The "Cash Fortress" Stock With $23.2B in Orders (P/E 10)

The S$10 Billion Mirage: Is Yangzijiang’s Record Profit a Peak or a Plateau?

Investors are salivating over Yangzijiang’s (SGX: BS6) record-breaking profits, thinking they’ve found a compounding machine at a discount. But here is the “Smart Money” reality check: shipbuilding is a brutally cyclical game of timing, currency swings, and steel prices. If you’re buying in now because the rearview mirror looks shiny, you might be walking straight into a “Peak Earnings” trap. The record 30-35% margins aren’t a permanent feature; they are an alignment of the stars—low steel, high backlog, and a weak RMB. When those stars move, the fall is usually fast and painful.

In This Article:

The Concept Deep Dive: Operating Leverage & The “Margin Mirage”

The Iggy Audit: 3 Good & 3 Red Flags

The Data Fortress: Dividend and Health Assessment

The Scenario Matrix: 2026 Forecasts

InvestingPro Reality Check

The Verdict: The Action Plan🦎 About Iggy the Investing Iguana

Welcome to the Iguana Pit! If you’re new here, I’m Iggy: your guide through the dense jungle of the Singapore markets. My mission is simple: to spot the predators before they spot your portfolio.

We are now 5,800+ subscribers strong across YouTube and Substack, focusing purely on the data-driven alpha that mainstream media misses.

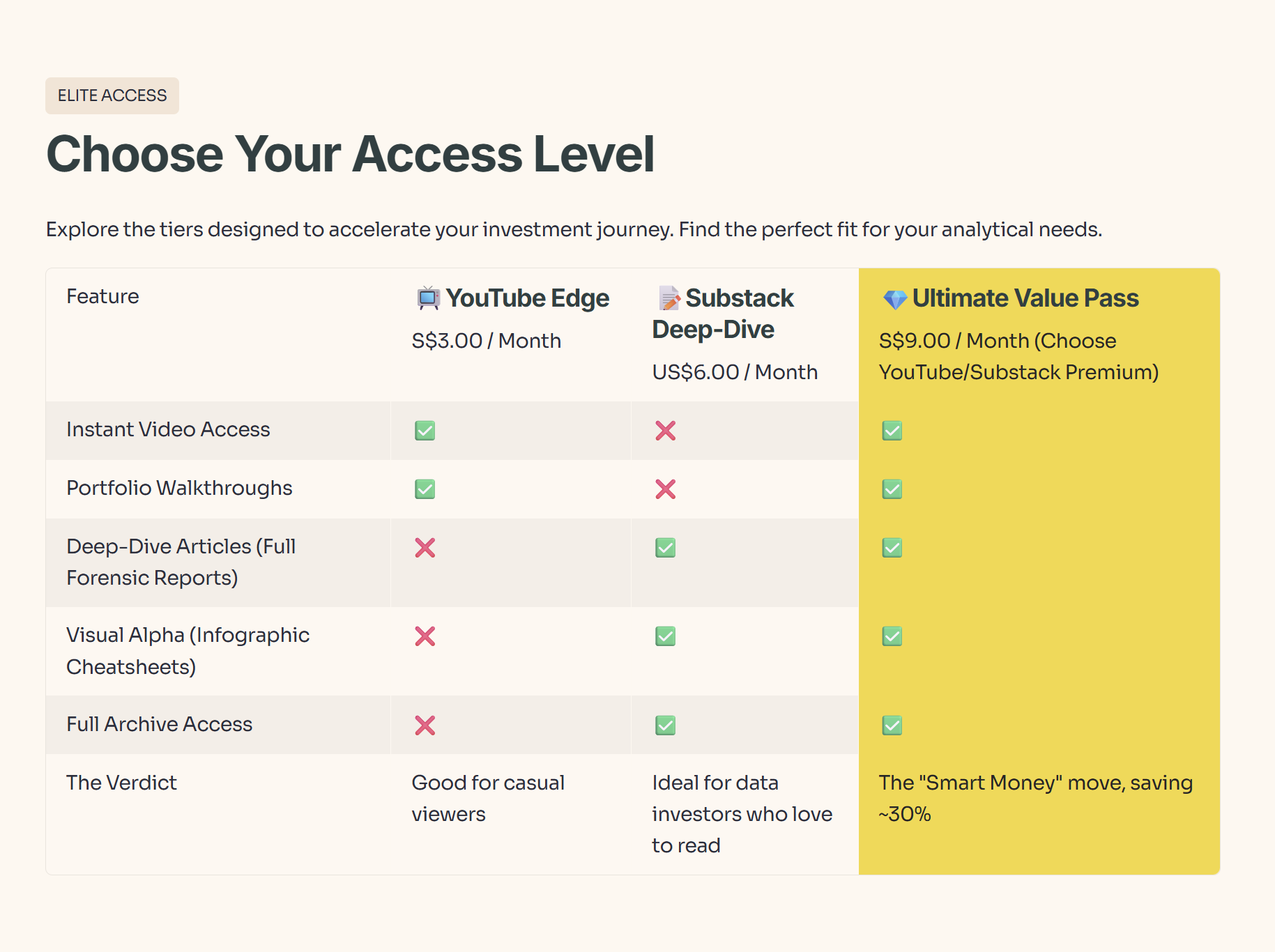

🚀 Join the “Elite 150” Inner Circle

Real alpha is found behind the velvet rope. Stop following the herd and start following the data with our 150+ paid members.

📺 The YouTube Edge (S$3/mo): Beat the Delay.

Instant Access: Watch new videos the moment they drop.

The Free Tier Trap: Free subscribers wait up to 14 days to see the same video. (By then, the news is old and the trade is gone).

📝 The Substack Deep-Dive (US$6/mo): Unlock the Vault.

Zero Paywalls: Read the full “Deep Dive” articles and “Substack Exclusive” articles found only on Substack.

Visual Alpha: Download exclusive Infographic Cheatsheets not available to free readers.

💎 The Ultimate Value Pass (S$9/mo): (BEST VALUE)

Get It All: Paid via YouTube, this bundle grants you Instant Video Access AND Full Substack Access.

The Math: You save ~30% compared to buying them separately. It’s the “Smart Money” move.

Why wait 2 weeks for old news? Get the data while it’s fresh. 👉 Join Here: https://www.youtube.com/@InvestingIguana/membership

The Concept Deep Dive: Operating Leverage & The “Margin Mirage”

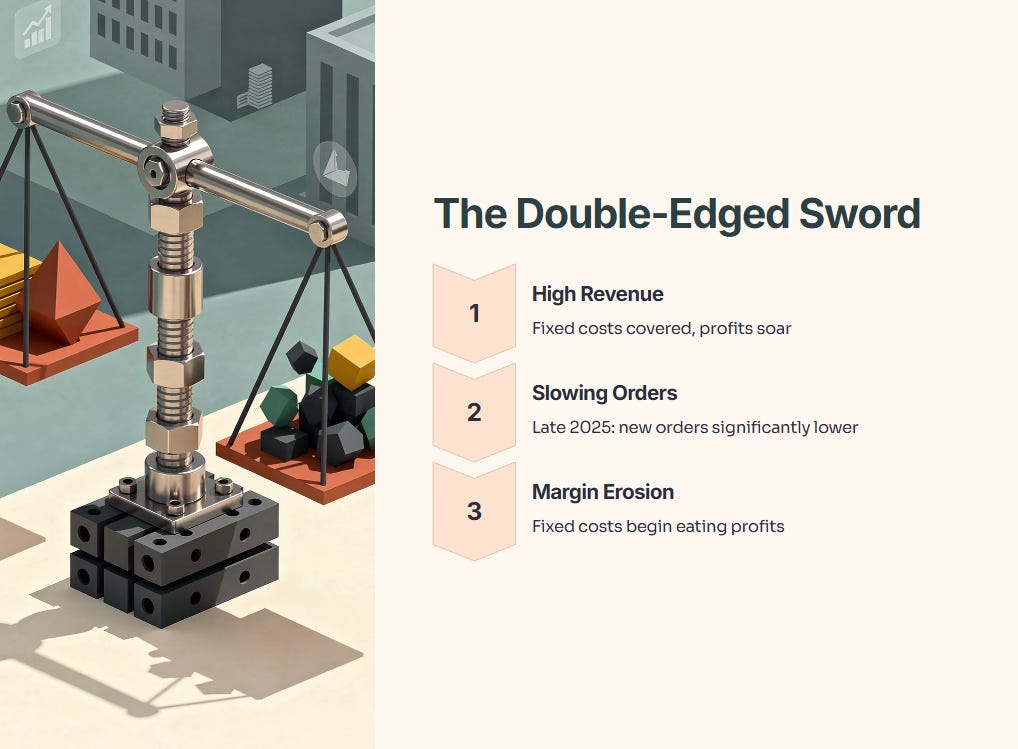

To understand Yangzijiang, you must master the concept of Operating Leverage. In heavy industries like shipbuilding, a massive portion of costs is fixed: the docks, the cranes, specialized labor, and administration. Once a yard covers these fixed costs, every additional dollar of revenue flows almost entirely to the bottom line. This is why YZJ’s net profit surged 37% in 1H2025 despite revenue dipping by 1%.

The “Mirage” occurs when investors assume these expanded margins are the new baseline. In 2024–2025, YZJ benefited from “legacy” high-priced contracts signed during the post-pandemic shipping crunch, while simultaneously enjoying a drop in Chinese domestic steel prices. This created a “Goldilocks” zone where Average Selling Price (ASP) remained high while input costs cratered. However, operating leverage is a double-edged sword. If the orderbook slows—as seen in late 2025 when new order wins were significantly lower than the prior year—the high fixed-cost base will begin to eat margins.

Furthermore, we must discuss “Revenue Lag.” A ship ordered today doesn’t show up in the P&L for 2–3 years. The record profits we see in 2026 are the ghost of 2023’s frantic ordering. If 2026 becomes a year of consolidation for shipowners, the “earnings cliff” in 2028 is already being built.

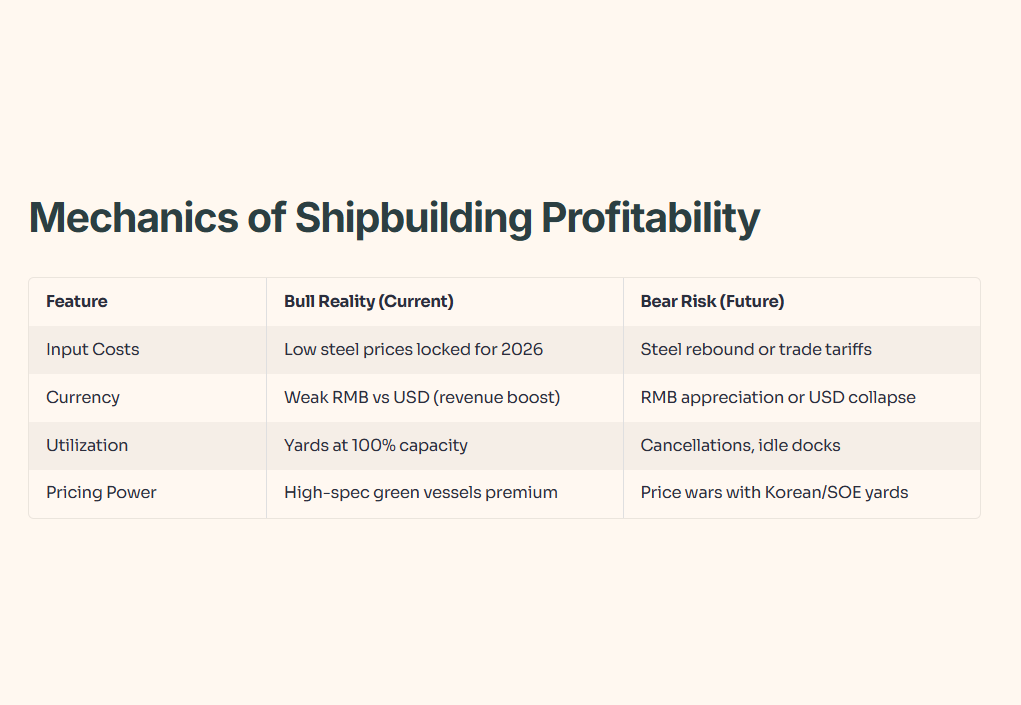

Mechanics of Shipbuilding Profitability

When you strip away the fancy charts, shipbuilding profitability is really a four‑lever machine: cheap Chinese steel and a weak RMB are turbo‑charging Yangzijiang’s margins today, but a rebound in steel or a sharp RMB move can flip that tailwind into drag almost overnight; full yards look great now because every extra ship drops fat profit on a largely fixed cost base, yet a wave of cancellations would leave the same docks and workers burning cash instead; and while high‑spec green vessels let YZJ charge premium prices in this cycle, a price war from Korean or state-backed yards would remind everyone that “pricing power” in shipping is a privilege, not a birthright.

The Iggy Audit: 3 Good & 3 Red Flags

The “3 Good”

Record Margin Expansion & Structural Cost Advantage: Shipbuilding gross margins hit record levels (~35%) due to lower steel costs and improved contract pricing. With most 2026 steel requirements already locked in, management is confident in maintaining these elevated margins in the medium term.

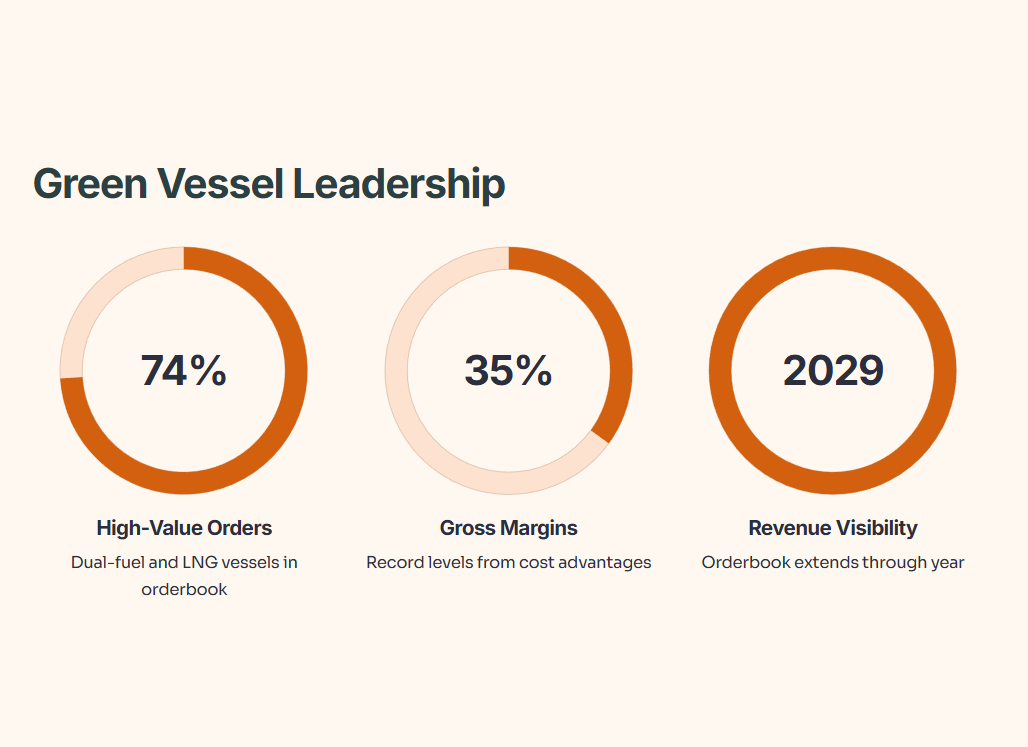

Staggering Orderbook Visibility: The total orderbook stands at a record US$23.2 billion, providing revenue visibility through 2029. Crucially, 74% of these orders are high-value “green” dual-fuel and LNG vessels, positioning YZJ as a leader in the industry’s decarbonization shift.

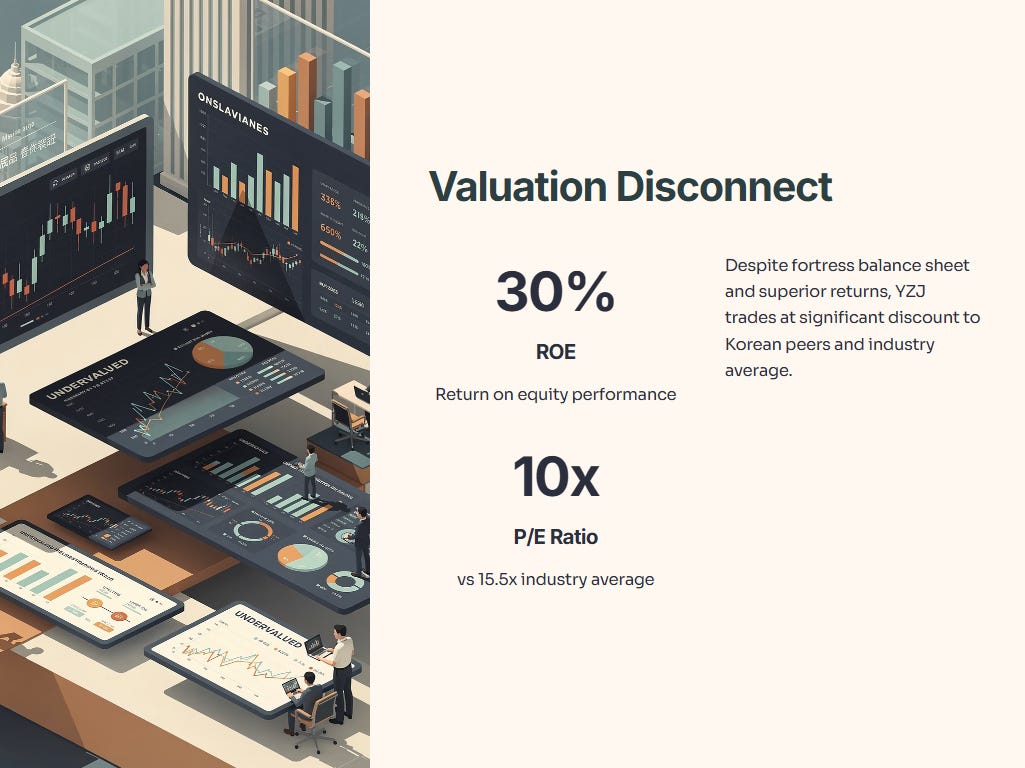

Fortress Balance Sheet & Peer Undervaluation: YZJ maintains a strong net cash position with cash exceeding total debt. Despite a 30% ROE, it trades at a P/E of ~10x, a significant discount compared to the industry average of 15.5x and its Korean peers.

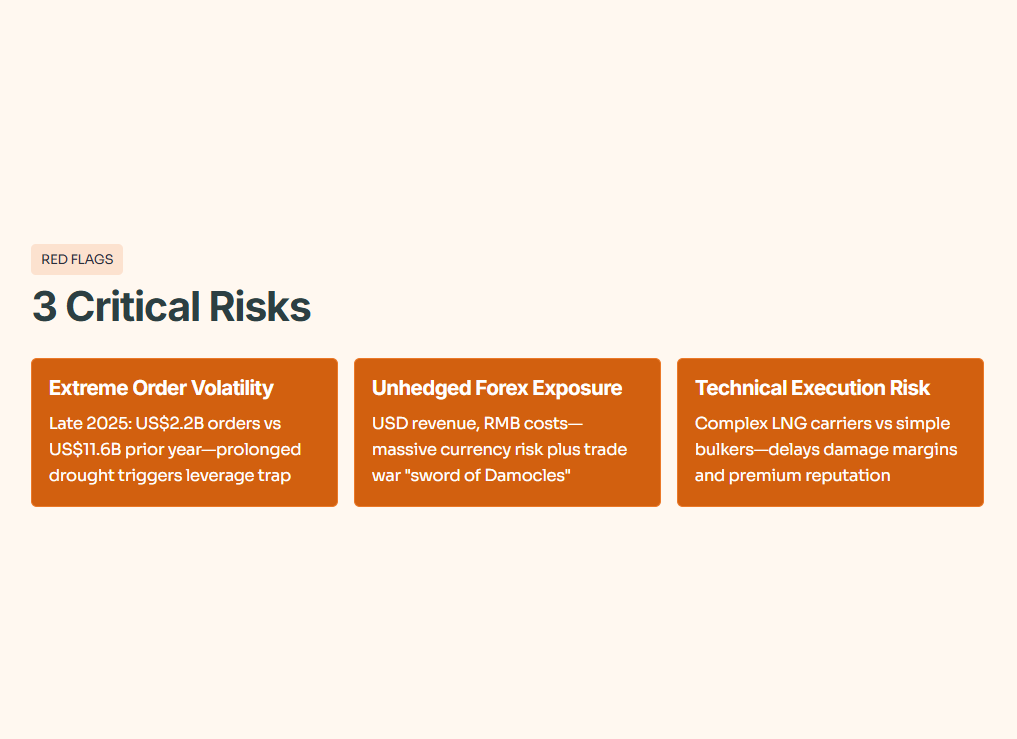

The “3 Red Flags”

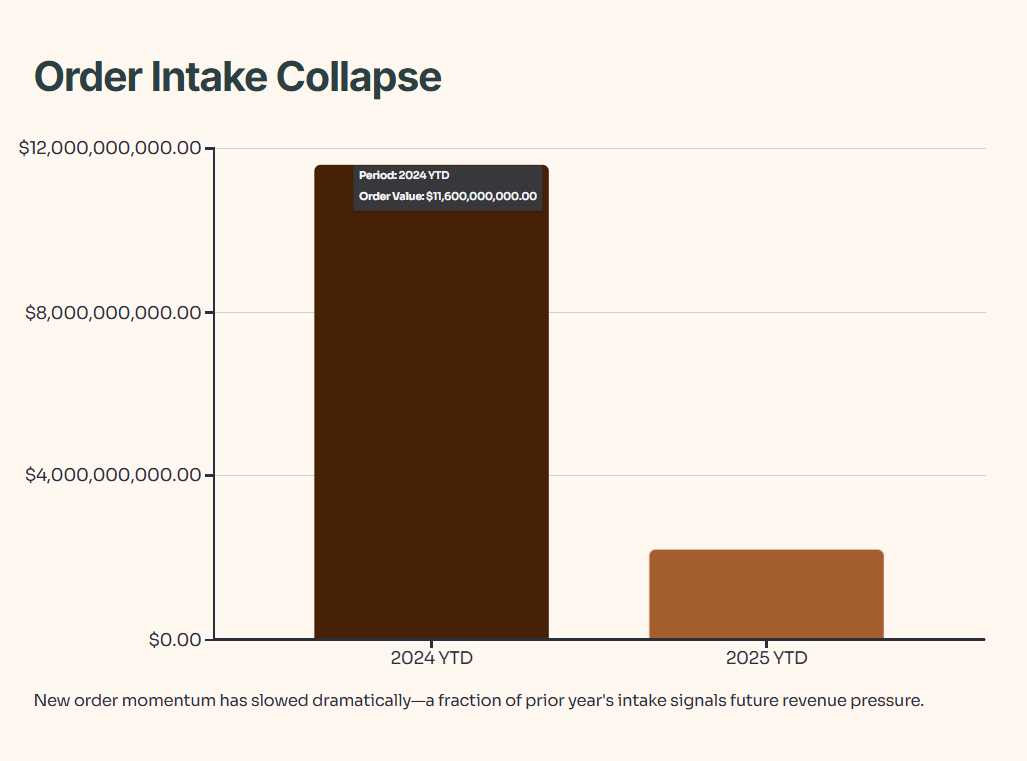

Extreme Order Intake Volatility: While the backlog is huge, new order momentum has slowed. In late 2025, year-to-date orders were just US$2.2 billion—a fraction of the US$11.6 billion secured in the same period the year prior. A prolonged drought in new orders will eventually trigger the operating leverage trap.

Unhedged Forex & Trade War Exposure: Revenue is primarily in USD while costs are in RMB, creating massive unhedged exposure to currency fluctuations. Furthermore, potential US policy actions or renewed trade wars targeted at Chinese-built vessels remain a persistent “sword of Damocles” for the share price.

Technical Execution Risk in High-Spec Vessels: Transitioning from simple bulkers to complex LNG carriers increases the risk of operational delays. Any technical failure or delivery delay in these first-in-class green vessels would not only impact margins but also damage YZJ’s newfound premium reputation.

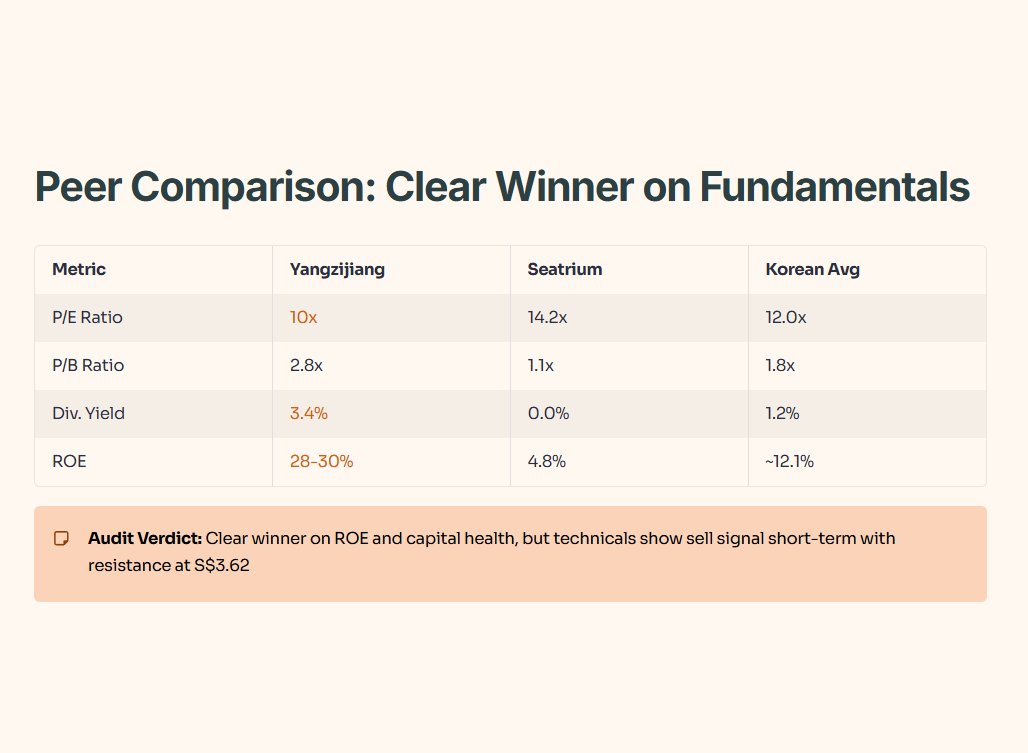

Peer Comparison Table

Audit Verdict: Yangzijiang is the clear Winner on fundamental efficiency (ROE) and capital health. However, technical indicators have recently issued a Sell signal for the short term, with resistance at S$3.62 as the stock tests historical peaks.

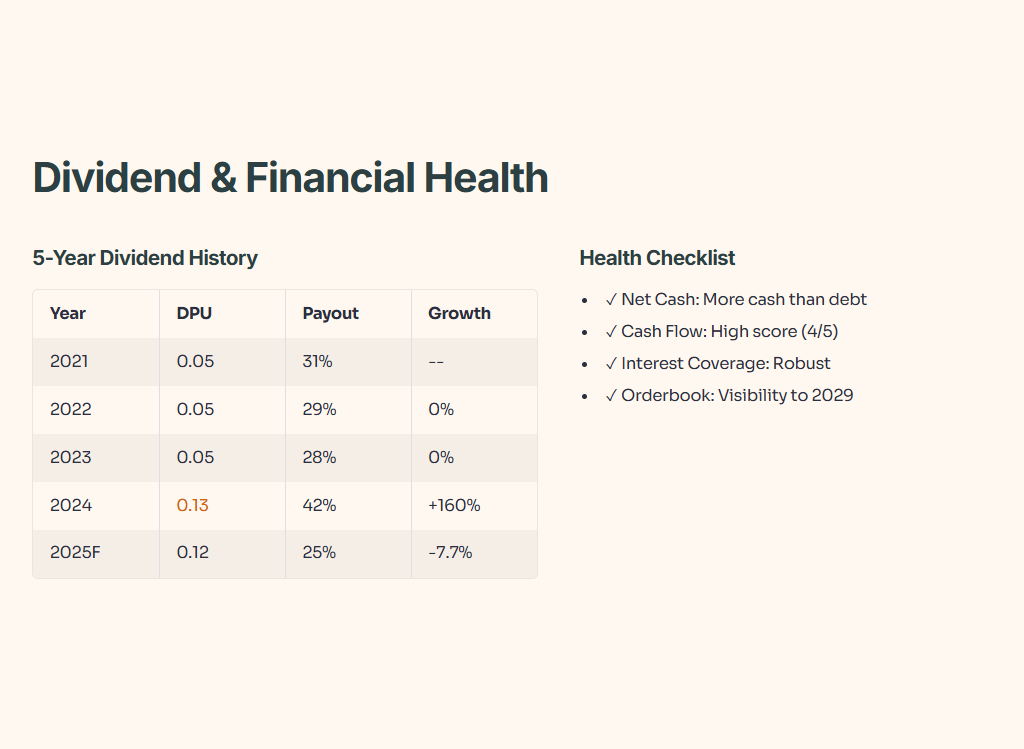

The Data Fortress: Dividend and Health Assessment

5-Year Dividend Ledger

Financial Health Checklist

Yangzijiang's balance sheet isn't just healthy—it's a fortress that laughs at recessions: more cash than debt means zero solvency stress even if orders vanish tomorrow; cash flow scores a rock-solid 4/5, proving operations print money without gimmicks; interest coverage stays robust enough to shrug off rate spikes; and that US$23.2 billion orderbook stretches visibility clean through 2029, turning revenue surprises into a non-event for patient investors who don't chase headlines.