Your Dividend Has an Expiry Date: The Truth Behind SingTel's Record Payout and the Big Three's S$8.5 Billion Return

Strip out the asset sales and the buyback programmes, and three of Singapore's most trusted blue chips yield less than CPF

Strip out the asset sales and the buyback programmes, and three of Singapore's most trusted blue chips yield less than CPF

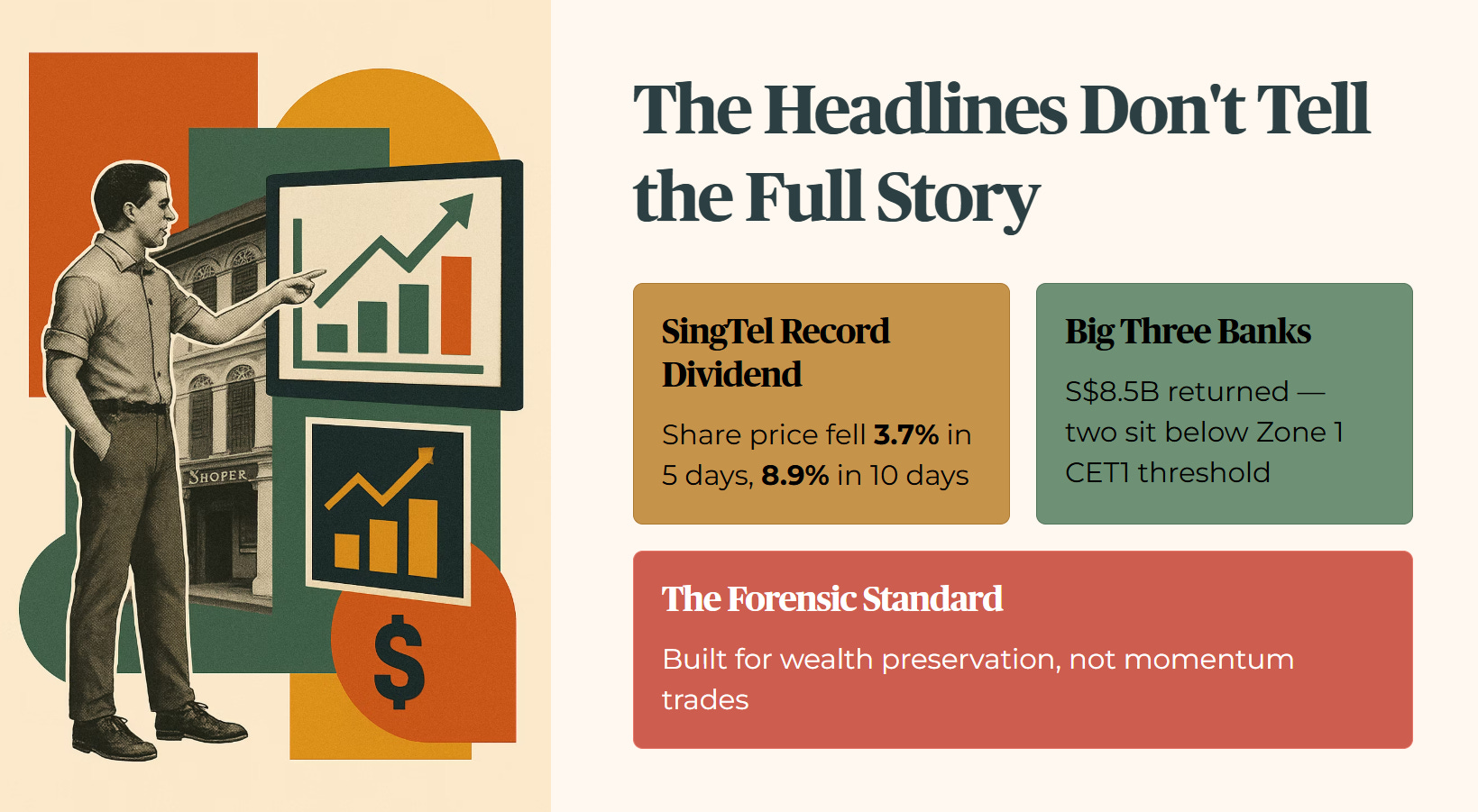

SingTel just paid out a record dividend. Its share price fell 3.7% over five days and 8.9% over ten days. The Big Three banks are returning S$8.5 billion to shareholders. Two of them are sitting below their Zone 1 CET1 threshold.

When blue chips restructure, the numbers rarely tell the story the press release wants you to read.

If you are chasing growth and momentum, a higher-risk profile may work for you. But if you are a retiree focused on wealth preservation and dependable drawdown income, my forensic standard is built to protect that. It is not built to accommodate a momentum trade that could derail 20 to 30 years of compounding.

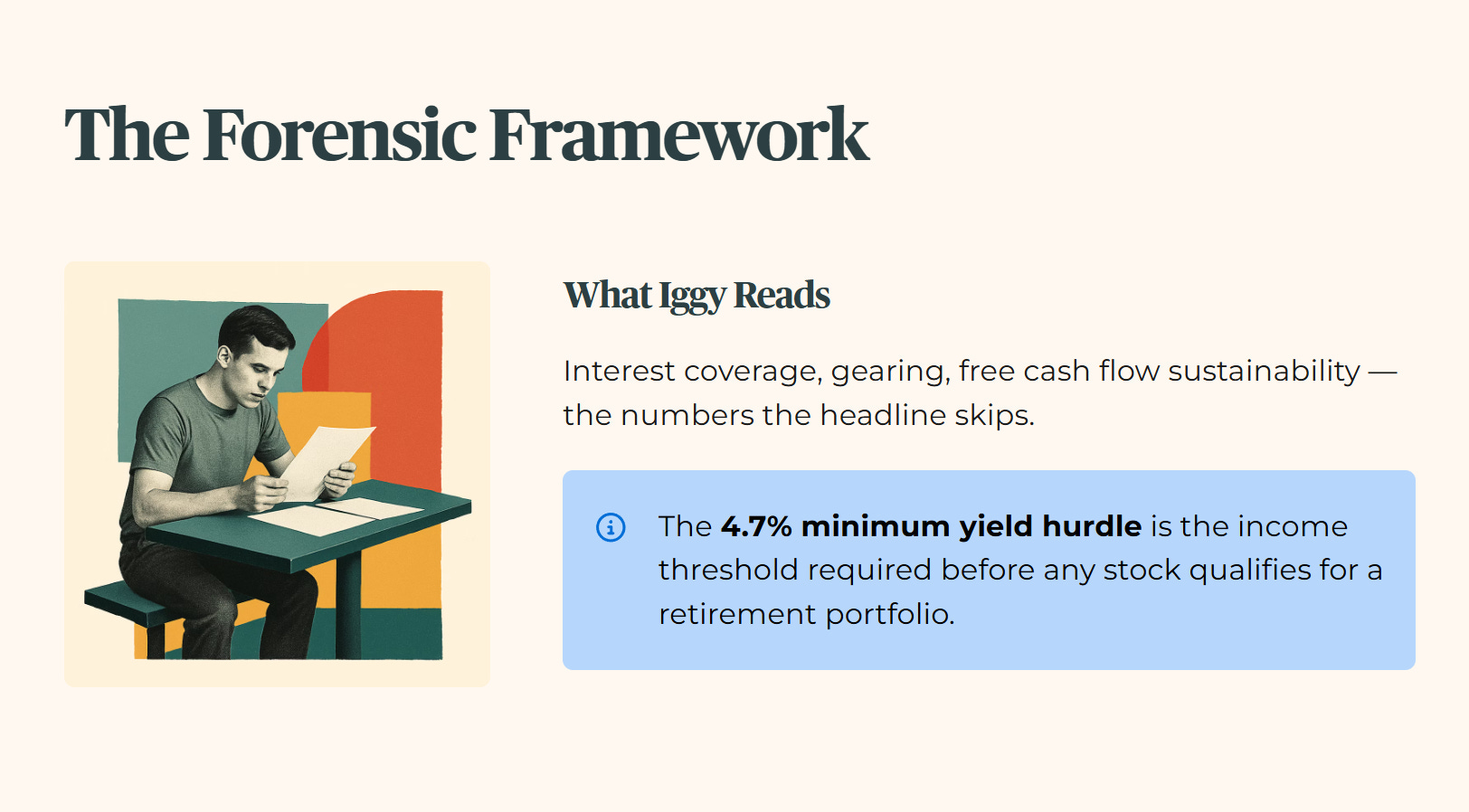

My job is simple, even if the balance sheet is not. I read the numbers that the headline skips: the interest coverage, the gearing, the free cash flow sustainability, so that the Singaporean building or living off a dividend portfolio gets the same forensic clarity that institutional money takes for granted.

This piece runs two of Singapore’s most watched restructuring stories through that framework. We look past the headline numbers to see what is actually happening to your portfolio cash flow. When I refer to the 4.7% minimum yield hurdle throughout, that is the income threshold I require before any stock qualifies for a retirement portfolio, not a market consensus figure, but a forensic standard calibrated to compensate for the risk of being in the open market at all.

In This Article:

Why Restructuring Is Not Always What It Looks Like

SingTel: The Asset Recycling Audit

Iggy’s Forensic Zone: Zone 4, Caution

The Big Three: What S$8.5 Billion in Capital Returns Actually Means

The Forensic Principle That Connects Both Stories

The Bottom Line

Why Restructuring Is Not Always What It Looks Like

The restructuring narrative on the SGX in 2026 is relentlessly positive. SingTel is moving toward an asset-light model and recycling its capital. The Big Three local banks are returning billions of dollars to shareholders. Keppel has transformed itself into an asset fund manager. The institutional framing from analysts and brokers is constructive across the board.

But we need to apply a forensic reframe.

Restructuring is simply a change in balance sheet arithmetic. It is not automatically good or bad for dividend sustainability. The critical question is whether the underlying cash flows that support the distribution are getting stronger or weaker as the restructuring proceeds. That distinction is what this piece is designed to answer for your retirement portfolio.

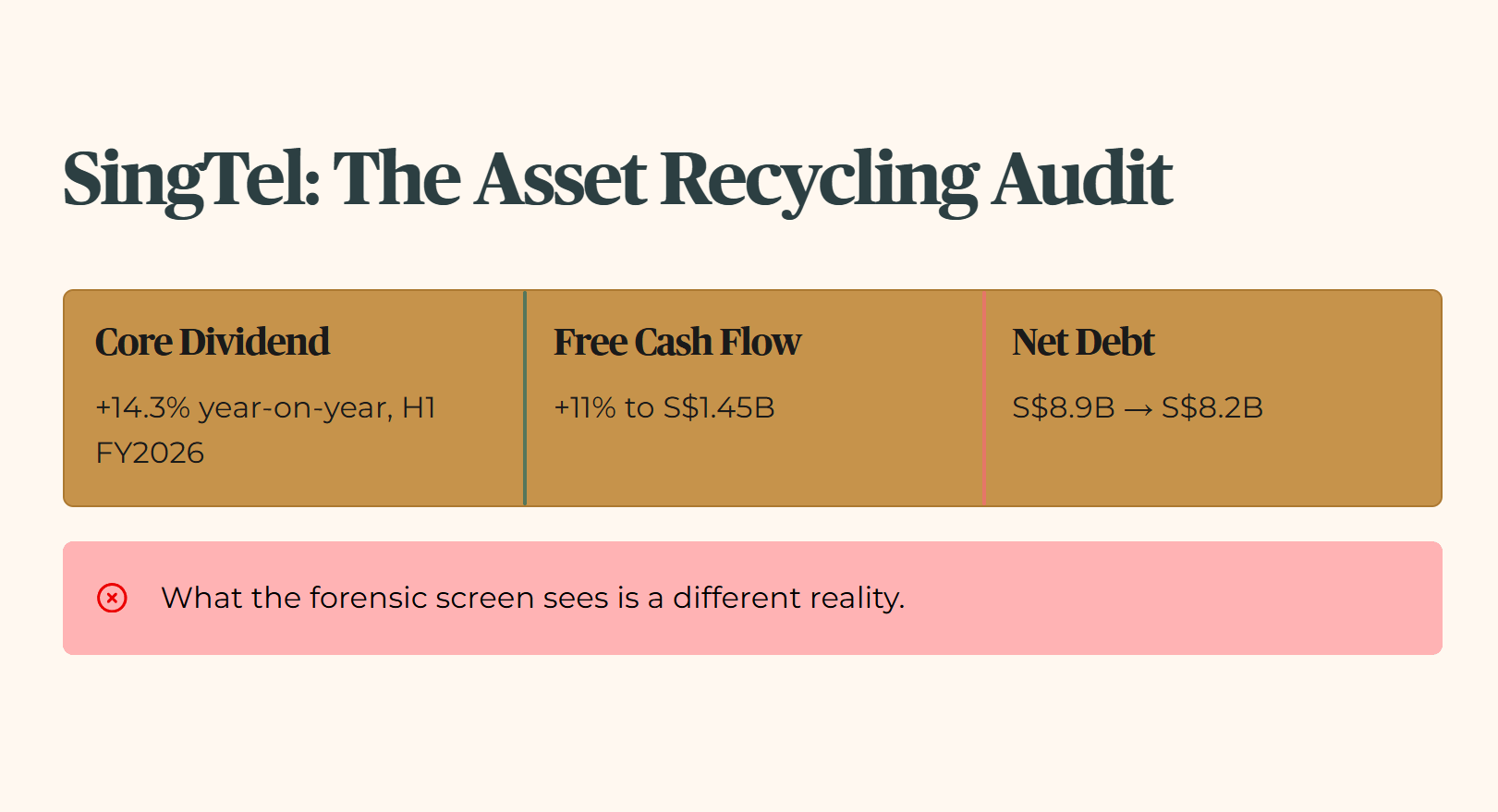

SingTel: The Asset Recycling Audit

What the market sees looks remarkably clean.

SingTel’s core dividend rose 14.3% year-on-year in the first half of FY2026. Free cash flow rose 11% to S$1.45 billion. Net debt declined from S$8.9 billion to S$8.2 billion through free cash flow generation and asset monetisation. The headline numbers show a growing core payout, record total distributions, and a declining net debt load.

What the forensic screen sees is a different reality.

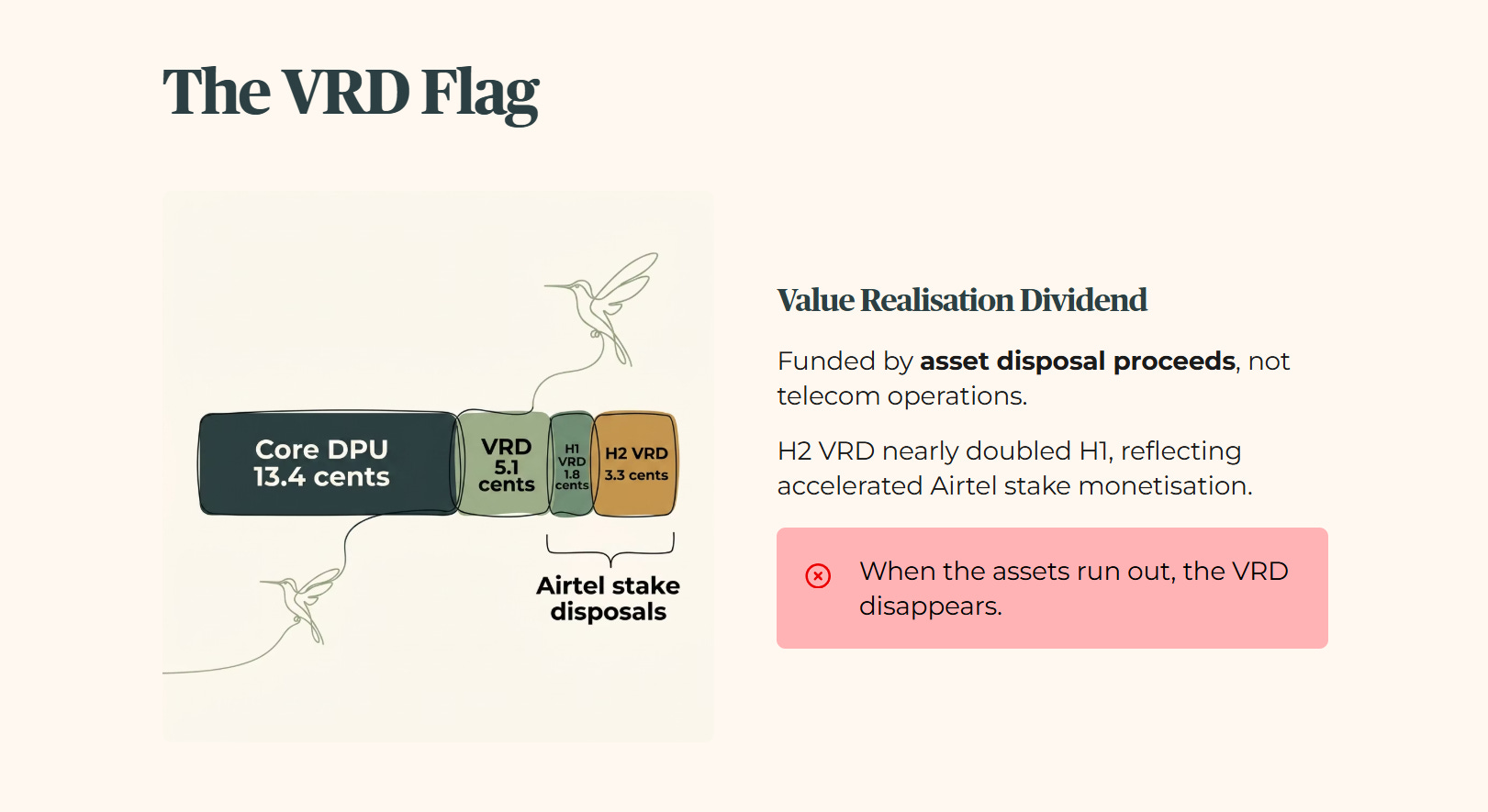

The load-bearing issue is the VRD flag. VRD stands for Value Realisation Dividend, a special payout funded not from telecom operations but from the proceeds of selling off corporate assets. SingTel’s full-year FY2026 dividend consists of a core component of 13.4 cents per share and a VRD component of 5.1 cents per share, split across two halves. The H1 VRD was 1.8 cents. The H2 VRD came in at 3.3 cents, nearly double the first half, reflecting accelerated monetisation of SingTel’s Airtel stake in the second half of the year.

The VRD is not earned income from regular business operations. It is asset disposal proceeds redistributed as a dividend. When the assets run out, the VRD component disappears.

Furthermore, SingTel guides for low to mid single digit growth in operating company EBIT for FY2027. EBIT stands for earnings before interest and taxes, the profit a company generates from its core business before accounting for debt costs and taxes. This guidance sits below consensus expectations of 12% or more growth. The Singapore consumer market remains challenged by weak mobile ARPU and severe competitive pressures. ARPU stands for average revenue per user, the amount of money the telecom earns from each customer.

SingTel’s FY2026 total dividend of 18.5 cents per share against a share price of S$4.18 produces a yield of approximately 4.43%. That fails my 4.7% minimum yield hurdle, the income threshold I require before any stock qualifies for a retirement portfolio. At the current price, this stock is not compensating you adequately for the risk of being in the open market.

Iggy’s Forensic Zone: Zone 4, Caution

My Zone 4 Caution verdict carries forward from previous audits. The asset recycling programme is real and the balance sheet is improving. Neither fact changes the yield arithmetic at the current price. The VRD component is a distribution of capital, not recurring earnings. A retirement investor who requires dependable drawdown income cannot rely on asset disposal proceeds as a sustainable income stream.

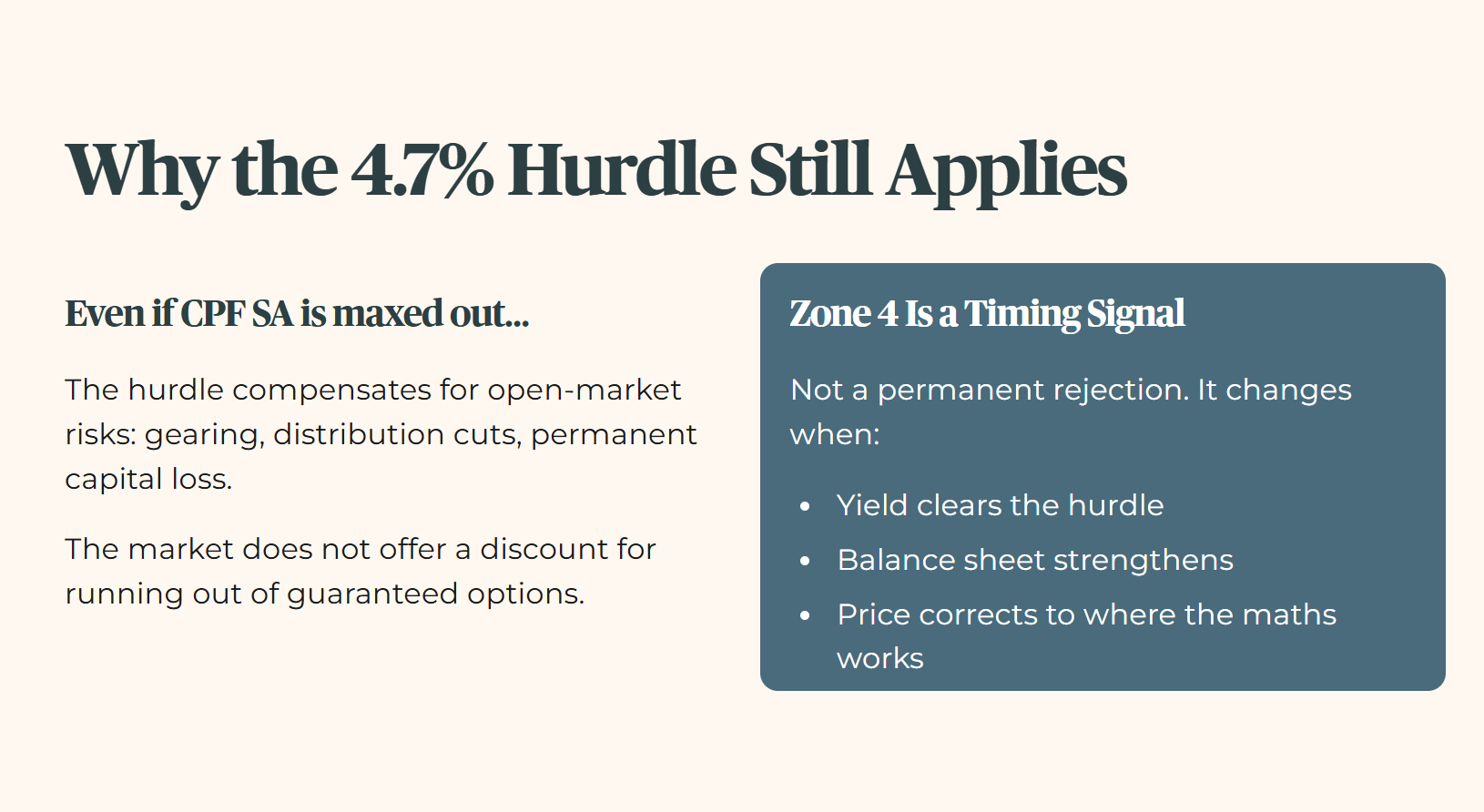

A common question worth addressing directly: if CPF SA is already maxed out, why does the 4.7% yield hurdle still apply to the dollars sitting outside the CPF system?

The answer is that the hurdle has nothing to do with what CPF will or will not pay you. It is the minimum return that justifies the risks you are taking on by being in the open market at all: gearing risk, distribution cuts, and the possibility of permanent capital loss. Those risks do not get cheaper because your CPF headroom is exhausted. The market does not offer you a discount for running out of guaranteed options.

The Zone 4 verdict here is not a permanent rejection. It is a forensic timing signal. At the current yield and price, this stock is not compensating you adequately for the risk you would be taking on. That changes when the yield clears the hurdle, when the balance sheet strengthens, or when the price corrects to a level where the maths works. When any of those conditions are met, Iggy will say so.

Until then, the framework holds, because the framework exists precisely for the moments when there is pressure to compromise it.

🦎 Iggy’s Insight

SingTel is using asset sales to fund a dividend expansion that its operating companies cannot support on their own. The core dividend, 13.4 cents for FY2026, is the only number that tells you whether regular telecom operations can support your retirement income position safely. The VRD added 5.1 cents this year, funded by Airtel stake disposals. Asset disposal proceeds are a finite resource, not a sustainable business model. A dividend backed by asset sales is a one-time event with a recurring label. When the assets run out, the yield resets. The forensic question is never what SingTel paid last year. It is what the core earnings can sustain when the recycling programme ends.

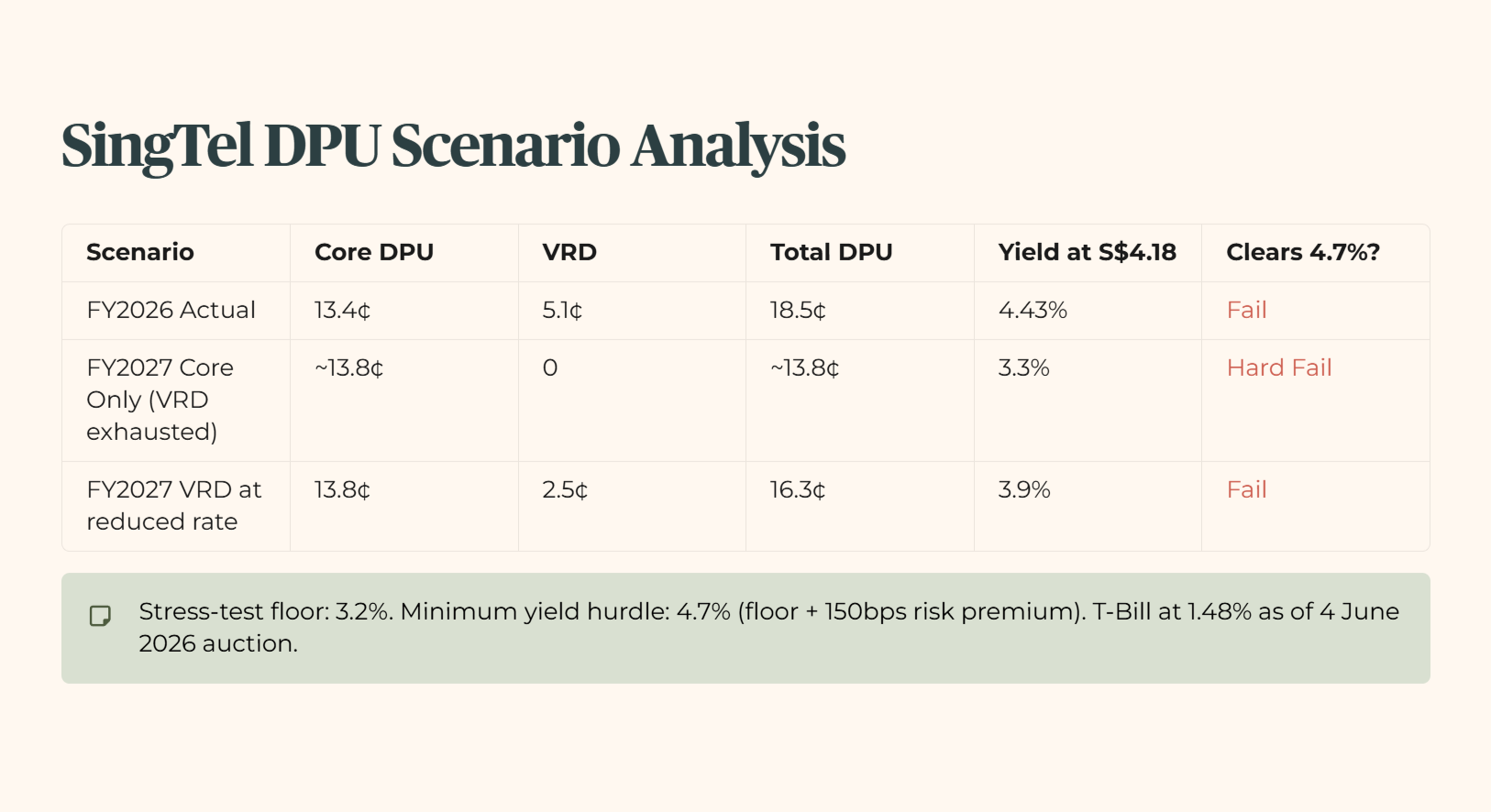

Below is the updated forensic scenario table analysing the SingTel dividend components:

Table 1: SingTel DPU decomposition scenario analysis

Note on the Stress-Test Buffer: For this audit, I apply a conservative floor of 3.2%. The T-Bill sits at 1.48% as of the 4 June 2026 auction. I do not lower my standards to match a temporary market dip. My floor remains at 3.2% to ensure sanctuary assets can withstand a return to long-term average interest rates. The minimum yield hurdle is 4.7%, which is the 3.2% floor plus 150 basis points of mandatory risk premium. SingTel has not guided a specific VRD per share for FY2027; the reduced-rate scenario above is an illustrative assumption under the current VRD framework, not an announced figure.

The next section runs the same 4.7% hurdle and durable‑vs‑headline yield decomposition through DBS, OCBC, and UOB’s S$8.5 billion capital return pool, and the CET1 maths resets more than one of those “blue‑chip” income stories.