The Real Winner of the $53B "Mirage" (5.5% Yield)

The $53 billion construction boom sounds like a goldmine. But for investors chasing main contractors, it's a trap disguised as opportunity.

The headline is intoxicating: “$53 billion construction boom in 2026.” Your retail instinct screams “Buy the builders!” You envision cranes over the skyline and dividends flooding your bank account. You see the names—the survivors of the 2022-2023 delisting wave—and you think you’ve found a generational play.

You are wrong. In fact, you are walking straight into a “Revenue Trap.” In the Singapore construction sector, revenue is a vanity metric; profit is sanity, but cash flow is reality. If you buy the main contractors, you aren’t buying growth; you’re buying a 3% margin business with 100% of the execution risk. Let’s look at why the smart money is buying the shovels, not the diggers.

In This Article:

The Masterclass: The Structural Rot of Fixed-Price Tendering

The Iggy Audit: Dissecting the Survivors

The Data Fortress: Is the Dividend a Mirage?

The Scenario Matrix: 2026 Forecast

InvestingPro Reality Check

The Verdict: The Iggy Action Plan🦎 About Iggy the Investing Iguana

Welcome to the Iguana Pit! If you’re new here, I’m Iggy: your guide through the dense jungle of the Singapore markets. My mission is simple: to spot the predators before they spot your portfolio.

We are now 5,800+ subscribers strong across YouTube and Substack, focusing purely on the data-driven alpha that mainstream media misses.

🚀 Join the “Elite 150” Inner Circle

Real alpha is found behind the velvet rope. Stop following the herd and start following the data with our 150+ paid members.

📺 The YouTube Edge (S$3/mo): Beat the Delay.

Instant Access: Watch new videos the moment they drop.

The Free Tier Trap: Free subscribers wait up to 14 days to see the same video. (By then, the news is old and the trade is gone).

📝 The Substack Deep-Dive (US$6/mo): Unlock the Vault.

Zero Paywalls: Read the full “Deep Dive” articles and “Substack Exclusive” articles found only on Substack.

Visual Alpha: Download exclusive Infographic Cheatsheets not available to free readers.

💎 The Ultimate Value Pass (S$9/mo): (BEST VALUE)

Get It All: Paid via YouTube, this bundle grants you Instant Video Access AND Full Substack Access.

The Math: You save ~30% compared to buying them separately. It’s the “Smart Money” move.

Why wait 2 weeks for old news? Get the data while it’s fresh. 👉 Join Here: https://www.youtube.com/@InvestingIguana/membership

The Masterclass: The Structural Rot of Fixed-Price Tendering

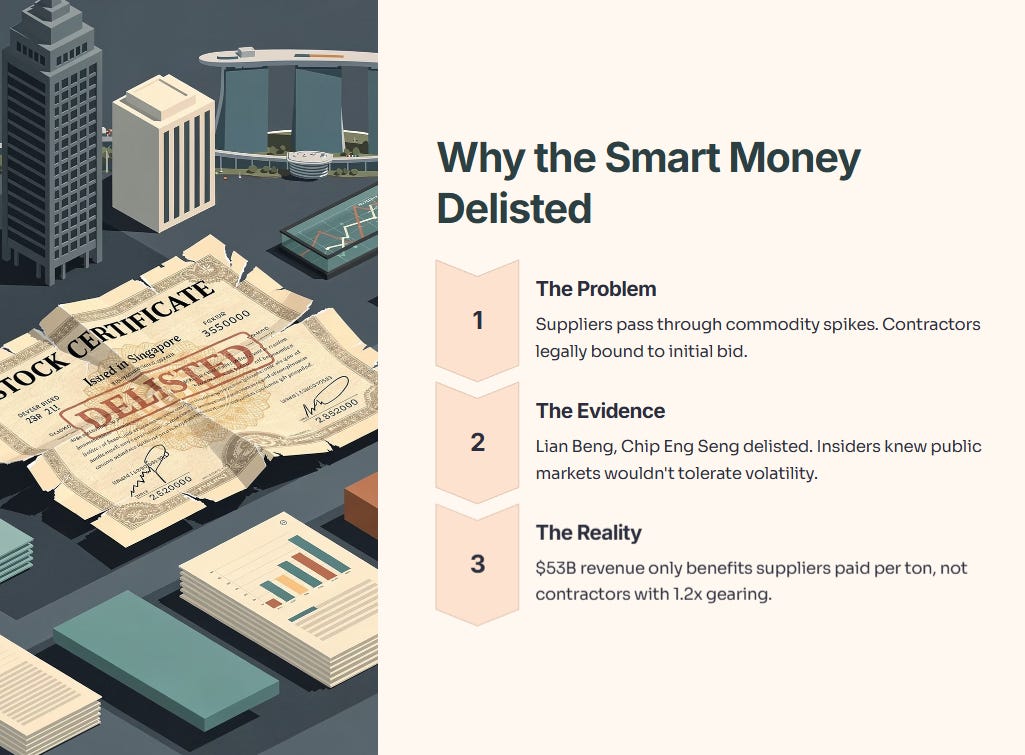

To understand why contractors like the now-privatized Lian Beng or Chip Eng Seng fled the public markets, you must understand the Fixed-Price Tender mechanism. When a contractor bids for a $500 million HDB or T5 project, they lock in a price today for work that will be completed 3–5 years from now.

This creates a massive asymmetric risk profile. The contractor has a “ceiling” on revenue but no “floor” on costs. If the price of reinforced steel surges, if labor costs spike due to policy shifts, or if a global supply chain hiccup delays a shipment of granite, the contractor eats every cent of that variance. We call this the “Negative Convexity” of construction. Your upside is capped at a razor-thin 3-5% net margin, while your downside is literally bankruptcy.

Conversely, Material Suppliers (the “Shovels”) operate on a volume-based, pass-through model. While they may suffer from weak gross profit margins—as seen in BRC Asia’s recent data—they compensate with massive throughput. They don’t bid on a 5-year fixed price; they fulfill purchase orders. If volume spikes ($53B), their high Operating Leverage ensures that net profit grows even if gross margins remain thin. They capture the boom’s volume without the contractor’s long-term liability.

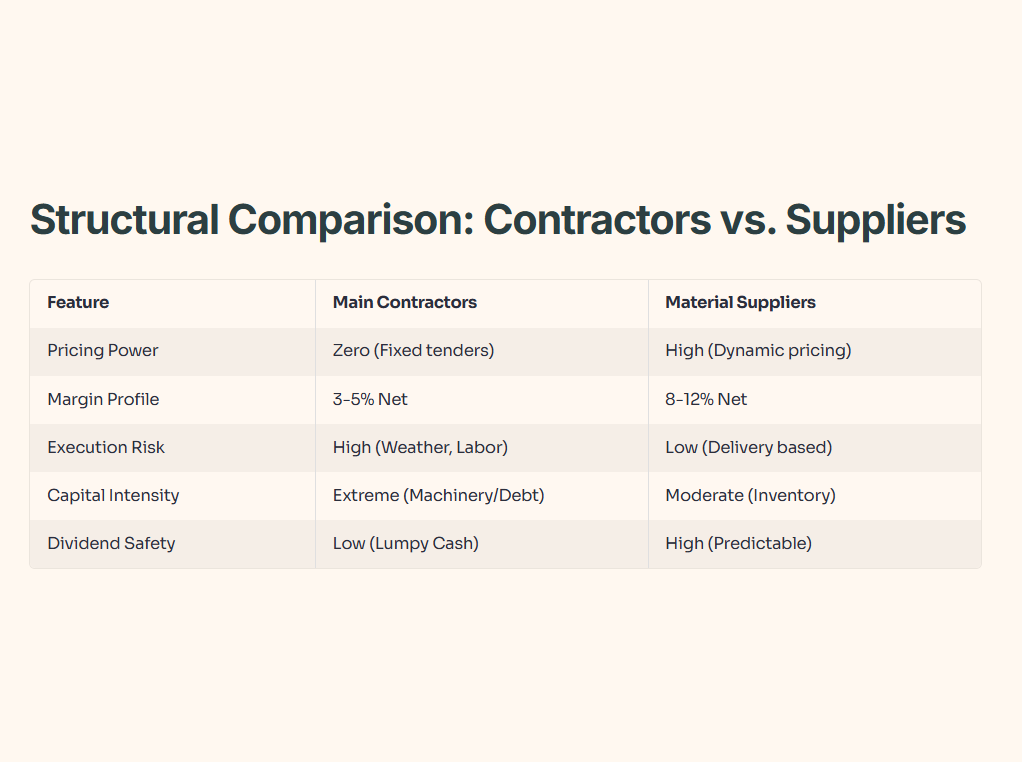

Table 1: Structural Comparison: Contractors vs. Suppliers

Analysing the “Why”: The table above highlights the fundamental divergence in business models. Main contractors operate on a “hope and pray” model where one site delay can wipe out years of profit. Notice the “Pricing Power” row: suppliers can pass through commodity spikes, whereas contractors are legally bound to their initial bid. This is why the Smart Money delisted Lian Beng and Chip Eng Seng; they knew public markets would never tolerate the volatility of fixed-price tender failures. For 2026, the $53B revenue figure only benefits the suppliers who get paid per ton delivered, not the contractors struggling with 1.2x gearing.

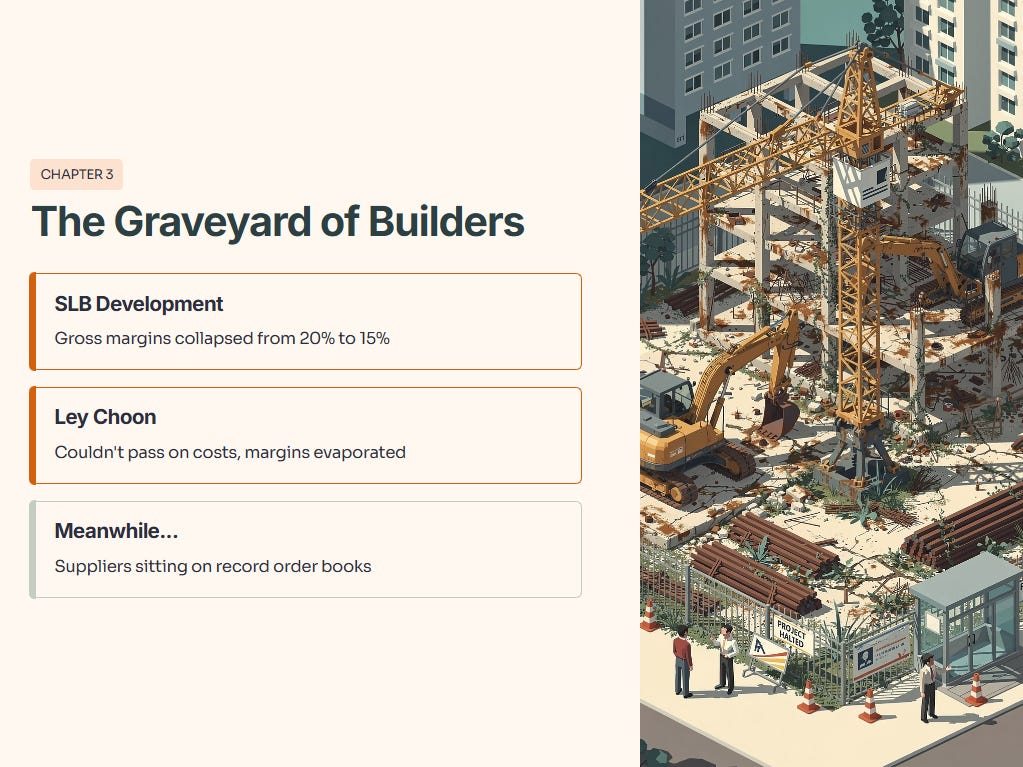

The Iggy Audit: Dissecting the Survivors

The market has punished the builders for a reason. Look at the “Graveyard” of firms like SLB Development or Ley Choon. Their gross margins fell from 20% to nearly 15% because they couldn’t pass on costs. Meanwhile, the suppliers are sitting on record order books.

BRC Asia (SGX:BEC) is the undisputed heavyweight here. Their order book just hit $1.9 billion, a 36% YoY increase. This isn’t just “projected” work; this is contracted steel for T5 and MBS expansion. While InvestingPro flags their weak gross profit margins, the stock has delivered a high return over the last year. This second-order effect is critical: in a boom, volume is the primary driver of EPS, not margin expansion. As Singapore pushes for greener buildings, BRC Asia’s low-carbon steel fabrication becomes a defensive moat that contractors simply cannot replicate.

Table 2: Peer Comparison (2026 Projections)

Analysis of the Audit

The winner is undeniably BRC Asia. While the P/B ratio of 1.4x suggests it’s “more expensive” than a generic contractor trading at 0.4x book value, the latter is a Value Trap. A contractor trading at 0.4x book reflects the market’s fear of hidden liabilities and asset impairments. BRC Asia’s higher valuation is justified by its “Great Performance” ranking (4/5) in Financial Health and its dominance in the steel rebar market.

The loser is the generic contractor. With a gearing ratio often exceeding 1.2, they are hyper-sensitive to interest rate fluctuations. In 2026, their interest expense alone can cannibalize their entire 3% net margin. If you are holding a builder hoping for a recovery, you are effectively gambling on interest rate cuts and perfect project execution—two things I wouldn’t bet my CPF on.

The Data Fortress: Is the Dividend a Mirage?

We need to look at the Dividend Ledger. A yield is only as good as the cash backing it. BRC Asia recently signaled its strength with a $0.07 special dividend.