Yangzijiang Shipbuilding: The 5.93% Yield Fortress the Retail Herd is Missing

How BS6's S$2.63 billion cash bunker protects your retirement drawdowns while local bank margins begin to freeze.

🚨 The bottom line for your wallet today

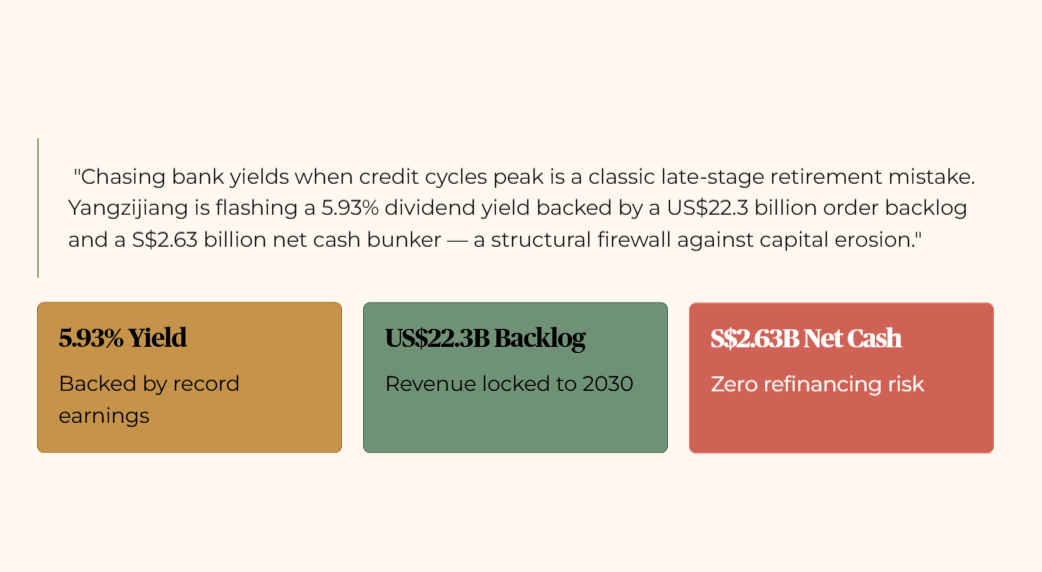

“Chasing bank yields when credit cycles peak is a classic late-stage retirement mistake. While local bank Net Interest Margins (NIM) begin to feel the squeeze from global interest rate easing, Yangzijiang Shipbuilding (SGX: BS6) is flashing a 5.93% dividend yield backed by a colossal US$22.3 billion order backlog and a S$2.63 billion net cash bunker. If your retirement drawdowns are heavily exposed to local financial counters, this industrial giant isn’t just an alternative—it is a structural firewall against capital erosion.”

In This Article:

Section 1: The financial health check

Section 2: The wealth audit (Yield and cash flow)

Section 3: The price check (Valuation)

Section 4: The dividend trajectory

Section 5: The forward stress-test (The ice storm scenario)

Section 6: The intuitive retirement verdict

The cold open: Look through the headline illusion

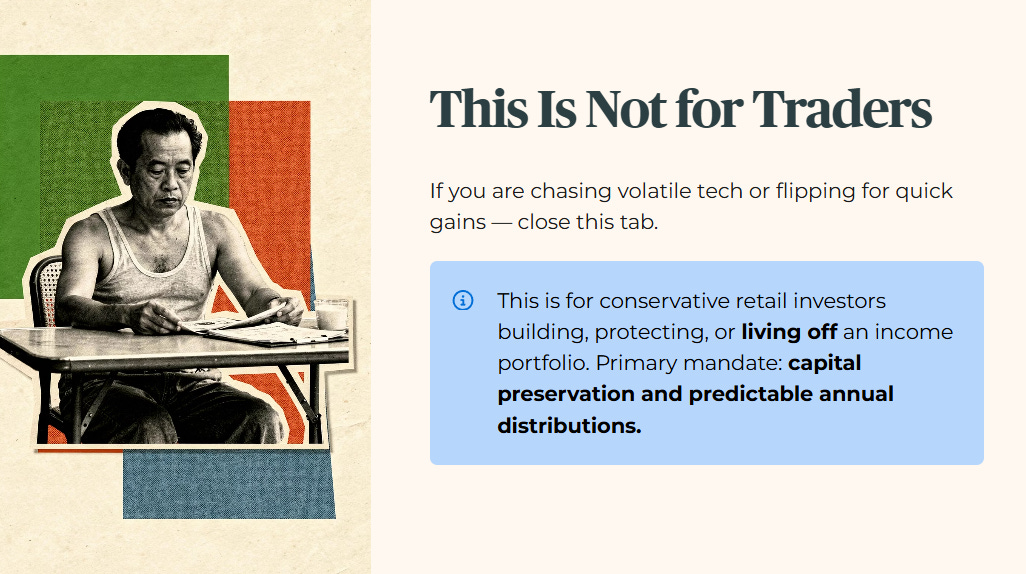

Listen to your Uncle here. If you are chasing hyper-volatile tech growth or scraping for short-term trading momentum to flip a fast buck, close this tab right now. This piece isn’t for you. Go back to your forums and hunt for memes.

But if you are a conservative retail investor—someone actively building, protecting, or living off an income portfolio—your primary mandate is simple: capital preservation and predictable annual distributions. My forensic standards are built to guard your hard-earned retirement savings, not to accommodate speculative plays.

The recent market correction has pushed a specific industrial counter straight into the crosshairs of my tracking radar. When the general retail public panics over short-term macroeconomic noise, the institutional money quietly looks at the plumbing. When a high-yield asset actually strengthens its underlying balance sheet during a global trade and geopolitical crisis, you don’t just watch it—you run the numbers.

My job is straightforward, even if corporate balance sheets are not. I read the forensic footnotes that the mainstream financial headlines skip entirely. I audit the interest coverage, the structural debt walls, and the genuine sustainability of free cash flow. Why? So that the average Singaporean trying to fund a comfortable lifestyle gets the exact same institutional-grade clarity that high-net-worth family offices take for granted.

Let’s dissect the raw reality of Yangzijiang Shipbuilding.

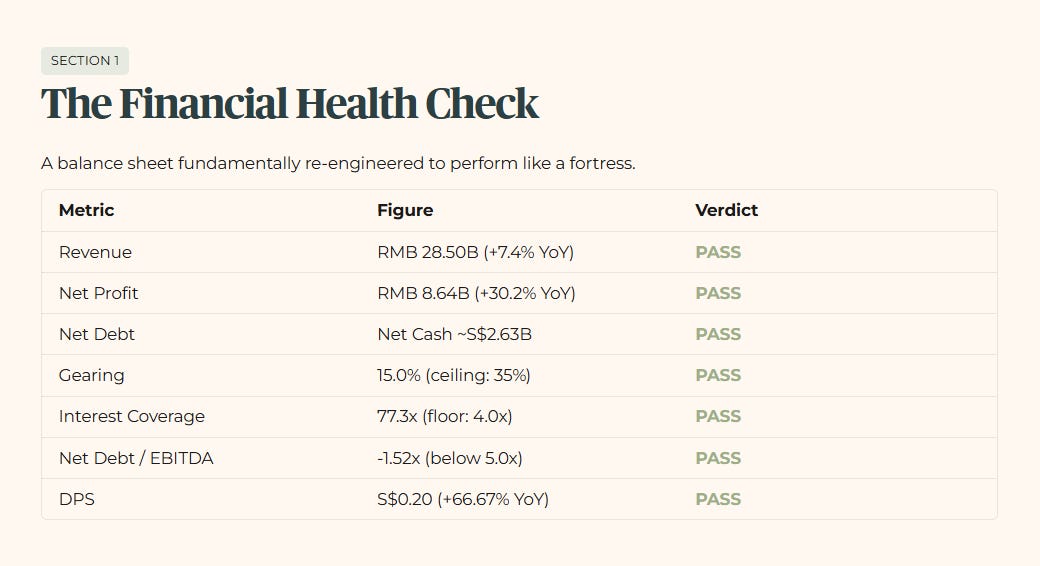

Section 1: The financial health check

This is an industrial balance sheet that has been fundamentally re-engineered to perform like an absolute fortress. We are no longer looking at the deeply cyclical, capital-starved yard operations of a decade ago.

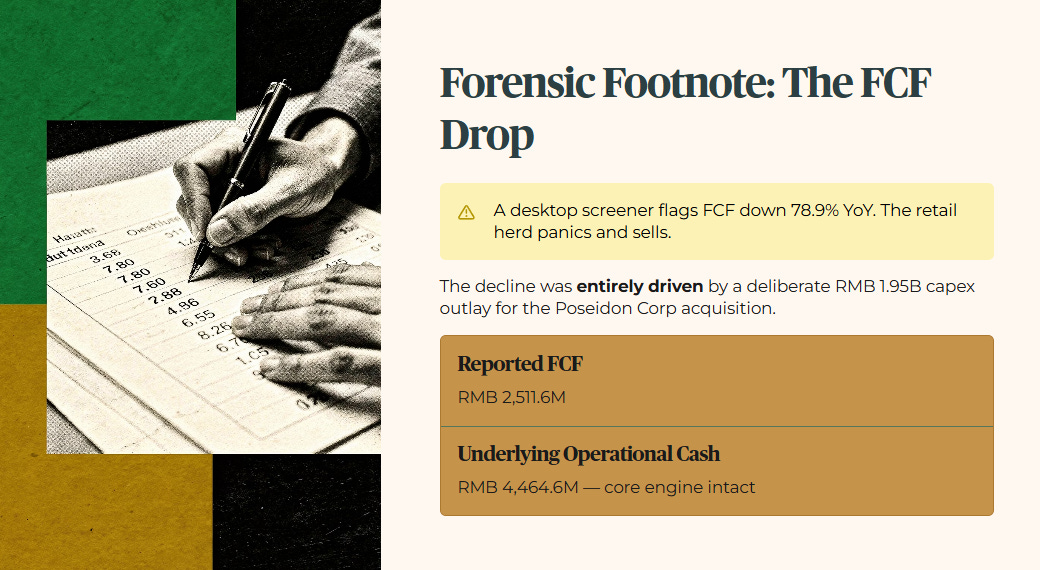

*Forensic Footnote on the Free Cash Flow Drop: A standard desktop screener will flag that Yangzijiang’s reported FCF declined by 78.9% YoY. The uneducated retail herd sees this, panics, and hits the sell button. But we look closer. This decline was entirely driven by a deliberate, strategic RMB 1.95 billion capex outlay used to fund the Poseidon Corp acquisition in FY2025. If you look at the underlying operational cash generation before this capital allocation, it sits at a robust RMB 4,464.6 million. The core cash-generating engine remains completely intact.

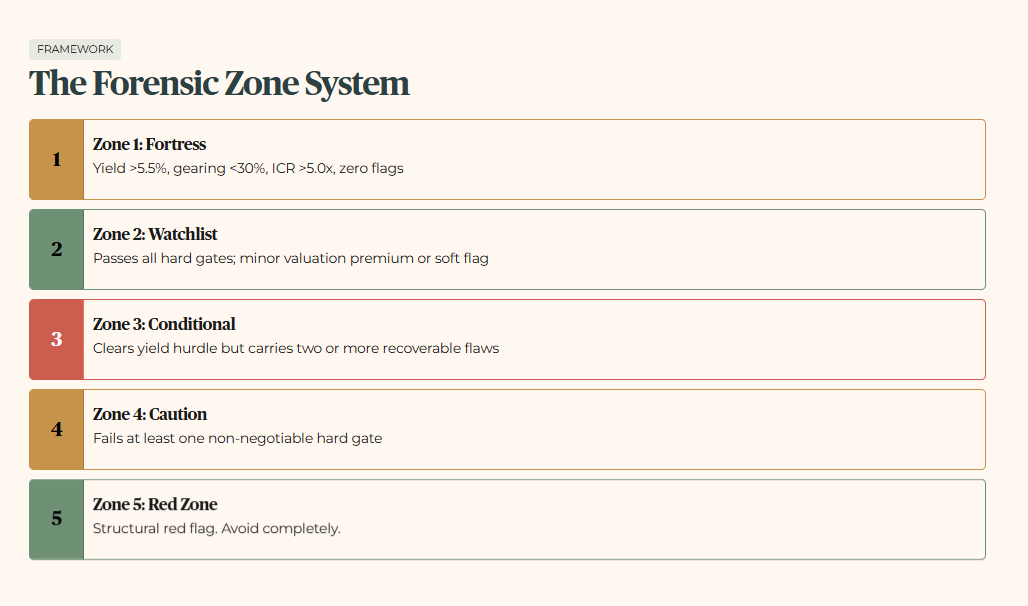

How Iggy rates the market: The Forensic Zone System

For the benefit of new readers, every single stock tracked inside my Second Brain is strictly assigned to a Forensic Zone. These are reject-first, think-later structural filters designed to remove human emotion from capital allocation.

Zone 1: Fortress – Retirement-grade sanctuary. Dividend yield above 5.5%, gearing strictly below 30%, Interest Coverage Ratio (ICR) above 5.0x, and absolutely zero structural or governance flags.

Zone 2: Watchlist – Passes every single hard forensic gate, but carries minor valuation premiums or soft flags that sit close to a threshold.

Zone 3: Conditional – Clears the minimum yield hurdle but carries two or more recoverable balance sheet or structural flaws.

Zone 4: Caution – Fails at least one non-negotiable hard gate. Capital is exposed to operational leakages.

Zone 5: Red Zone – Carries a structural red flag or a severe threat of capital liquidation. Full stop. Avoid completely.

Elite Investors receive zero-day access to the full forensic rationale, zone trajectory updates, and soft flag breakdowns for the entire SGX ecosystem.

Section 2: The wealth audit (Yield and cash flow)

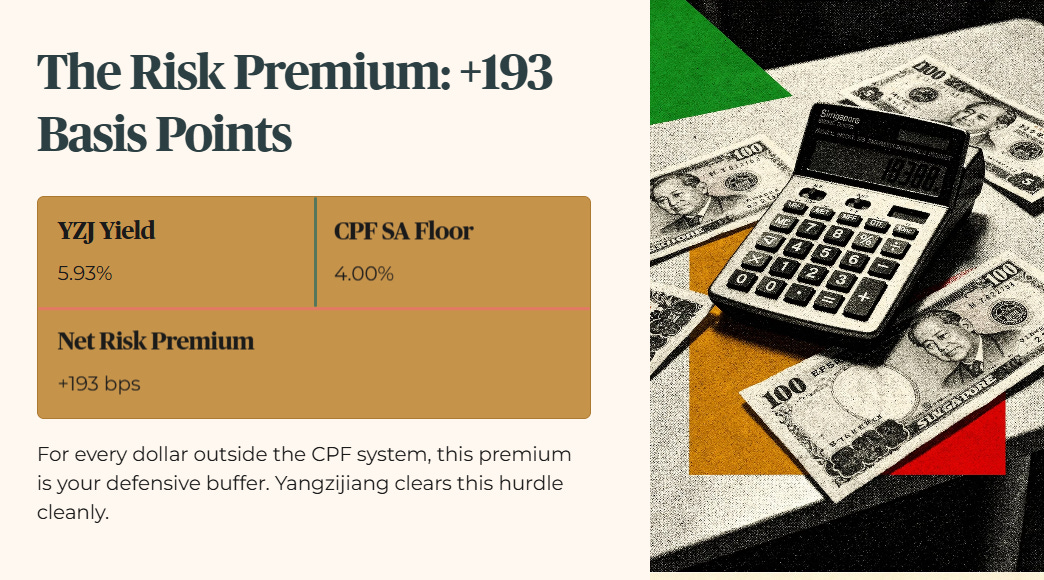

The current dividend yield stands at 5.93% based on a share price of S$3.47. To understand why this matters, you must understand exactly where your alternative risk-free sanctuary sits in late-2026.

The risk premium challenge

The Central Provident Fund Special Account (CPF SA) pays a rock-solid, guaranteed 4.0% floor in Q2 2026. It features zero company risk, zero distribution cuts, and absolutely zero price volatility. If you are going to take your money out of a government-guaranteed vehicle and expose it to the wild storms of the open stock market, you must demand a justifiable premium.

Yangzijiang Dividend Yield: 5.93%

- CPF Special Account Floor: 4.00%

---------------------------------------

= Real Net Risk Premium: +193 basis points

This 193-basis-point risk premium is the minimum psychological justification for owning equity here. For every dollar of personal capital sitting outside the safety of the CPF system, this premium represents your defensive buffer. Yangzijiang clears this hurdle cleanly.

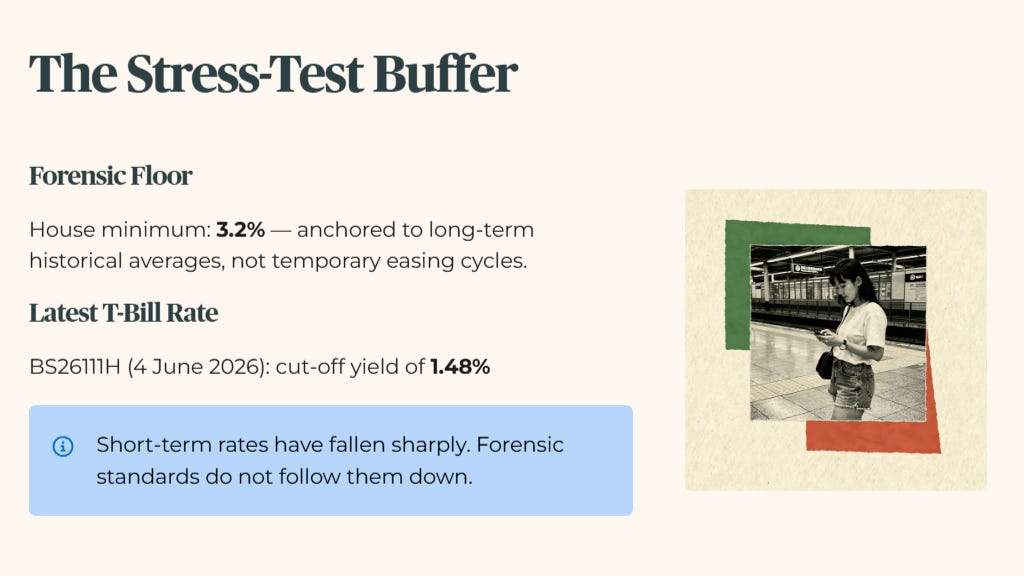

The stress-test buffer

We audit for the catastrophic storm, not for the beautifully sunny day. My house framework maintains a strict, conservative forensic floor of 3.2%. The latest Singapore 6-Month T-Bill auction (Issue Code: BS26111H, 4 June 2026) delivered a cut-off yield of 1.48%.

While short-term government rates have fallen significantly across the MAS curve, I refuse to lower my analytical standards to match a temporary market easing cycle. My forensic floor remains anchored at 3.2% to guarantee that our sanctuary assets can comfortably withstand a future return to long-term macroeconomic historical averages.

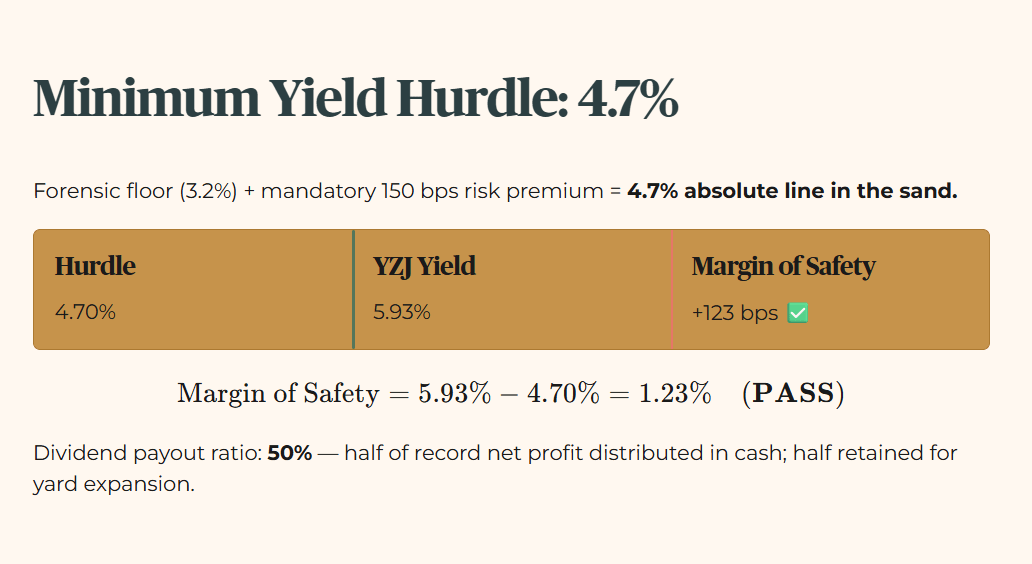

Our Minimum Acceptable Yield Hurdle is calculated as the 3.2% forensic floor plus a mandatory 150-basis-point risk premium. This sets our absolute line in the sand at 4.7%. Yangzijiang outpaces this minimum hurdle by a wide 123-basis-point margin.

[MINIMUM YIELD HURDLE: 4.7%] ---> [YANGZIJIANG AUDITED YIELD: 5.93%]

Margin of Safety=5.93%−4.70%=1.23%(PASS)

But the 1.23% margin of safety is only the first gate Yangzijiang clears cleanly; the next section drills into the 50% payout ratio and 77.3x interest coverage math that determines whether this 5.93% yield can actually survive the next credit cycle intact.