Fraud, Fines, and Fear: Is the Wilmar Thesis Broken? (3 Good, 3 Red Flags)🦖EP1295

A Chinese court just handed Wilmar a S$345 million bill. Here is why the “boring” blue chip is now a high-stakes governance play.

One of Singapore’s most important blue chips just had a Chinese court say its subsidiary helped cause S$345 million of losses in a contract fraud case. For Singapore investors who see Wilmar as the “boring” food and palm oil giant in their CPF or SRS, this is no longer a sleepy yield play—it is headline risk, legal risk, and opportunity, all rolled into one.

Right now, the real question for SGX holders is simple: is this the start of a structural crack in Wilmar, or a classic “good business, bad headline” setup where patient investors get paid to wait?

When you combine China fraud headlines, an earlier graft-related hit in Indonesia, and a stock stuck around multi‑year lows, it is normal to feel confused about whether to buy the dip, cut losses, or just ignore it.

This deep dive will walk through Wilmar International (SGX: F34) using one clear lens: 3 Good, 3 Red Flags, and a final Buy/Hold/Sell verdict. We are going beyond the headlines to look at the balance sheet mechanics that will determine your returns.

In This Article:

• The Data: Valuation & Income Snapshot

• The 3 Good: Why The Bulls Are Holding On

• Good #1: The “Sum-of-the-Parts” Arbitrage

• Good #2: Resilience in the “Real Economy”

• Good #3: The Dividend is Covered (For Now)

• The 3 Red Flags: Why The Bears Are worried

• Red Flag #1: The “Governance Tax” & Subsidiary Risk

• Red Flag #2: High Leverage in a High-Rate World

• Red Flag #3: It’s NOT a “Sleep Well at Night” Stock

• Iggy’s Verdict and StrategyThe Data: Valuation & Income Snapshot

Before we analyze the “Why,” let’s look at the “What.” Here is where Wilmar stands today (late 2025 data).

The 3 Good: Why The Bulls Are Holding On

Good #1: The “Sum-of-the-Parts” Arbitrage

This is the strongest mathematical argument for owning Wilmar. Wilmar is a holding company. It owns ~90% of Yihai Kerry Arawana (listed in China) and a majority stake in Adani Wilmar (listed in India).

Because Chinese and Indian investors give those local stocks high valuations (often 30x+ P/E), the market value of Wilmar’s stakes in those two companies is often higher than Wilmar’s entire market cap on the SGX.

This means when you buy Wilmar at S$3.00, you are effectively buying their China and India businesses at a discount, and getting their global palm oil, sugar, and shipping businesses for free.

Iggy’s Insight:

This is a classic “Kong Hee Fatt Choy” discount—where the conglomerate structure hides the true value. The market is penalizing Wilmar because of the “Singapore holding company discount.” If management ever decides to spin off assets or unbundle, the share price would legally have to rerate upwards to match the underlying assets. You are being paid a 5% yield to wait for value realization.

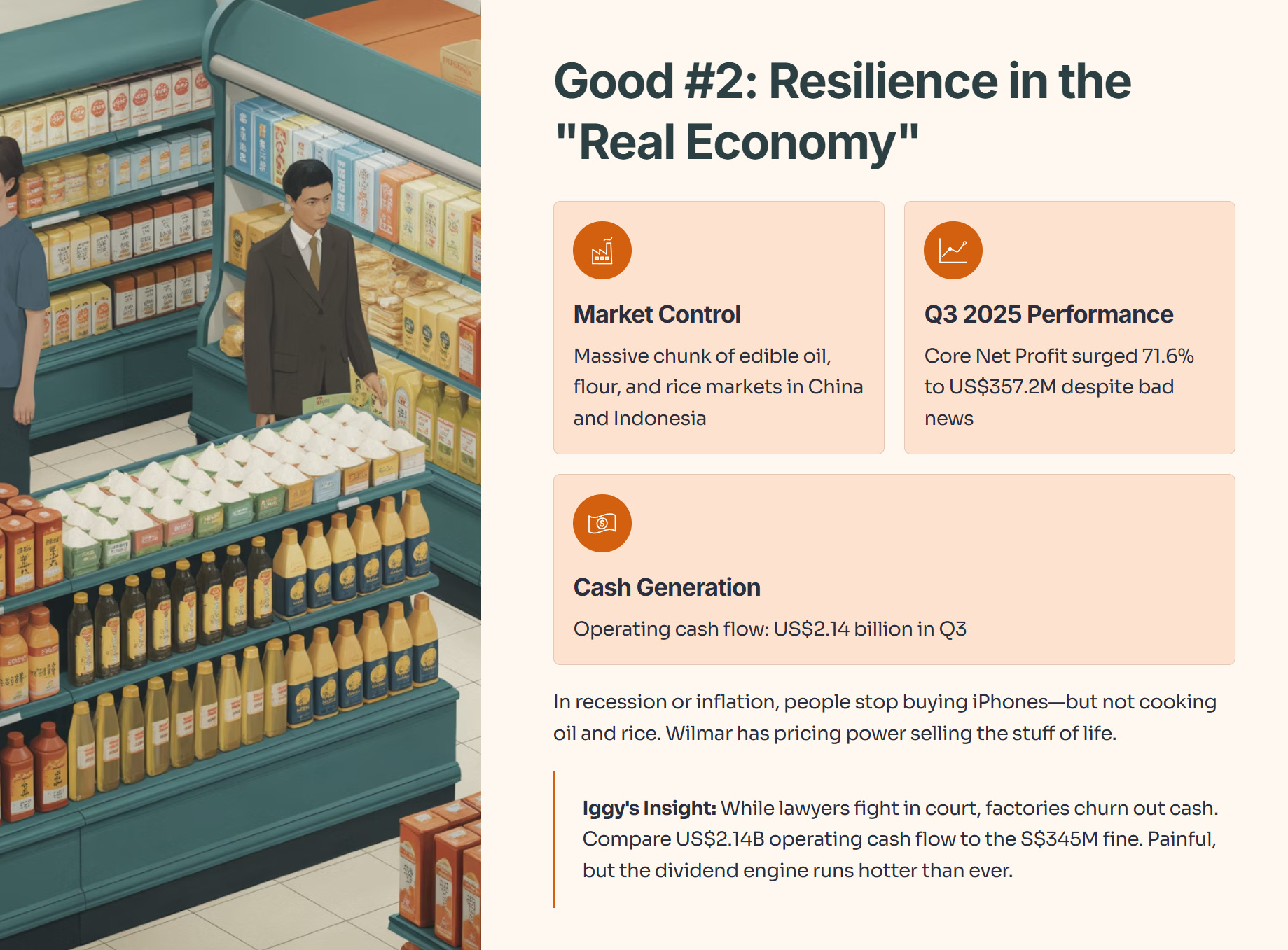

Good #2: Resilience in the “Real Economy”

Forget the legal drama for a moment. Look at the groceries. Wilmar controls a massive chunk of the edible oil, flour, and rice markets in China and Indonesia.

In Q3 2025, despite the bad news, Core Net Profit surged 71.6% to US$357.2 million. Why? because refining margins improved and sales volumes grew. In a recession or an inflationary environment, people might stop buying new iPhones, but they do not stop buying cooking oil and rice. Wilmar has pricing power because they sell the stuff of life.

Iggy’s Insight:

While the lawyers are fighting in court, the factories are still churning out cash. Operating cash flow in Q3 was a massive US$2.14 billion. Compare that to the S$345 million fine. The fine is painful, but the engine that pays your dividends is running hotter than ever.

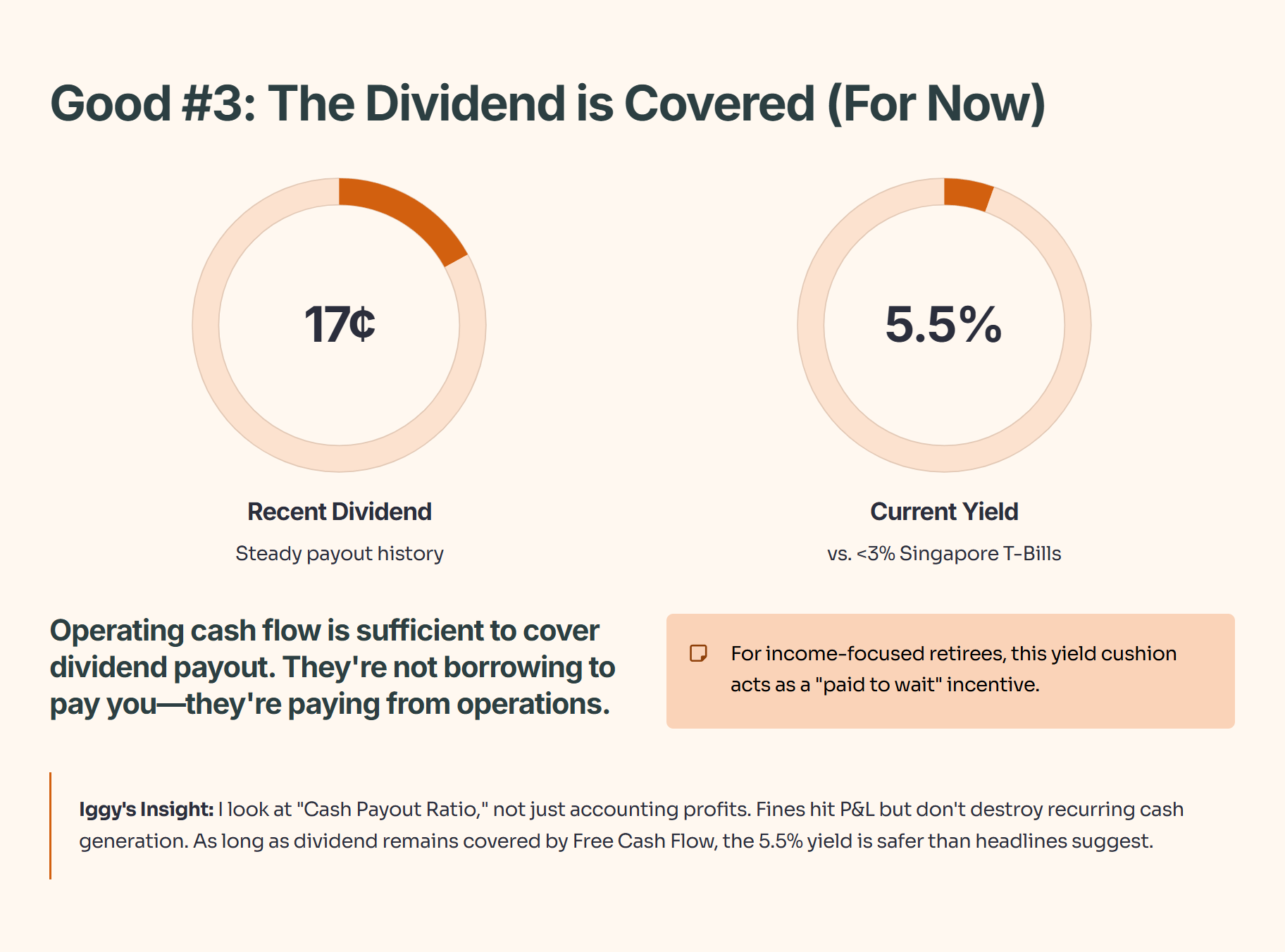

Good #3: The Dividend is Covered (For Now)

Wilmar has a history of paying steady dividends (approx. 17 cents SGD recently). Even with the “one-off” fines in Indonesia and China, the company’s operating cash flow is sufficient to cover the dividend payout.

They are not borrowing money to pay you; they are paying you from operations. At a ~5.5% yield, Wilmar offers a compelling spread over the Singapore T-Bill (which has dropped below 3%). For income-focused retirees, this yield cushion acts as a “paid to wait” incentive.

Iggy’s Insight:

I look at “Cash Payout Ratio,” not just accounting profits. Because the fines are “one-off” items, they hit the P&L statement, but they don’t destroy the recurring cash generating ability of the plants. As long as the dividend remains covered by Free Cash Flow, the 5.5% yield is safer than the headlines suggest.

The 3 Red Flags: Why The Bears Are worried

Red Flag #1: The “Governance Tax” & Subsidiary Risk

This is the elephant in the room. A S$345 million fraud verdict in China. A US$712 million graft penalty in Indonesia.

The problem isn’t just the money; it’s the span of control. Wilmar is huge, with thousands of subsidiaries. These penalties suggest that the Headquarters in Singapore may not have full visibility or control over what local managers in China or Indonesia are doing.

This creates a “Governance Tax.” Institutional investors (big funds) hate surprises. They will keep Wilmar’s valuation suppressed (low P/E) because they are terrified of the next headline.

Iggy’s Insight:

In emerging markets, size is a double-edged sword. You get scale, but you lose oversight. My fear isn’t that Wilmar goes bust; my fear is that every year, a new “one-off” fine eats up 10% of the profits. If “extraordinary items” happen every year, they aren’t extraordinary—they are a cost of doing business.

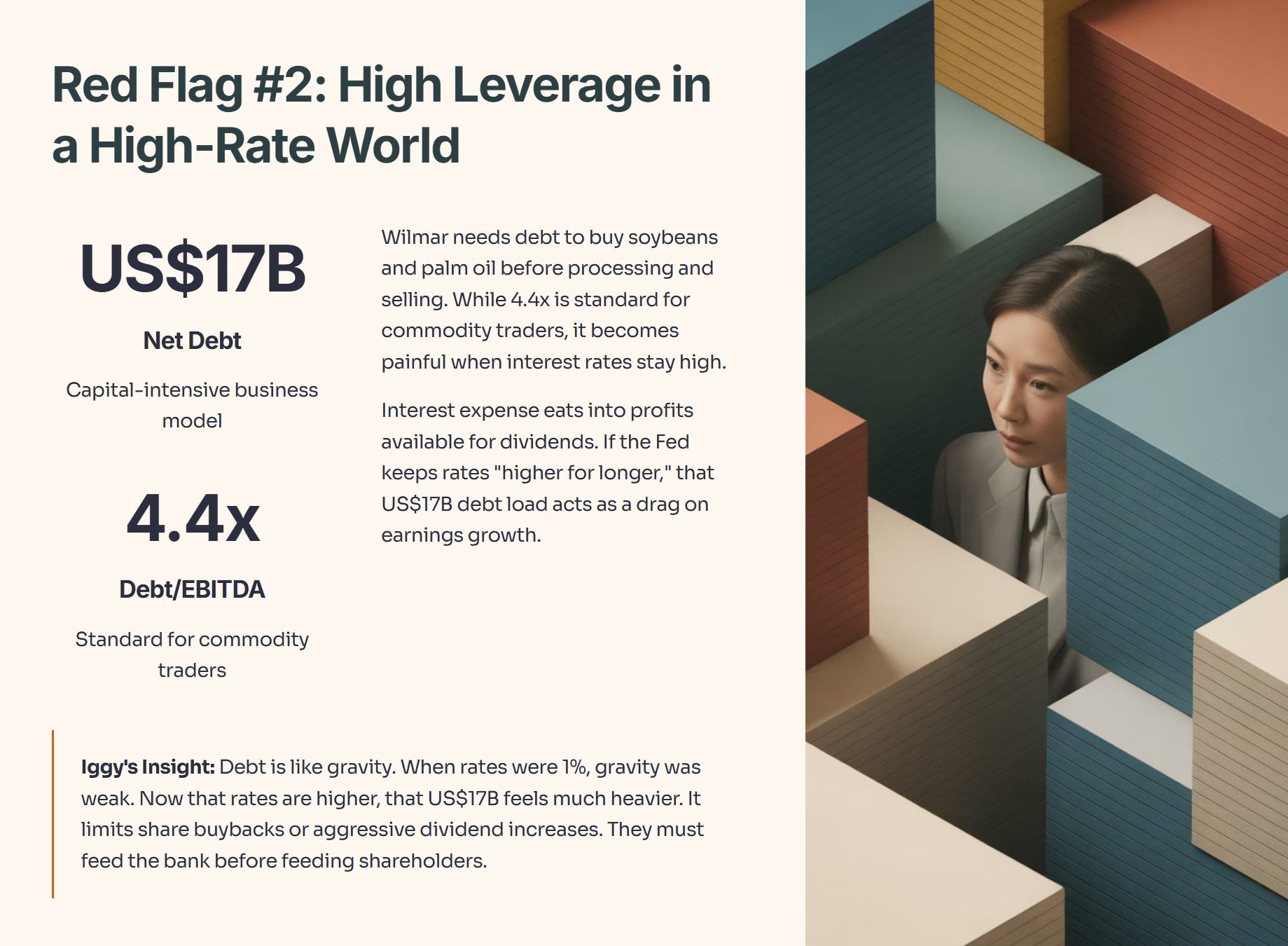

Red Flag #2: High Leverage in a High-Rate World

Wilmar is a capital-intensive business. They need debt to buy soybeans and palm oil before they process and sell them. Net Debt is around US$16.5 - 17.9 billion.

While a Net Debt/EBITDA of ~4.4x is standard for commodity traders (who use debt to fund liquid inventory), it becomes painful when interest rates stay high. Interest expense eats into the profits available for dividends. If the US Federal Reserve keeps rates “higher for longer,” Wilmar’s interest bill stays high, acting as a drag on earnings growth.

Iggy’s Insight:

Debt is like gravity. When rates were 1%, gravity was weak. Now that rates are higher, that US$17 billion debt load feels much heavier. It limits their ability to do share buybacks or increase dividends aggressively. They have to feed the bank before they feed us shareholders.

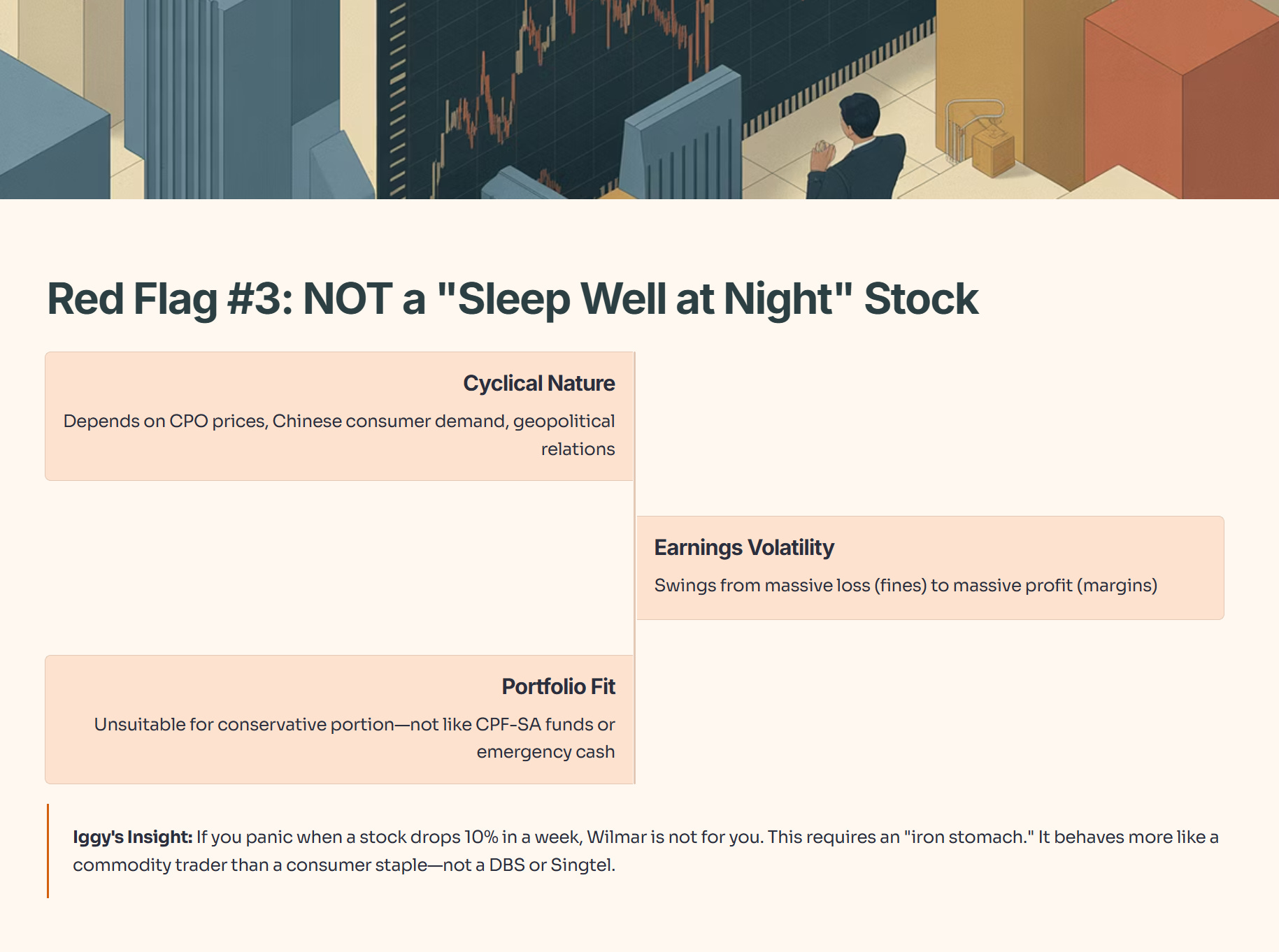

Red Flag #3: It’s NOT a “Sleep Well at Night” Stock

Many Singaporeans treat blue chips like “set and forget” assets. Wilmar is not that. It is cyclical. It depends on Crude Palm Oil (CPO) prices, Chinese consumer demand, and geopolitical relations between nations.

The volatility in earnings—swinging from a massive loss (due to fines) to a massive profit (due to margins)—makes it unsuitable for the conservative portion of a portfolio (like CPF-SA funds or emergency cash).

Iggy’s Insight:

If you panic when a stock drops 10% in a week, Wilmar is not for you. This is a stock that requires an “iron stomach.” It is not a DBS or a Singtel. It behaves more like a commodity trader than a consumer staple.

Iggy’s Verdict and Strategy