Will CapitaLand & Mapletree Merge? $100B SG Giant Explained (and what it means for SG investors)

Explore what a $195 billion property powerhouse means for your REIT yields, concentration risk, and the smart moves you can make right now—before headlines turn into reality.

The Rumor That’s Shaking Singapore’s Real Estate World

Last week, word broke that CapitaLand Investment (CLI) and Mapletree Investments—two of Singapore’s most influential property giants—are in early-stage talks about a potential merger. The combined company would manage around US$150 billion (S$195 billion) in assets across REITs, private funds, logistics, commercial properties, and student housing.

Sounds massive, right? That’s because it is.

But here’s the thing: both companies have remained silent. Temasek Holdings, which owns Mapletree and is the largest shareholder in CLI, hasn’t confirmed anything. However, this shouldn’t be dismissed as idle market gossip.

This move aligns perfectly with Temasek’s long-standing strategy of merging its portfolio companies to create larger, more globally competitive “national champions.” That context elevates this from a rumor to a credible strategic possibility.

Yes, the discussions are exploratory, non-binding, and may never happen.

So why should you care? Because if this deal moves forward, it could shift the entire landscape of Singapore REITs, your portfolio’s diversification, and the yields you depend on. Understanding the risks now means you’re ready—whether the deal closes or falls apart.

In This Article:

• The Rumor That’s Shaking Singapore’s Real estate World

• What Would This Merger Actually Look Like?

• The Concentration Risk Nobody’s Talking About Openly

• Will Dividends Stay Safe, or Face the Merger Chop?

• The Real Risks Nobody’s Pricing In Yet

• What’s the Synergy Story, Really?

• Practical Actions for Singapore Retail Investors Right Now

• The Bigger Picture: Is This Deal Good for Singapore Investors?

• Your Sharp Takeaways

• What’s NextWhat Would This Merger Actually Look Like?

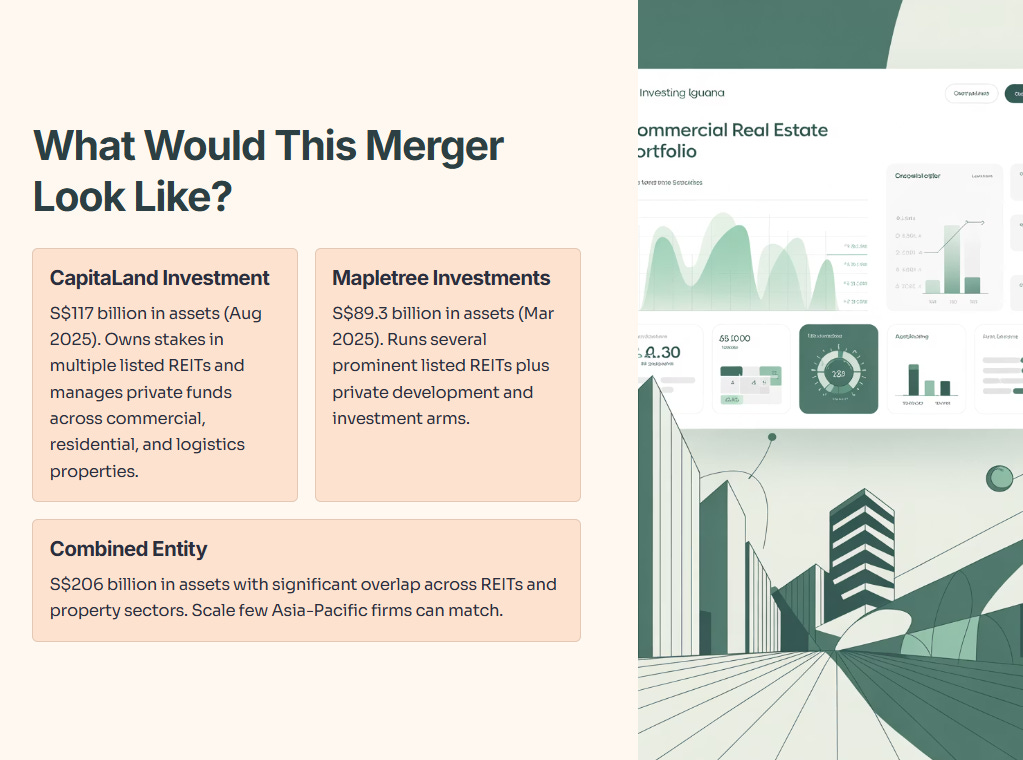

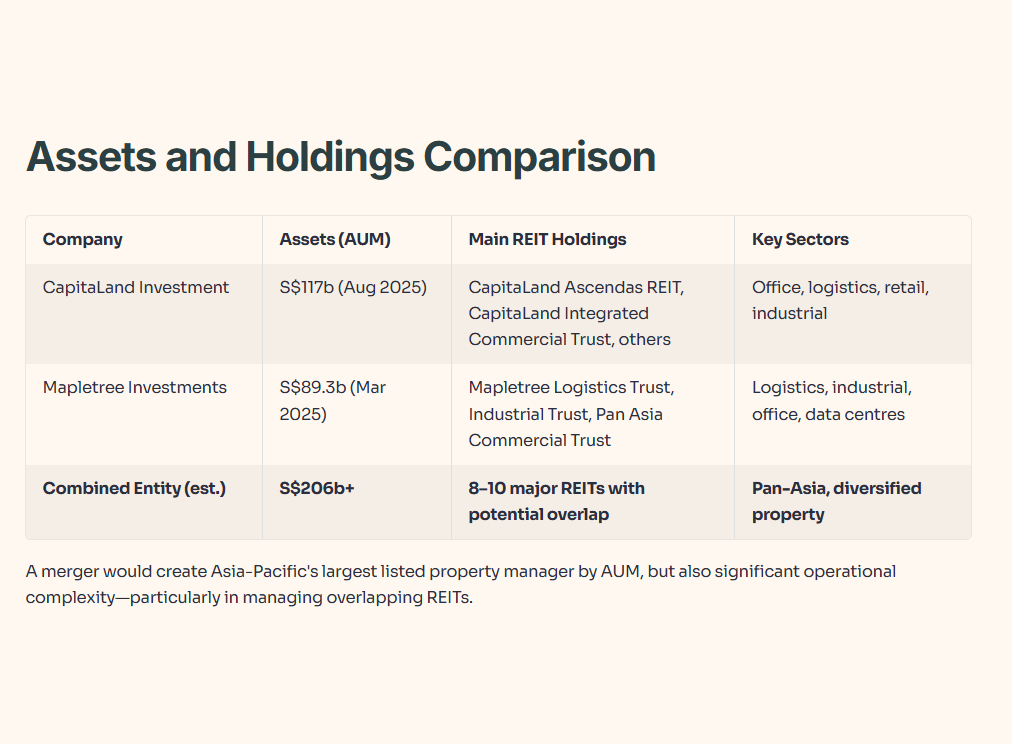

CapitaLand Investment is Singapore’s listed property powerhouse. As of August 2025, it managed S$117 billion in assets. It owns stakes in multiple listed REITs and manages private funds focused on commercial, residential, and logistics properties across Asia and beyond.

Mapletree Investments, fully owned by Temasek, manages S$89.3 billion in assets as of March 2025. Mapletree runs several prominent listed REITs—Mapletree Logistics Trust, Mapletree Industrial Trust, and Mapletree Pan Asia Commercial Trust—plus private development and investment arms.

If they merged, you’d have a combined entity with S$206 billion in assets, significant overlap across REITs and property sectors, and the ability to operate at a scale few real estate firms in the Asia-Pacific can match. The cost savings alone would be substantial. But merging is never as clean as the PowerPoint slides suggest.

Table 1: AUM and Key Holdings Comparison. This table shows the scale and asset composition of both firms. A merger would create Asia-Pacific’s largest listed property manager by AUM, but also create significant operational complexity—particularly in how many overlapping REITs would be managed or consolidated.

The Concentration Risk Nobody’s Talking About Openly

Here’s a hard truth: Singapore’s REIT market is already concentrated. A handful of big players dominate the listing. Fewer independent operators means less choice for investors and more market power concentrated in fewer hands.

Right now, you can diversify across multiple managers—CapitaLand, Mapletree, Frasers, Keppel, and others. Each brings its own strategy, governance, and risk appetite. If CapitaLand and Mapletree merge, you lose that independence. Suddenly, one entity controls an even bigger slice of Singapore’s listed property pie.

Let’s say you own three Mapletree REITs and two CapitaLand REITs today. You feel diversified. But if they merge under one holding company, your exposure to a single management philosophy, a single board, and a single set of strategic bets grows dramatically. That’s concentration masquerading as diversification.

The question becomes: If one merged entity stumbles—bad acquisition, management turnover, regulatory issues—how many of your properties are affected? Answer: all of them.

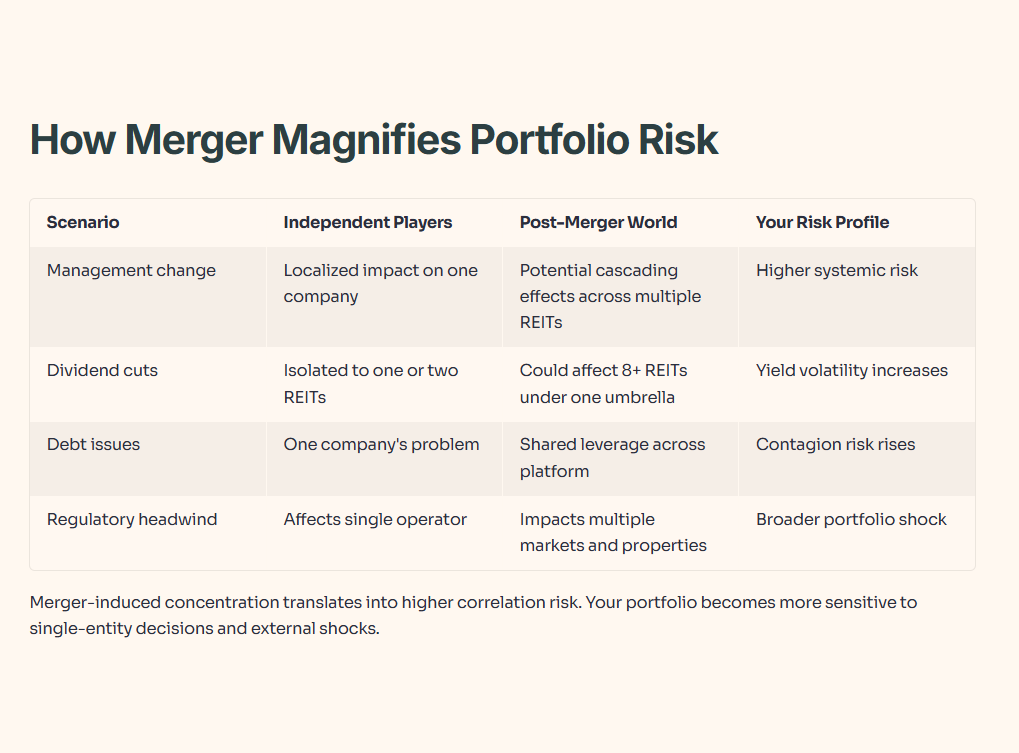

Table 2: How a Merger Could Magnify Portfolio Risk. This table illustrates how merger-induced concentration translates into higher correlation risk. Instead of managing independent bets, your portfolio becomes more sensitive to single-entity decisions and external shocks.

Will Dividends Stay Safe, or Face the Merger Chop?

This is the question keeping REIT investors awake at night.

The Bull Case: Bigger platforms generate efficiency. Back-office consolidation, smarter capital allocation, shared deal-sourcing—these could fatten margins and support dividends. History shows that well-executed property mergers sometimes boost payout stability by reducing costs and improving asset utilization.

The Bear Case: Integration is messy. During the merger year and the two years after, management gets distracted. You see asset sales to fund the deal, dividend holds to preserve balance sheet strength, and unexpected costs. Look at past major Singapore M&A in real estate—even successful deals often involve distribution freezes or modest cuts in the first 18–24 months.

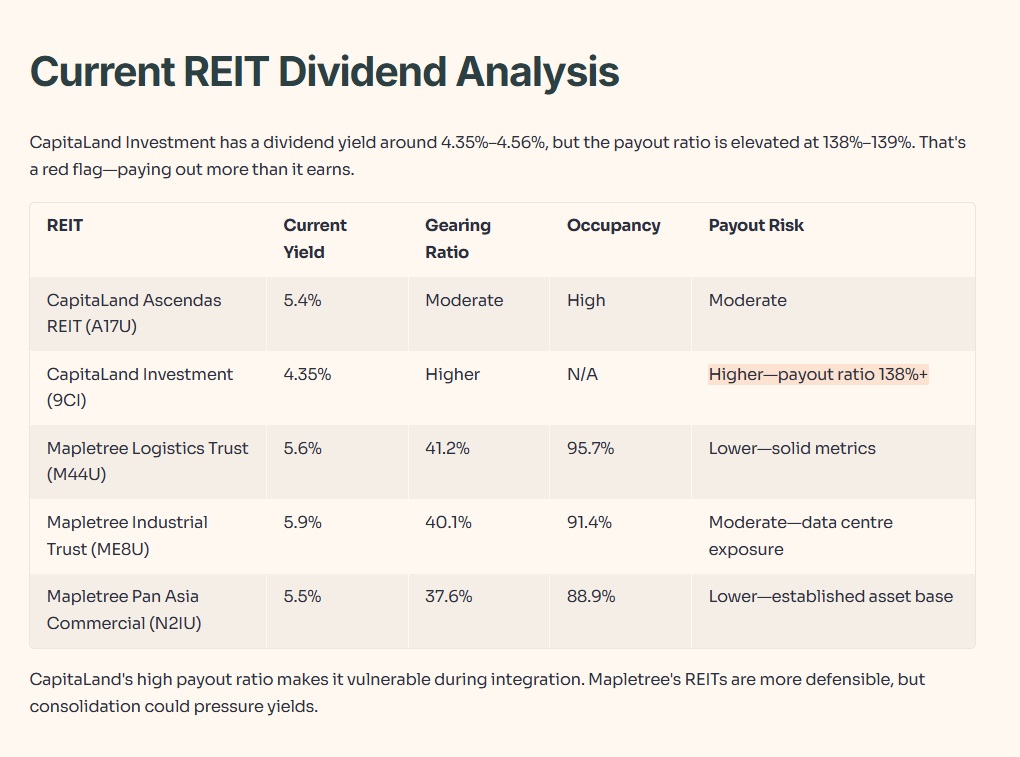

Let’s look at dividend data. CapitaLand Investment has a current dividend yield around 4.35%–4.56% per share, but the payout ratio is elevated—somewhere around 138%–139%. That’s a red flag. It means CapitaLand is paying out more than it earns, relying on asset disposals and financing to fund dividends. High payout ratios leave little room for a dividend cut if things tighten.

Mapletree REITs have shown more resilience. Mapletree Logistics Trust yields 5.6%, Mapletree Industrial Trust 5.9%, and Mapletree Pan Asia Commercial Trust 5.5%. Their gearing is moderate (37%–41%), and occupancy is solid. But their distributions have been under pressure from higher interest rates in recent years.

The table reveals a key insight: CapitaLand Investment’s high payout ratio makes it vulnerable during integration turbulence. Mapletree’s REITs are more defensible, but consolidation could pressure their yields if the merged entity prioritizes debt reduction or capital recycling over distributions.

The Real Risks Nobody’s Pricing In Yet

Complexity and Integration: Merging two massive platforms isn’t like combining two small startups. You’re talking about 8–10 publicly listed REITs, separate management teams, overlapping tenant bases, and different operational cultures. The integration roadmap alone could take 24 months.

Minority Shareholder Pushback: CapitaLand Investment is publicly listed. Its minority shareholders will demand clarity on the merger’s terms, the governance structure of the combined entity, and how their dividends will be protected. Expect activist questions and possible resistance at shareholder meetings.

Regulatory Headwinds: Singapore’s Monetary Authority (MAS) regulates REITs closely. Any merger involving major REIT consolidation will face scrutiny—especially around leverage ratios, interest coverage, and market concentration. MAS won’t sign off on anything that threatens financial stability or systemic risk.

Sector Overlap and Rationalisation: If the merged entity owns two office buildings on the same street or three logistics hubs serving the same region, something has to give. Asset sales mean one-time costs, potential capital gains tax, and tenant disruption. Alternatively, they might consolidate some REITs, privatizing smaller ones—which would erase your listing and force you into a cash-out scenario.

Macro Headwind: Interest rates are volatile. If rates stay high, the cost of integration debt becomes punishing. If rates fall sharply, that’s a tail wind, but timing is uncertain.

What’s the Synergy Story, Really?

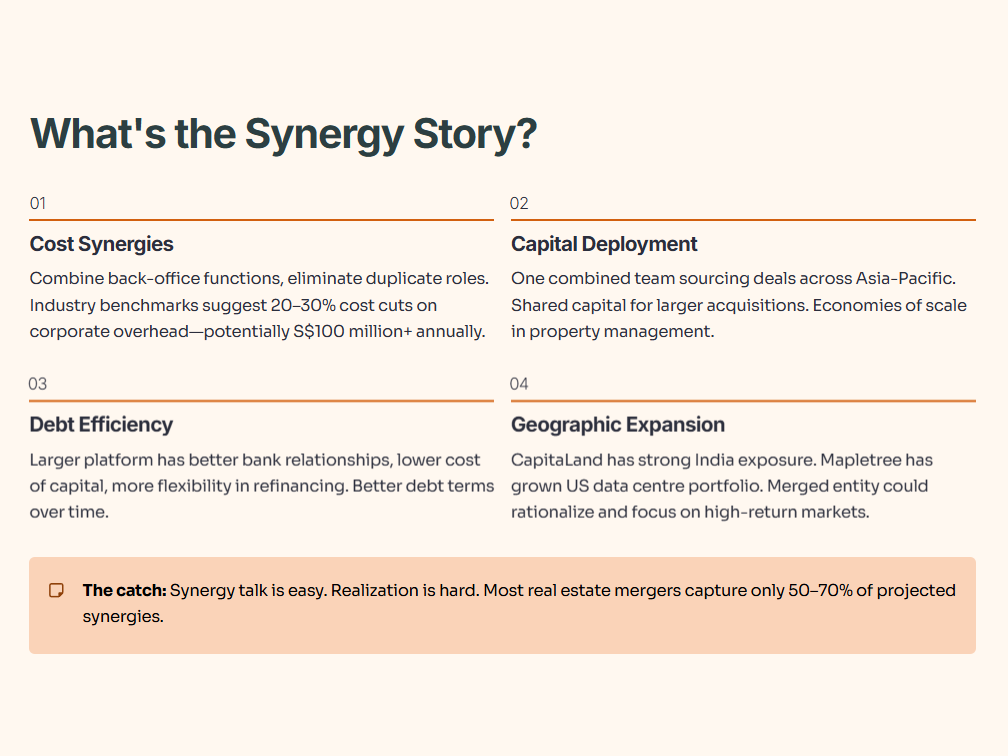

Here’s what a merged CapitaLand-Mapletree could theoretically achieve:

Cost Synergies: Combine back-office functions, eliminate duplicate roles in finance, legal, and HR, negotiate better terms with service providers. Industry benchmarks suggest 20–30% cost cuts on corporate overhead. That’s real money—potentially S$100 million+ annually.

Capital Deployment: One combined team sourcing deals across Asia-Pacific. Shared capital for larger acquisitions. Economies of scale in property management and tenant services.

Debt Efficiency: A larger platform has better bank relationships, lower cost of capital, and more flexibility in refinancing. Over time, that translates to better debt terms.

Geographic Expansion: CapitaLand already has strong India exposure. Mapletree has grown its US data centre portfolio. A merged entity could rationalize and focus on high-return markets more efficiently.

But here’s the catch: synergy talk is easy. Realization is hard. Most mergers in real estate capture 50–70% of projected synergies. The rest gets eaten by integration costs, market disruption, and execution delays.

Practical Actions for Singapore Retail Investors Right Now

You don’t need to panic or sell everything. But you do need a plan. Here’s what to do: