You have 6 weeks left to lock in an instant 11.5% to 22% return—but leaving it in cash will destroy your wealth.

The clock is ticking. December 31, 2025 is the final deadline to contribute to your Supplementary Retirement Scheme (SRS) account and qualify for tax relief in Year of Assessment 2026.

The clock is ticking. December 31, 2025 is the final deadline to contribute to your Supplementary Retirement Scheme (SRS) account and qualify for tax relief in Year of Assessment 2026.

Miss this date, and you lose the single best risk-free return available in Singapore today.

Here’s the brutal truth most wealth managers won’t tell you: topping up your SRS isn’t just about tax savings. It’s about securing a guaranteed return that beats nearly every investment you can make today. And if you leave that money sitting in cash at 0.05% interest while inflation runs at 2.5%, you’re voluntarily destroying your purchasing power.

Let me show you exactly why this matters, what the numbers really mean, and how to deploy your SRS funds into three boring ETFs that will compound your retirement wealth while you sleep.

In This Article:

• The Instant Return Math: Your Guaranteed 11.5% to 22% Gain

• The Cash Trap: How You’re Guaranteeing a Loss

• The Safe-Growth Solution: 3 ETFs That Automate Your Retirement Wealth

• Why This 3-ETF Strategy Works for SRS

• Critical Considerations Before You Top Up

• The Brutal Reality: Most People Will Ignore ThisThe Instant Return Math: Your Guaranteed 11.5% to 22% Gain

Most Singaporeans think SRS is just a “tax savings scheme.” Wrong. It’s an instant return machine.

When you contribute to your SRS, you reduce your taxable income dollar-for-dollar. The tax bracket you’re in determines your instant return percentage. And unlike stocks, REITs, or bonds, this return is guaranteed the moment you transfer the money.

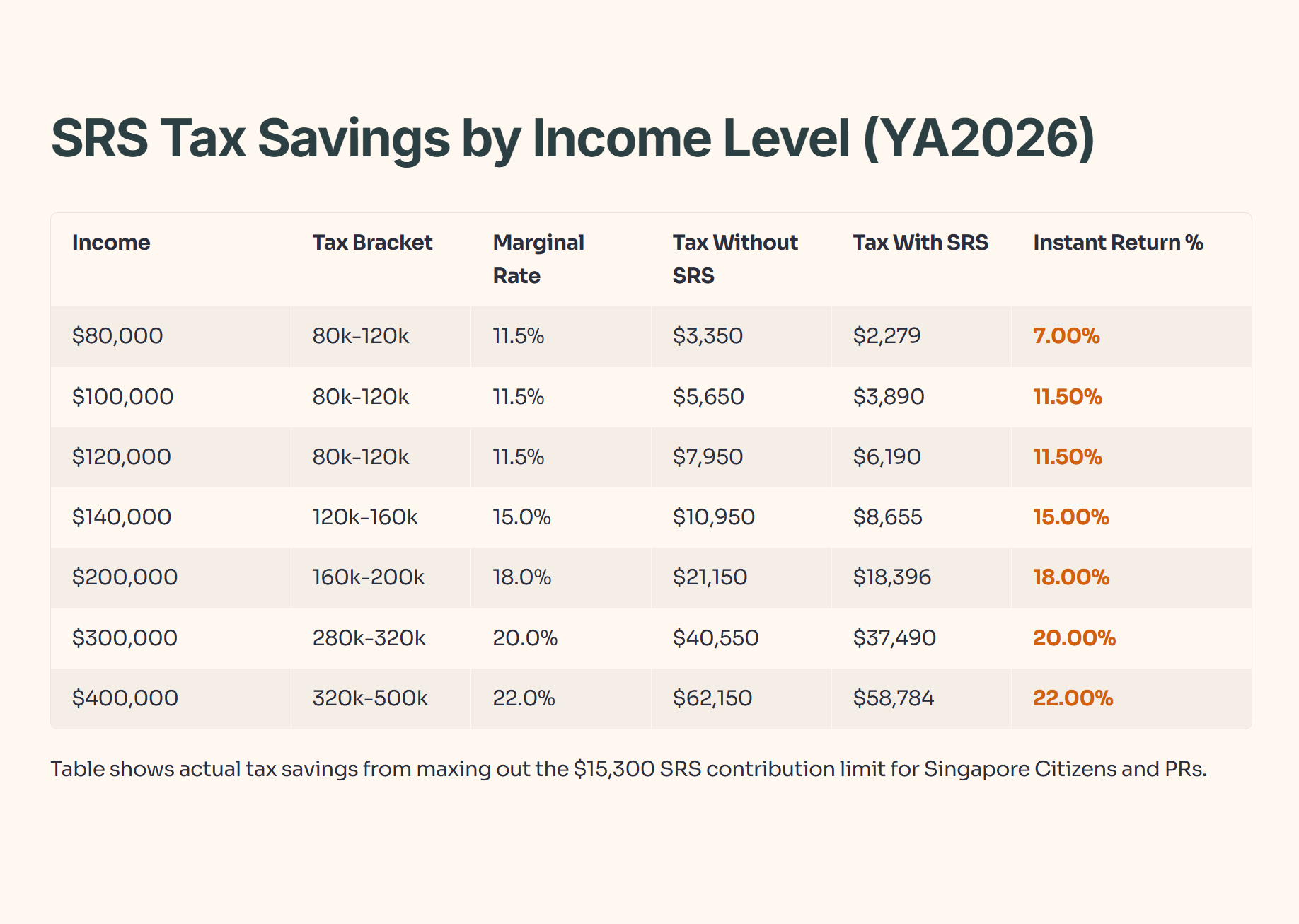

SRS Tax Savings by Income Level (YA2026)

Table shows actual tax savings from maxing out the $15,300 SRS contribution limit for Singapore Citizens and PRs. Foreigners can contribute up to $35,700.

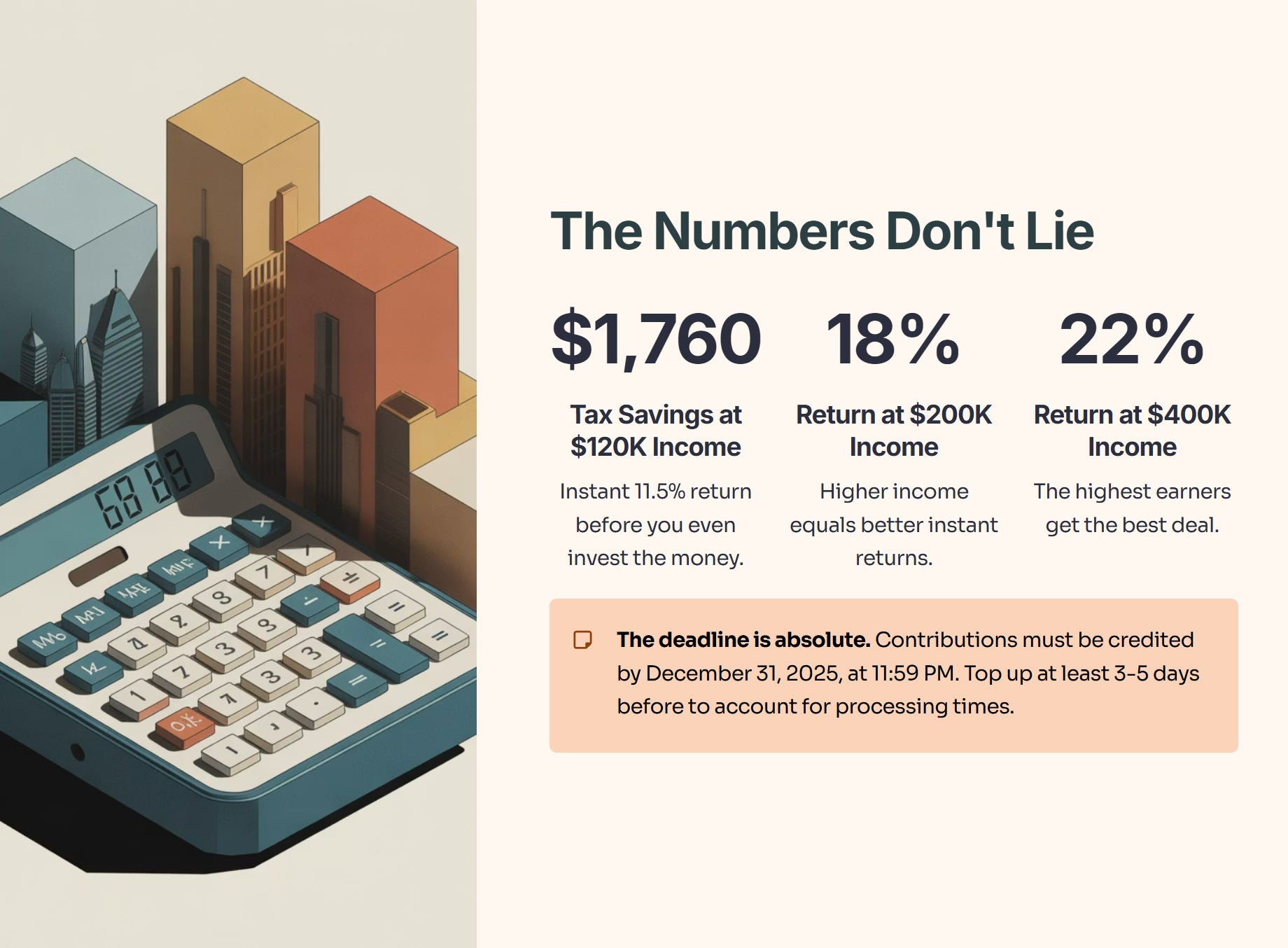

Let’s break this down. If you earn $120,000 and contribute the full $15,300, you save $1,759.50 in taxes immediately. That’s an instant 11.5% return before you even invest the money.

The higher your income, the better the deal gets. At $200,000 income, you’re looking at an 18% instant return. At $400,000, it jumps to 22%.

The deadline is absolute. Contributions must be credited to your SRS account by December 31, 2025, at 11:59 PM. Banks have different processing times, especially during the year-end rush. Don’t wait until December 30th—top up at least three to five days before the deadline.

The Cash Trap: How You’re Guaranteeing a Loss

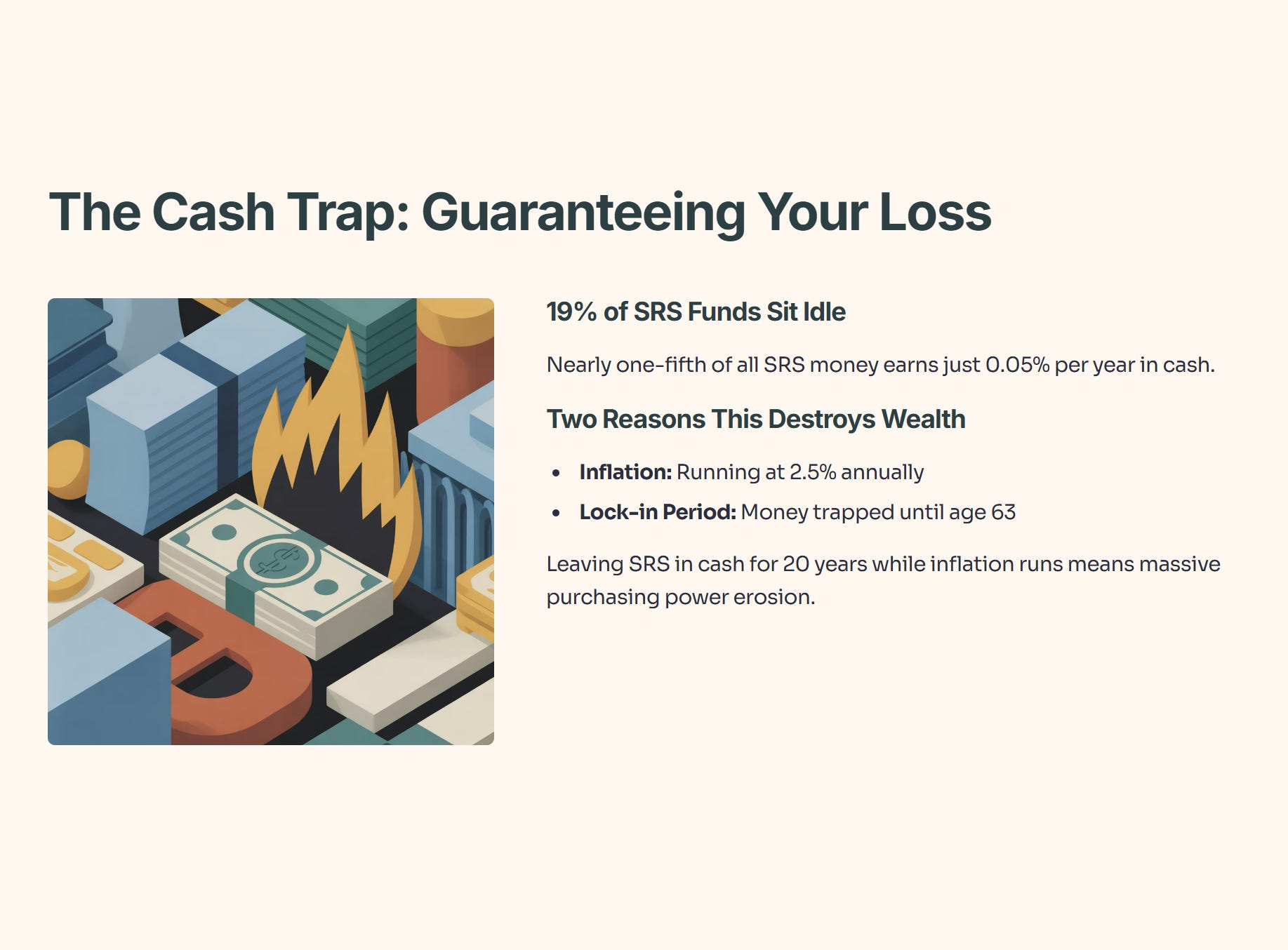

Here’s where most people destroy their SRS wealth. They top up to get the tax savings, then leave the money sitting in cash earning 0.05% per year. They think they’re being “safe.”

They’re actually lighting money on fire.

According to Ministry of Finance data, nearly 19% of all SRS funds sit idle in cash. Why is this so bad? Two reasons: inflation and lock-in period.

Your SRS money is locked until age 63. If you leave that money in cash for 20 years while inflation runs at a conservative 2.5%, the erosion of your wealth is staggering.

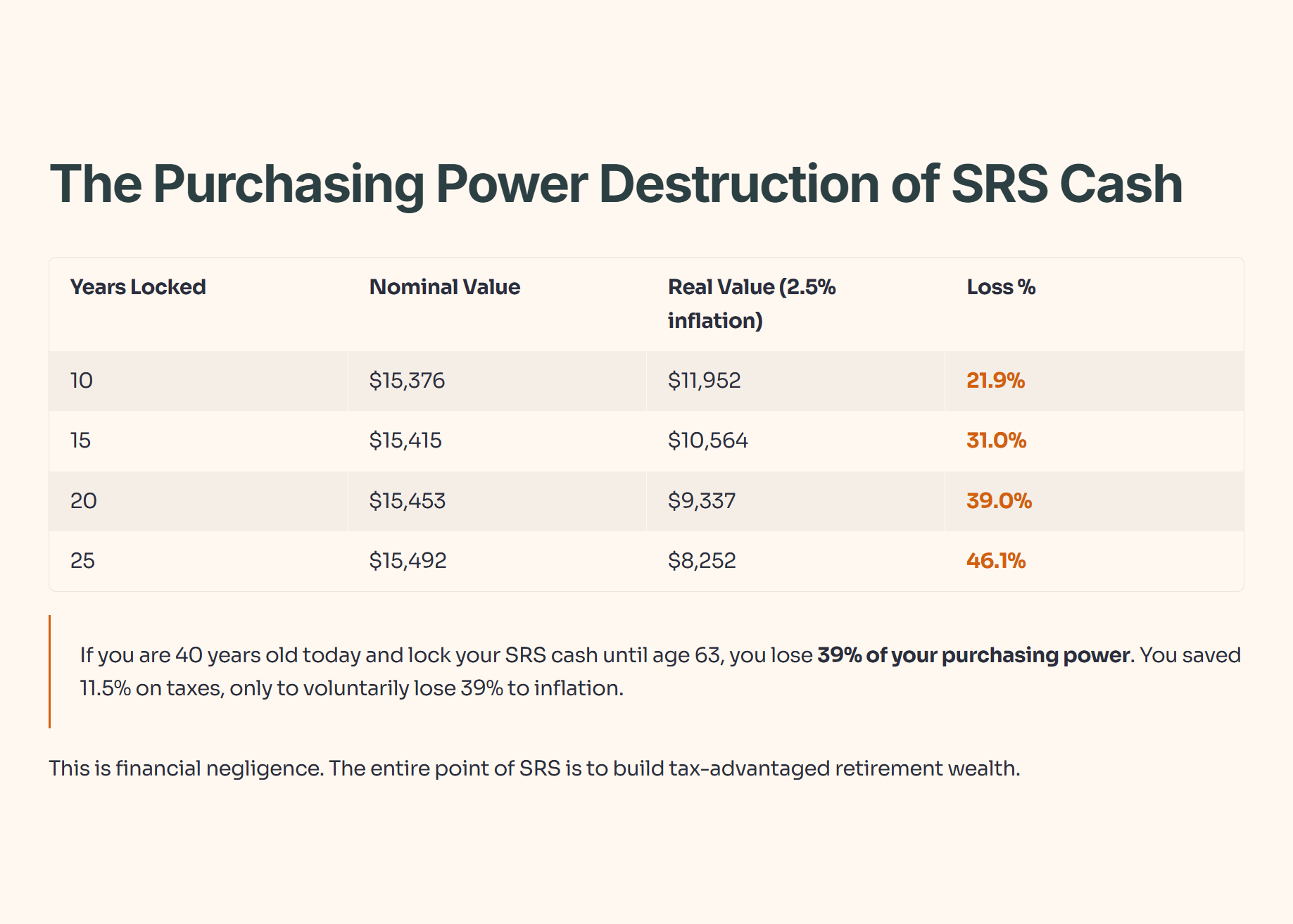

The Purchasing Power Destruction of SRS Cash

If you are 40 years old today and lock your SRS cash until age 63, you lose 39% of your purchasing power. You saved 11.5% on taxes, only to voluntarily lose 39% to inflation. This is financial negligence.

The entire point of SRS is to build tax-advantaged retirement wealth. If you’re not investing it, you’re wasting the advantage.

The Safe-Growth Solution: 3 ETFs That Automate Your Retirement Wealth

Most people leave their SRS in cash because they are paralyzed by choice.

I get it. That’s why I use a boring, automated “Safe-Growth” strategy. I buy just three ETFs that cover Singapore blue chips, REITs, and investment-grade bonds.

(Note: Below, I reveal the exact tickers I use. However, the magic is in the weighting—how much Bond vs. REIT vs. Equity you hold based on your age to minimize volatility while maximizing growth. I break down those exact allocation percentages and my annual rebalancing rules in my premium guide, “The SRS Safe-Growth Portfolio.” Upgrade to see the full system.)

Here is the framework (free version):

ETF #1: Stability – ABF Singapore Bond Index Fund (Ticker: A35)

This is the safest, most boring ETF you can own in Singapore. It tracks the iBoxx ABF Singapore Bond Index, holding AAA-rated Singapore government and government-linked bonds.

Role: This is your anchor. When markets panic, this ETF tends to hold steady or rise as investors flee to safety.

Stats: ~7.47% 3-year annualized return (as of Nov 2025). Expense ratio: 0.30%.