commencement, successful cable deployment tests. Those catalysts are years away. For income investors, Sembcorp offers a dividend yield around 2.83 percent, which provides some return while you wait, but it’s not compelling enough to overcome the opportunity cost of capital sitting in a slow-growth stock.

Investment Recommendation: Strategic Hold for Patient Capital