You Have S$200,000 Outside CPF. Now What?

The CPF decision worth roughly S$400,000 in lifetime income, and almost nobody explains it before it happens.

You Have S$200,000 Outside CPF. Now What?

If you are turning 55 this year, you are about to make a financial decision worth roughly S$400,000 in lifetime income, whether you realise it or not. Almost nobody explains this decision before it happens, and once it is made, it cannot be undone. This piece walks through exactly how the numbers work, using a worked example so you can apply the same forensic process to your own Retirement Account.

I am Iggy, ranked eighth among Singapore retail investors on Tiger Brokers, and I built this framework for two kinds of readers. One of you has been tracking CPF policy changes closely and knows the broad strokes of what is coming. The other is hearing about the Enhanced Retirement Sum for the first time and just wants to know what it means for your own account. Both of you are about to see the same numbers, applied to the same decision, because the math does not change depending on how much homework you have already done.

Before we get into the numbers, I want to say who I am doing this for. Not the trader with a twenty-year runway. Not the growth chaser hunting the next ten-bagger. I am doing this for the retiring and retired Singaporean who needs their capital to work reliably, not spectacularly.

In This Article:

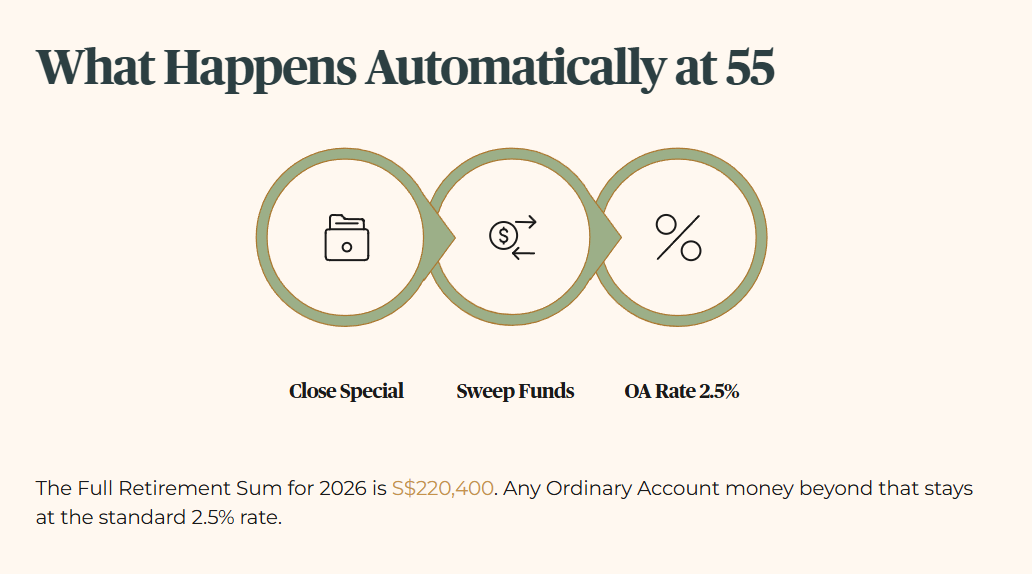

What Happens Automatically at 55

The Forensic Math Behind the Number

What Governs the Capital You Choose to Keep Liquid

Why Entry Cost Matters to a Forensic Investor

Tan’s Decision: Two Scenarios

The SAN Score Reality Check

Strategic Considerations

What Happens Automatically at 55

Here is the decision in plain terms. At age 55, your CPF Special Account closes permanently, a change that took effect from 19 January 2025. Whatever was in your Special Account, plus part of your Ordinary Account, gets swept into a new account called the Retirement Account, up to a ceiling called the Full Retirement Sum, or FRS. For 2026, the FRS is S$220,400. Any Ordinary Account money beyond that stays in your Ordinary Account, earning the standard 2.5% rate rather than the higher 4.0% rate your Special Account used to earn.

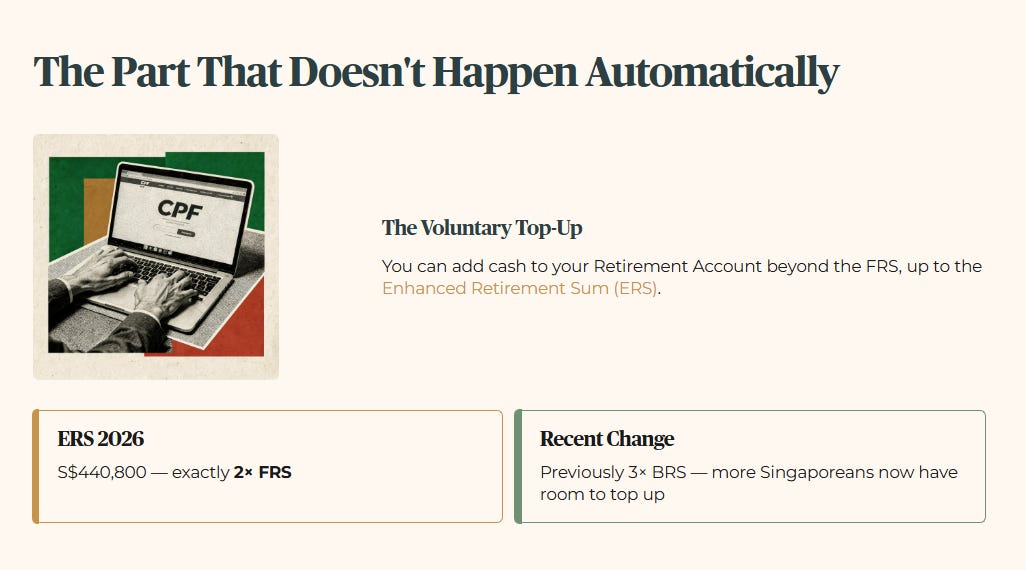

That part happens automatically. The part that does not happen automatically, and the part this article is really about, is whether you choose to add more cash to your Retirement Account voluntarily, on top of the FRS, up to a higher ceiling called the Enhanced Retirement Sum, or ERS. For 2026, the ERS is S$440,800, which works out to exactly twice the FRS. This is itself a recent change. Until the start of 2026, the ERS ceiling was calculated differently, at three times a smaller reference figure called the Basic Retirement Sum. The shift to a flat two times FRS means more Singaporeans now have meaningful room to top up than before, if they have the cash sitting outside CPF to do it.

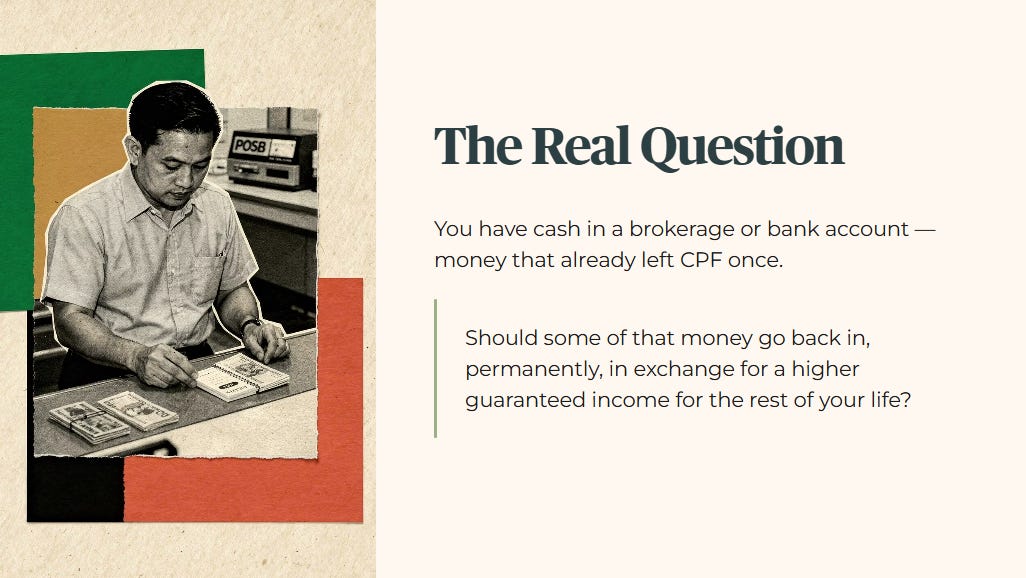

This is the decision nobody walks you through. You have cash sitting in a brokerage account or a bank account, money that already left the CPF system once. The question in front of you is whether some of that money should go back in, permanently, in exchange for a higher guaranteed income for the rest of your life.

The Forensic Math Behind the Number

Here is why this decision is worth roughly S$400,000 over a typical retirement, and where that figure actually comes from, because I am not going to ask you to trust a headline number without showing the working.

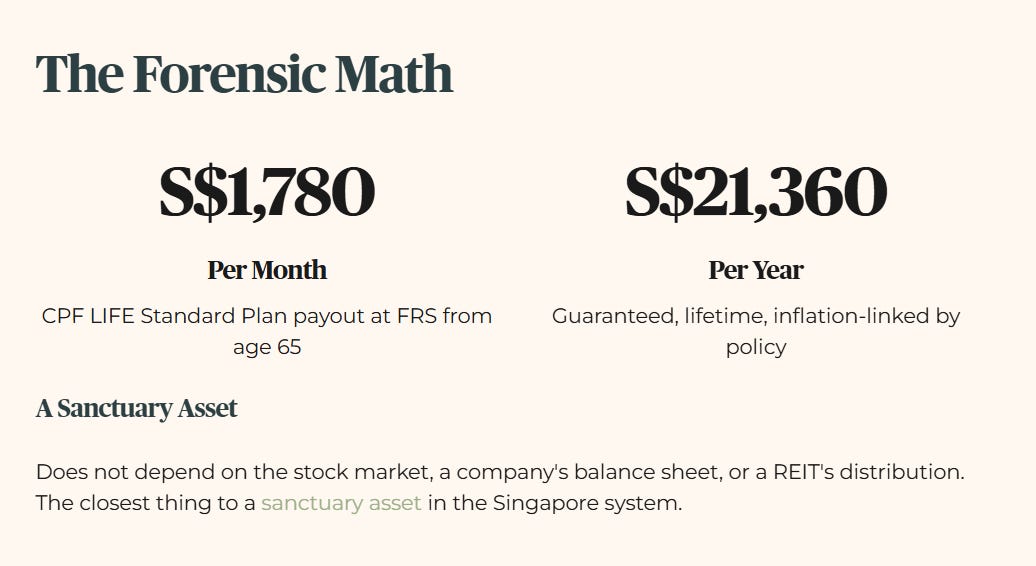

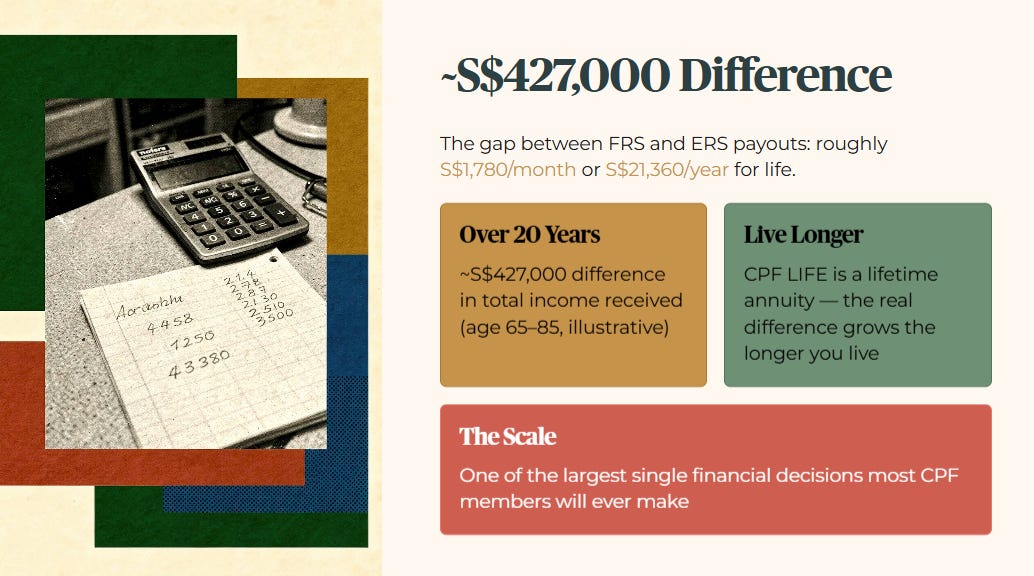

CPF publishes an estimate that a member with a Retirement Account at the FRS level, taking CPF LIFE Standard Plan payouts from age 65, can expect approximately S$1,780 per month for life. That works out to S$21,360 a year. This is a guaranteed, lifetime, inflation linked by policy income stream. It does not depend on the stock market, on a company’s balance sheet, or on whether a REIT’s distribution per unit holds up. It is the closest thing to a sanctuary asset that exists in the Singapore system.

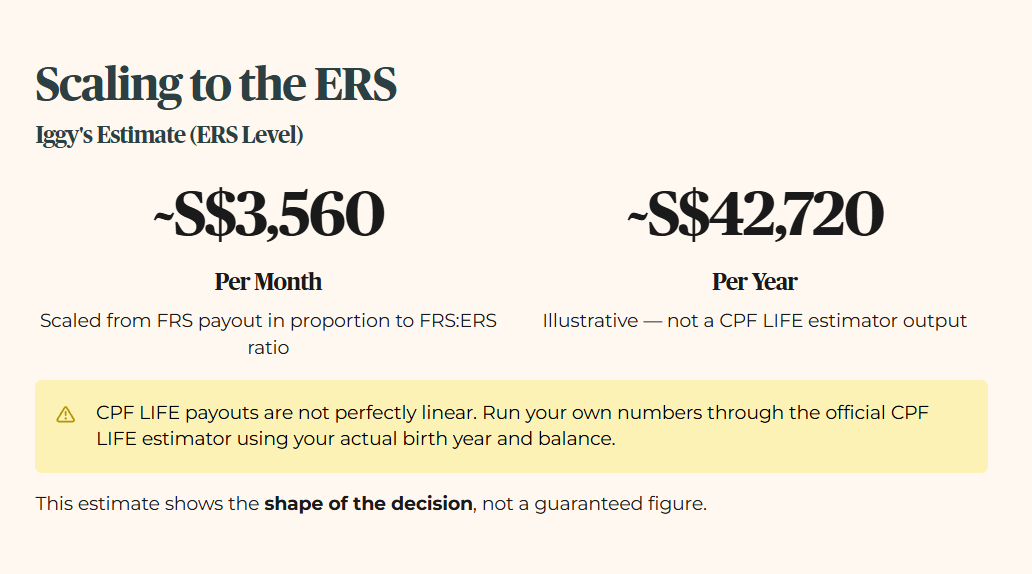

Now here is where it gets interesting. Because the ERS is exactly twice the FRS, and CPF LIFE payouts scale roughly in proportion to your Retirement Account balance at the point your payouts start, a Retirement Account funded to the full ERS level would generate a monthly payout in the region of S$3,560, or roughly S$42,720 a year. I want to be precise about what this figure is and is not. It is Iggy’s estimate, derived by scaling the verified FRS payout figure in proportion to the FRS to ERS ratio. It is not a CPF LIFE estimator output for the ERS level specifically, and CPF LIFE payouts are not perfectly linear across the entire range. If you are seriously considering a top-up, run your own numbers through the official CPF LIFE estimator using your actual birth year and Retirement Account balance. The estimate here is for illustration, to show the shape of the decision, not to promise you an exact figure.

With that caveat in place, the gap between the FRS payout and the ERS payout is roughly S$1,780 a month, or about S$21,360 a year, for the rest of your life. Run that gap over a twenty-year payout horizon, from age 65 to 85, purely as an illustrative comparison rather than a guarantee, and you get a difference in the region of S$427,000 in total income received. CPF LIFE is a lifetime annuity, so if you live longer than twenty years past 65, the real difference is larger. If you live a shorter time, it is smaller. Either way, the order of magnitude is the same. This is not a rounding error. It is one of the largest single financial decisions most CPF members will ever make, and it is made with a few clicks on the CPF website, often without anyone explaining what just happened.

🦎 Iggy’s Insight Block 1

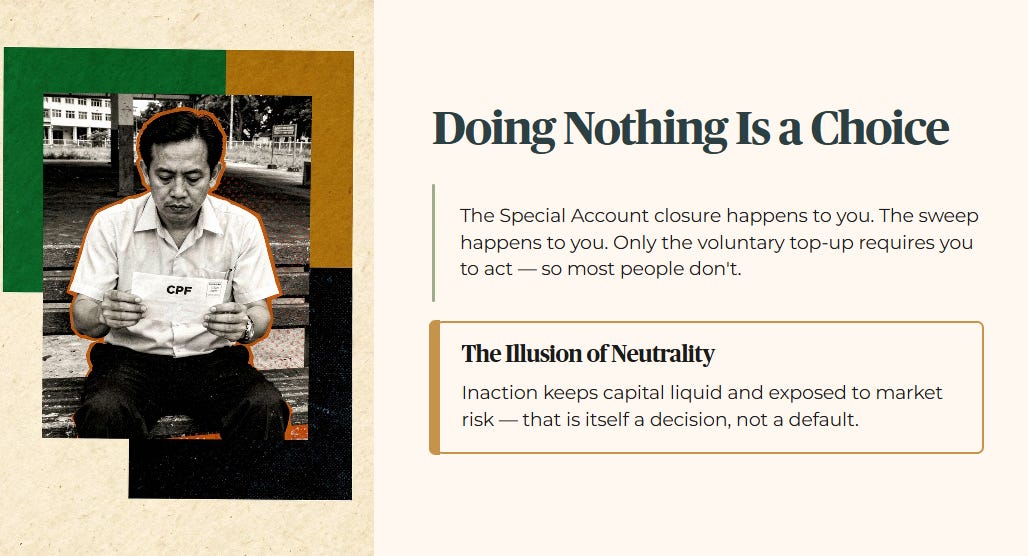

The reason this decision goes unexamined is that it does not feel like a decision. The Special Account closure happens to you automatically at 55. The sweep into the Retirement Account happens automatically. The only part that requires you to act is the voluntary top-up beyond FRS, and because it requires action, most people simply do nothing, and doing nothing feels neutral. It is not neutral. Doing nothing is itself a choice, the choice to keep that capital liquid and exposed to market risk rather than converting it into guaranteed lifetime income. Neither choice is wrong. But only one of them is being made consciously by most retirees, and it is usually not the voluntary one.

What Governs the Capital You Choose to Keep Liquid

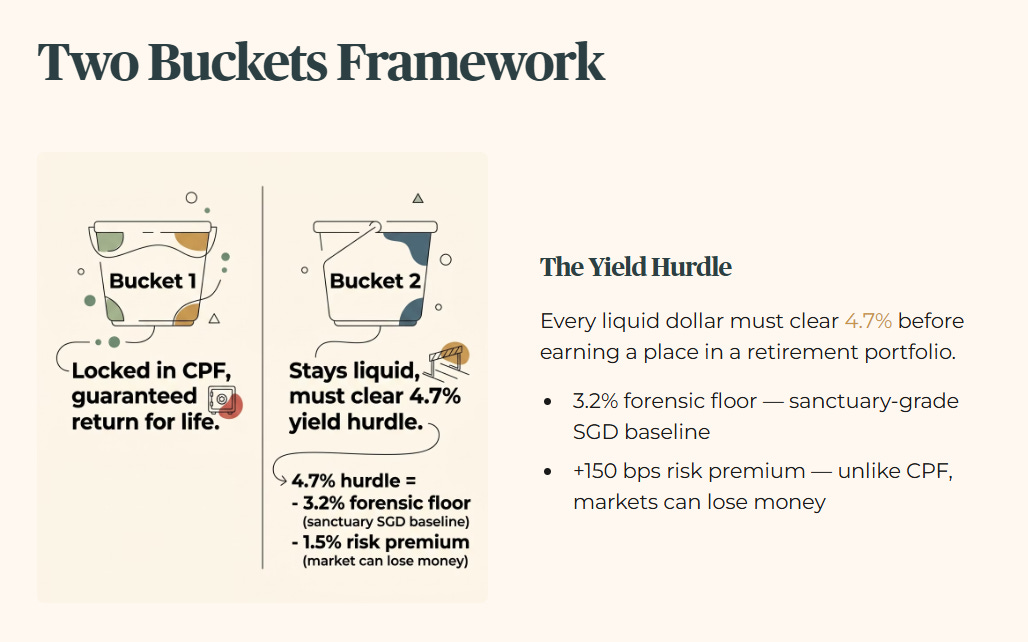

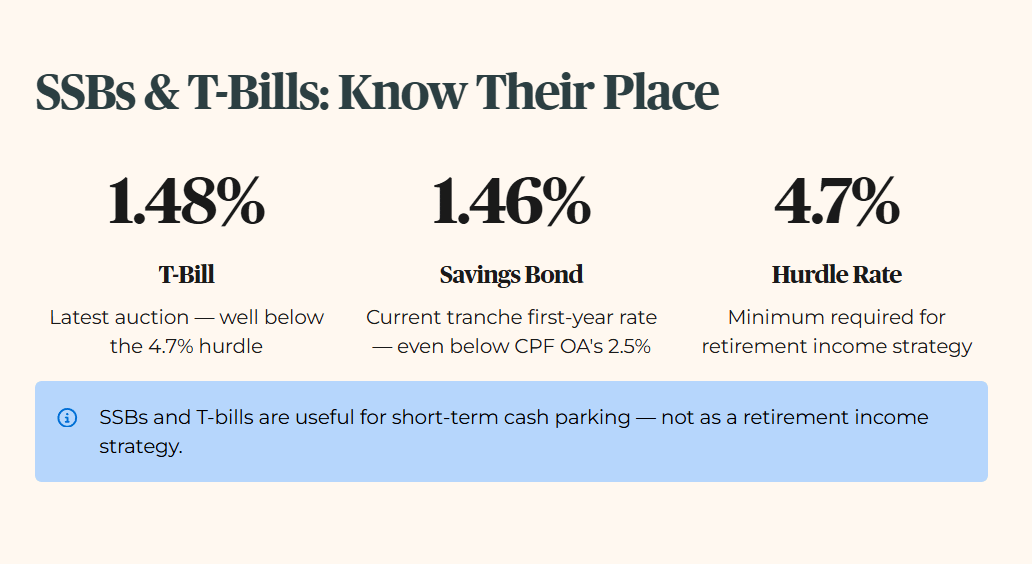

Whatever portion of your outside capital you do not put into your Retirement Account stays exposed to the open market, and that is where my standard forensic framework takes over. I think of it as two buckets. One bucket is locked away in exchange for a guaranteed return for life. The other bucket stays liquid, and every dollar in that bucket has to clear my yield hurdle, the minimum return I require before any income-generating asset earns a place in a retirement portfolio, which is 4.7%. This hurdle is built from my forensic floor of 3.2%, which is my personal baseline for what a sanctuary-grade SGD asset should yield, plus a 150 basis point risk premium for the fact that, unlike CPF, the open market can lose you money.

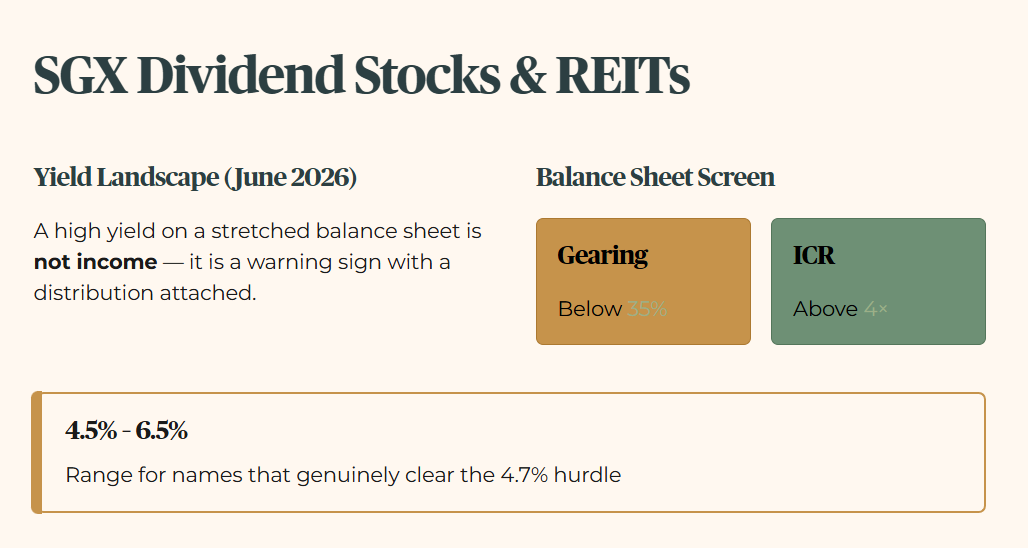

For Singapore dollar dividend stocks and REITs (real estate investment trusts), the yield landscape in June 2026 ranges roughly from 4.5% to 6.5% for names that genuinely clear my hurdle, with some higher-yielding REITs extending further, though a higher yield on its own is never the full story. Before any stock or REIT earns a place in this bucket, it also has to pass a balance sheet screen. Gearing, which is the proportion of a company’s or trust’s assets funded by debt, needs to sit below 35%. Interest coverage ratio, or ICR, which measures how many times over a company’s earnings can cover its interest payments, needs to sit above 4 times. A high yield sitting on top of a stretched balance sheet is not income, it is a warning sign with a distribution attached.

Singapore Savings Bonds and T-bills sit below this hurdle by design. The most recent T-bill auction cleared at 1.48%, and the current Savings Bond tranche offers a 1.46% first-year rate. Both are well below the 4.7% hurdle and even below the 2.5% your CPF Ordinary Account already pays. They are useful as short-term cash parking, not as a retirement income strategy. If part of your liquid bucket needs to stay genuinely safe and accessible, this is where it goes, with eyes open about what it is for.

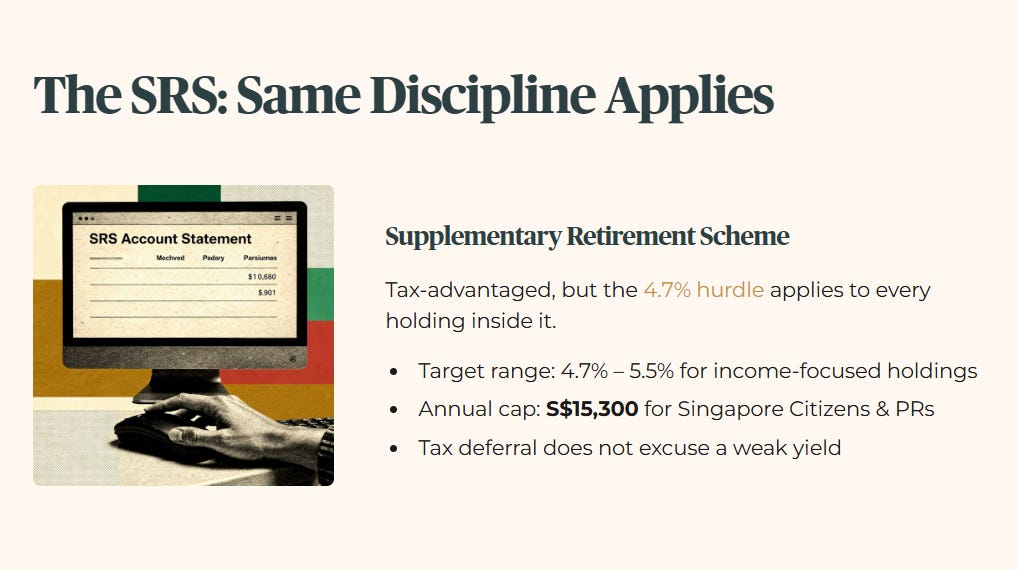

The Supplementary Retirement Scheme, or SRS, is a separate tax-advantaged account where the same 4.7% discipline applies to whatever you invest inside it, typically in a range of 4.7% to 5.5% for income-focused holdings under this framework. The annual contribution cap for Singapore Citizens and Permanent Residents is S$15,300. Tax deferral inside SRS does not excuse a weak yield outside it, the same forensic standard applies regardless of which account the money sits in.

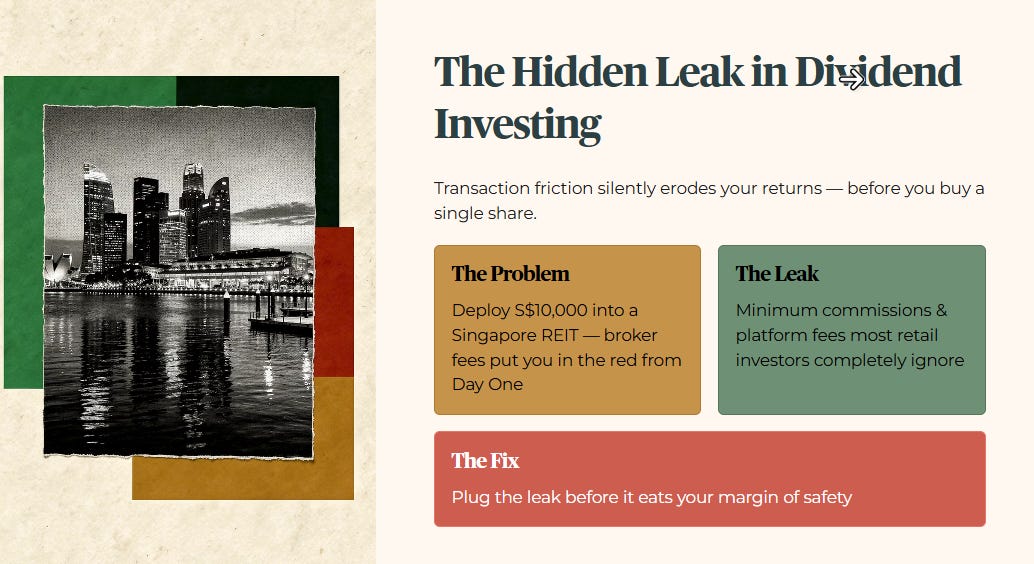

All of this assumes you can actually deploy capital into the Four Lanes without losing ground before you start. There is a cost most forensic discussions skip entirely: what it costs you, in fees and friction, just to place the trade. If you are putting ten thousand Singapore dollars into a Singapore REIT and your broker eats a meaningful chunk of that in minimum commissions, you have started the position in the red before a single distribution has landed in your account. This is worth a short detour, because it directly affects the real yield you receive from anything in Lane 1 or Lane 3.

Why Entry Cost Matters to a Forensic Investor

In the world of dividend investing, we spend a lot of time talking about the yield spread, the difference between what a stock pays you and the risk-free rate. But there is a hidden leak that most retail investors completely ignore: transaction friction. If you are deploying ten thousand Singapore dollars into a Singapore REIT, and your broker eats a chunk of that in minimum commissions or platform fees, you are starting your investment in the red before you have even bought a single share.

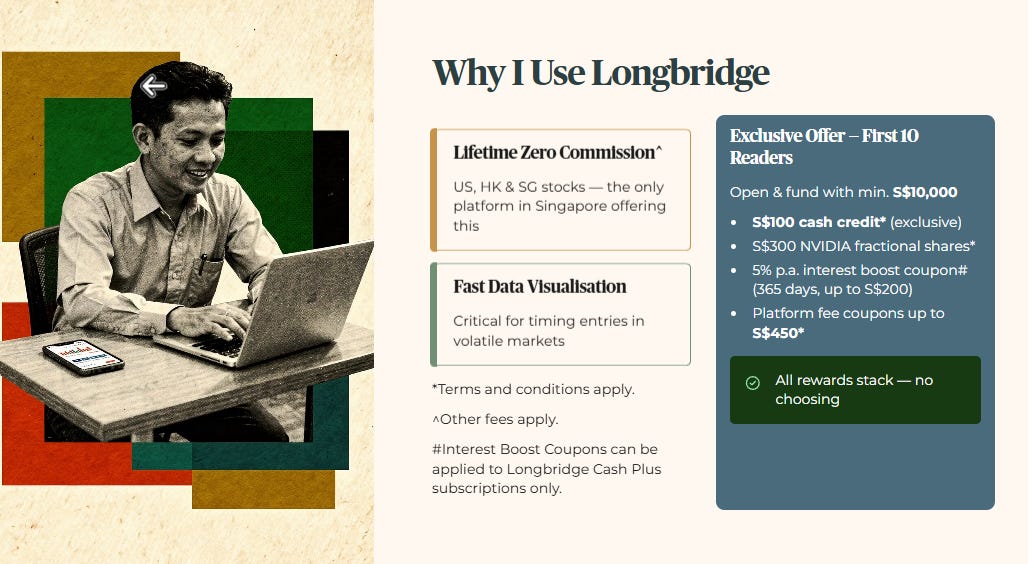

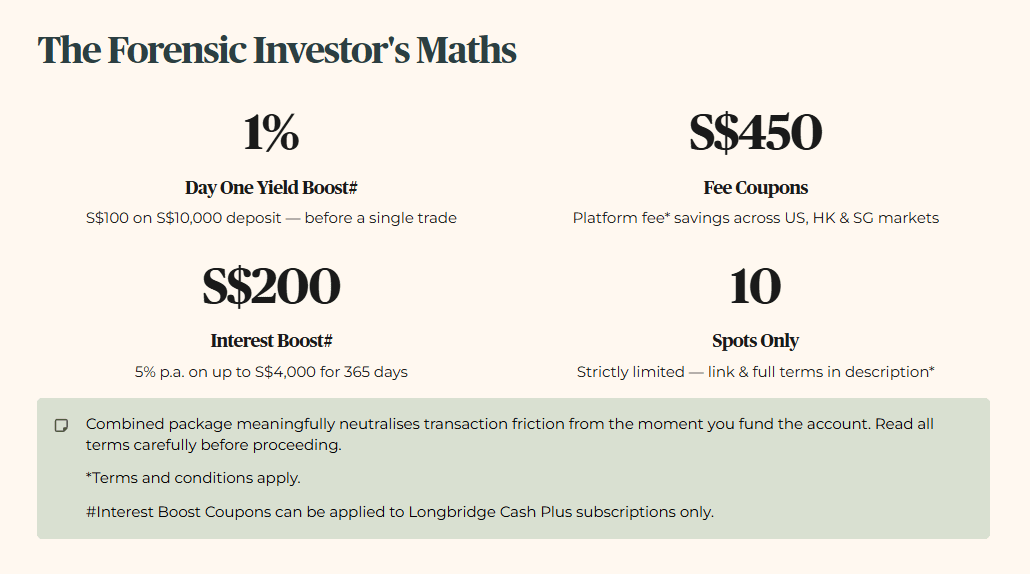

Data is only useful if you have the tools to act on it without getting eaten alive by those fees. That is why I use Longbridge. They are currently the only platform in Singapore offering lifetime zero commission^ for US, Hong Kong, and Singapore stocks. Their data visualisation is also some of the fastest I have used, which is critical when you are timing an entry in a volatile market.

To help you plug that leak, I have partnered with Longbridge on an exclusive arrangement for my readers. For the first ten readers who open and fund an account with a minimum of ten thousand Singapore dollars, Longbridge is offering a direct one hundred Singapore dollar* cash credit on top of their already generous June welcome rewards.

Here is what the full package looks like if you deposit ten thousand dollars, hold it for ninety days, and complete five buy trades. You receive the exclusive one hundred dollar cash credit. You receive three hundred Singapore dollars worth of NVIDIA fractional shares. You receive a five percent per annum interest boost coupon valid for three hundred and sixty-five days on deposits up to four thousand dollars, worth up to two hundred Singapore dollars over the year. And you receive platform fee coupons worth up to four hundred and fifty Singapore dollars across US, Hong Kong, and Singapore markets. All of these stack together. You do not have to choose between them.

Why does this math matter to a forensic investor? Because one hundred dollars on a ten thousand dollar deposit is an immediate one percent Day One Yield Boost before you have executed a single trade. Combined with the interest boost coupon# and platform fee savings, the total welcome package meaningfully neutralises transaction friction and protects your margin of safety from the moment you fund the account.

This is strictly limited to the first ten spots. The link and full terms are below, so read those carefully before you proceed. But for a forensic investor who cares about entry cost and yield from day one, this is worth five minutes of your time.

Tan’s Decision: Two Scenarios

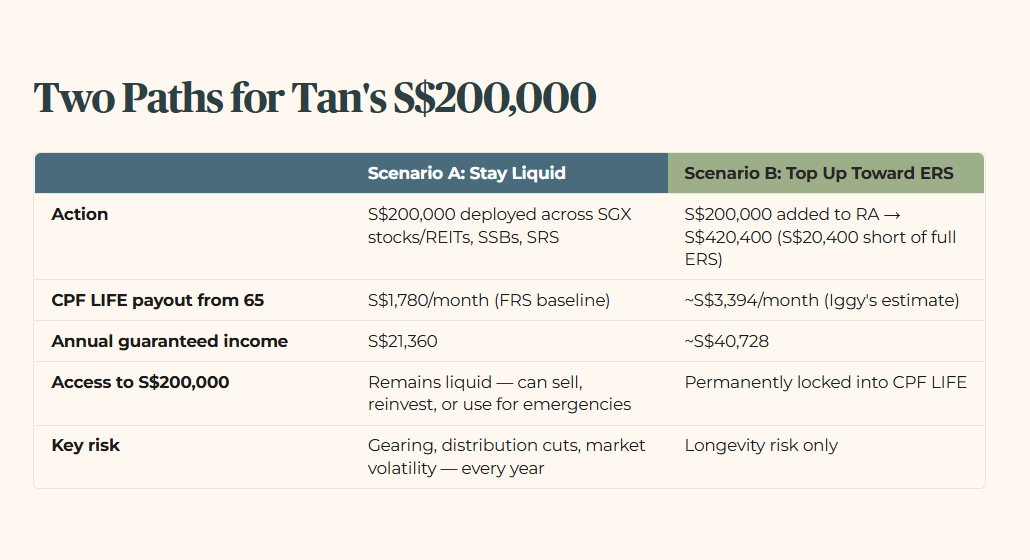

Let me make this concrete with a heartland archetype. Tan is 55, lives in a four-room HDB flat in Bedok, and has just had his CPF Special Account closed and swept into his Retirement Account at the FRS of S$220,400. Outside CPF, he has S$200,000 in liquid capital and S$15,300 in his SRS account. The gap between his Retirement Account at FRS and the ERS ceiling is S$220,400, almost exactly the amount of his liquid capital. He is, in practice, one decision away from a meaningful top-up.

Table 1: Two Paths for Tan’s S$200,000

Neither column is the right answer for everyone, and I am not telling you which one to pick. That decision depends on things this framework cannot see: your health, your family’s longevity, whether you have other liquid assets for emergencies, and how much you value certainty over flexibility. What the framework can do is make sure you are choosing with the real numbers in front of you, rather than defaulting into Scenario A by inaction without realising that is what you have done.

🦎 Iggy’s Insight Block 2

Most retirees who end up in Scenario A did not choose it. They simply did not act on the top-up option before the deadline that applies to their cohort, and the default became permanent by omission. The forensic tragedy here is not that Scenario A is wrong, plenty of retirees with strong health, other liquid reserves, and the discipline to apply a 4.7% hurdle consistently will do perfectly well in Scenario A. The tragedy is when someone who would have genuinely preferred the certainty of Scenario B never knew the door was open, and finds out only when a friend mentions it years later, by which point the window for that cohort’s top-up calculation has shifted. This is not a product to be sold to you. It is a feature of the system that only works if you know it exists.

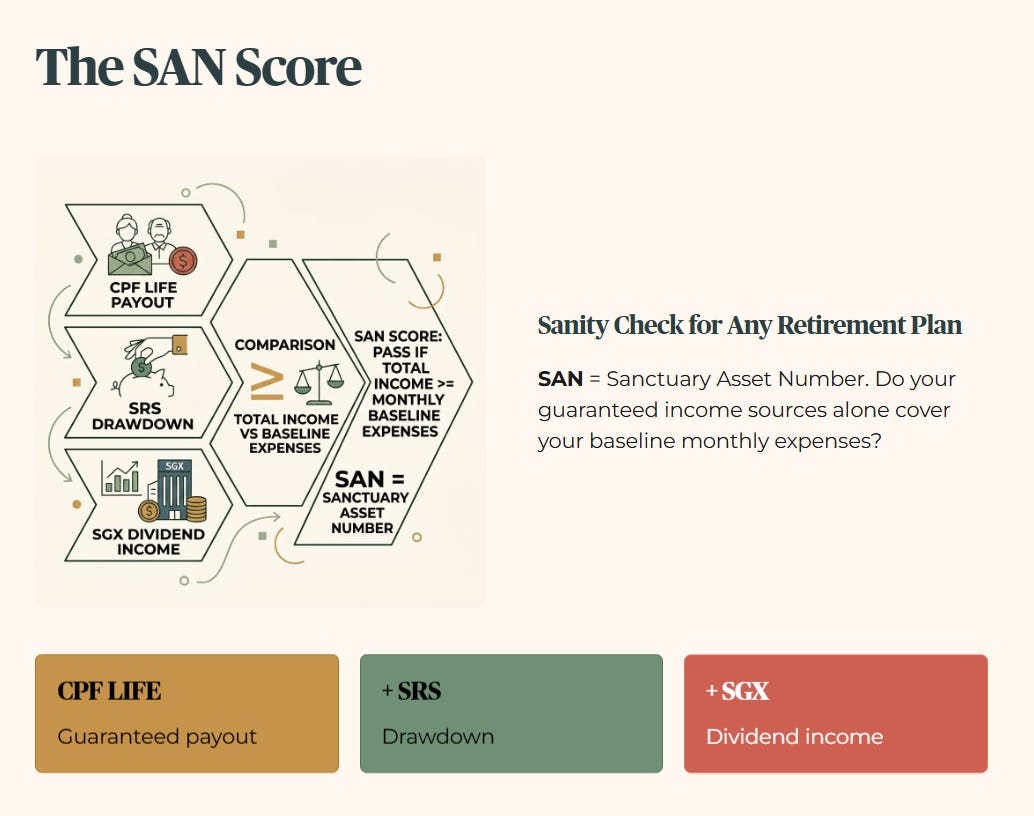

The SAN Score Reality Check

I use something I call the SAN Score, shorthand for whether your guaranteed income sources alone cover your baseline monthly expenses, as a sanity check for any retirement plan. The formula is simple: CPF LIFE payout, plus SRS drawdown, plus SGX dividend income, compared against your monthly baseline expenses.

Table 2: SAN Score Under Each Scenario (illustrative monthly figures)

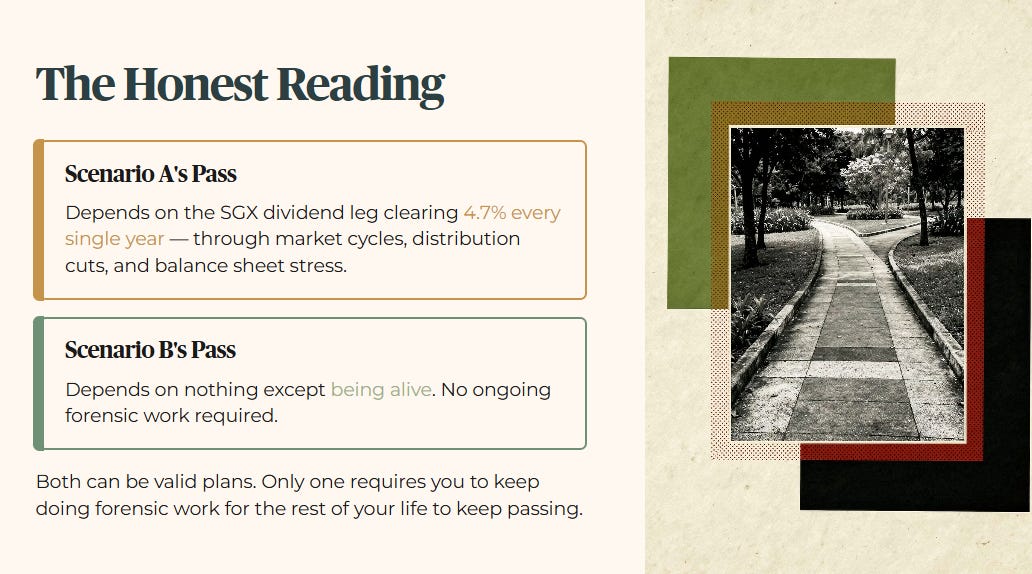

The honest reading of this table is not that Scenario B “wins” on the SAN Score. It is that Scenario A’s pass depends on the SGX dividend leg actually clearing 4.7% and continuing to clear it every single year, through market cycles, distribution cuts, and balance sheet stress. Scenario B’s pass does not depend on anything except being alive. Both can be valid plans. Only one of them requires you to keep doing forensic work for the rest of your life to keep passing.

Strategic Considerations

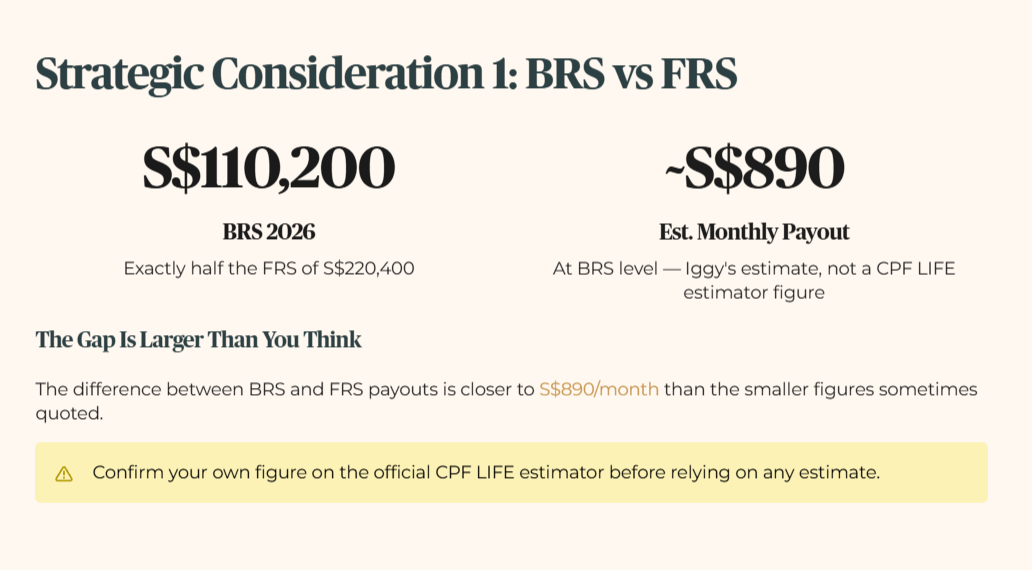

Strategic Consideration 1: The gap between the Basic Retirement Sum and the Full Retirement Sum matters even if you are not considering an ERS top-up. The 2026 BRS is S$110,200, exactly half the FRS of S$220,400. If CPF LIFE payouts scale roughly in proportion to your Retirement Account balance, the same way the FRS to ERS comparison works above, a Retirement Account at BRS would generate roughly half the FRS payout, in the region of S$890 a month, compared to S$1,780 at FRS. This is Iggy’s estimate based on the FRS to BRS ratio, not a verified CPF LIFE estimator figure for BRS specifically. If you are deciding between BRS and FRS, the gap is closer to S$890 a month than the smaller figures sometimes quoted, and you should confirm your own figure on the official CPF LIFE estimator before relying on it.

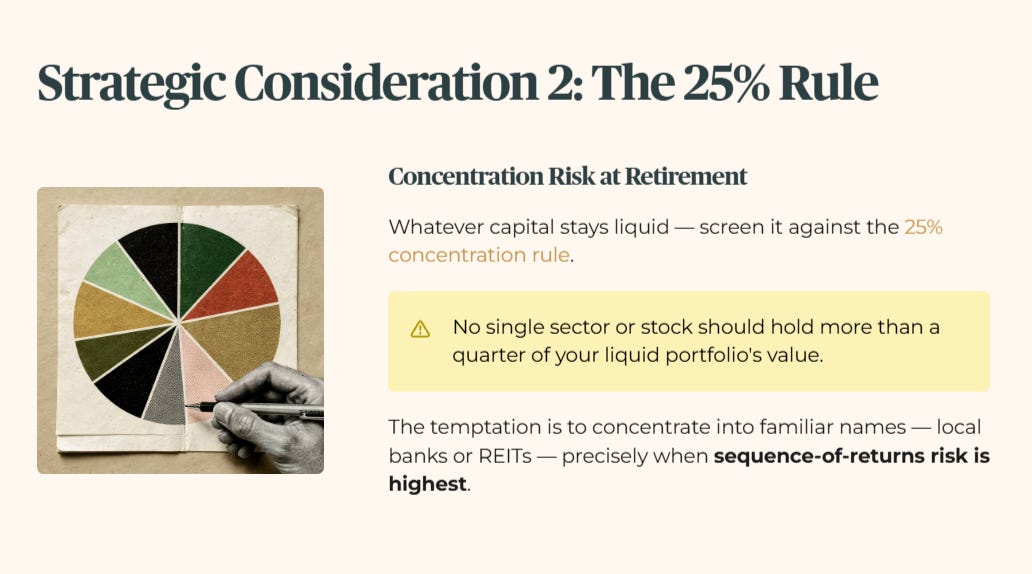

Strategic Consideration 2: Whatever capital you decide to keep liquid, whether that is the full S$200,000 in Scenario A or the remaining S$20,400 gap in Scenario B, screen it against the 25% concentration rule. No single sector or stock should hold more than a quarter of that liquid portfolio’s value. The temptation at this life stage is to concentrate into familiar names, usually local banks or REITs, precisely when sequence-of-returns risk is highest.

Strategic Consideration 3: If you are seriously evaluating a top-up, the deadline that applies to your specific birth cohort and the exact mechanics of the top-up process are CPF Board matters, not market data, and they change. Confirm the current process and any cohort-specific windows directly with CPF Board before acting. This framework tells you how to think about the decision. It does not replace verifying the mechanics with the source.

You now have the same forensic process I use to look at this decision. The Special Account closure already happened to you automatically. The question this piece leaves you with is simple: are you going to let the rest of the decision happen to you too, or are you going to make it?

Iggy’s Forensic Disclaimer

This video is a paid partnership with Longbridge Singapore. It is intended for general awareness and does not constitute investment advice or a recommendation to buy, sell, or otherwise engage with any investment products or financial services.

The presenter is not a licensed financial adviser and is not offering financial advice. All views expressed are solely those of the presenter and do not necessarily reflect the views of Longbridge Singapore.

All investments carry risks, may not be suitable for everyone, and you may lose your investment principal. Past performance is not indicative of future results. You should seek independent financial advice if you are unsure about any investment decisions. This advertisement has not been reviewed by the Monetary Authority of Singapore.