Introduction: The Growing Role of Annuities in Singapore’s Retirement Landscape Annuities are gaining traction as a sought-after retirement planning tool in Singapore. With an aging population and fluctuating markets, the financial future for retirees is more uncertain than ever. It's no surprise that many Singaporeans are turning to annuities, often facilitated through CPF and SRS, to ensure a stable income during their twilight years. This guide delves into 10 crucial facts about annuities to help you understand how they fit into the broader financial and investment landscape in Singapore. 1. What Are Annuities?Annuities are long-term investment products designed to offer a guaranteed income, typically upon retirement. In Singapore, annuities can be purchased privately or can be part of your CPF LIFE scheme. The mechanics are simple: you pay a lump sum or a series of payments into an annuity fund, and in return, the annuity promises to pay you a fixed income at a future date. Understanding the basic structure of annuities is the first step towards incorporating them into your retirement planning. As with any investment, it's critical to scrutinize the terms, such as payout rates and associated fees, to ensure it aligns with your financial goals. 2. Annuities and CPF LIFE The Central Provident Fund (CPF) offers CPF LIFE (Lifelong Income for the Elderly), an annuity scheme designed to provide a monthly income for retirees. CPF LIFE is a significant milestone for retirement planning in Singapore as it guarantees an income for as long as you live. You can start receiving payouts as early as age 65, depending on your preferences and financial needs. Given its critical role in securing financial comfort for the elderly, understanding CPF LIFE is paramount for anyone considering annuities as part of their retirement strategy in Singapore. 3. The Supplementary Retirement Scheme (SRS) The Supplementary Retirement Scheme (SRS) is another platform that can be utilized to invest in annuities. It’s a voluntary scheme that complements the mandatory CPF savings. Contributions to the SRS account are eligible for tax deductions, providing a tax-efficient pathway to invest in annuities. Moreover, the flexibility of the SRS account allows for a range of investment options, which means you can diversify your retirement portfolio while still maintaining a core annuity investment. Considering the tax benefits and flexibility, the SRS serves as an excellent supplement to CPF for investing in annuities. 4. Annuities vs. Singapore Treasury Bills Singapore Treasury Bills are short-term securities that offer a risk-free way to invest your funds. These are backed by the Singapore Government and are considered extremely low-risk. However, the returns are generally lower than what you could expect from a well-chosen annuity. If you’re looking for guaranteed, higher returns and are comfortable locking away your funds for an extended period, annuities may offer a more suitable option for your retirement planning. Knowing when to invest in low-risk treasury bills versus annuities could make a considerable difference in your retirement savings. 5. Diversification and Annuities Just like any other investment, annuities should not make up 100% of your retirement portfolio. Diversification is key to mitigating risks and maximizing returns. The Singaporean market offers various investment vehicles like real estate, equities, and bonds, which can complement your annuity investments. Given that annuities are more illiquid and generally have longer lock-in periods, having other more liquid and potentially higher-return investments in your portfolio is crucial for balanced financial planning. 6. Tax Implications of Annuities One of the biggest draws of annuities in Singapore is their tax-deferred status. This means you won't have to pay taxes on the interest, dividends, or capital gains accumulating on your annuity until you start receiving payouts. Understanding the tax benefits can greatly enhance your long-term financial planning. The tax-deferred status can be particularly beneficial for higher earners looking to minimize their taxable income in retirement. 7. Costs and Fees Annuities are not without costs. They come with various fees such as administrative fees, management fees, and surrender charges if you decide to withdraw your funds early. Always read the fine print and understand what fees you'll incur over the life of the annuity. High fees can eat into your returns, compromising the financial security you're seeking in retirement. 8. Inflation Risk Annuities provide a fixed or variable income, but they usually don't account for inflation. The purchasing power of your annuity payments could diminish over time, particularly in an economy experiencing high inflation. To counter this, some annuities offer an inflation-adjustment feature at an additional cost. Weighing the benefits against the extra costs is essential in determining whether an inflation-adjusted annuity fits into your financial strategy. 9. Beneficiary Designations Annuities can be an integral part of estate planning. Many annuity schemes allow you to name a beneficiary who will receive the remaining funds or income streams upon your death. It’s crucial to review and, if necessary, update your beneficiary information to ensure your financial assets are distributed according to your wishes. Neglecting this aspect could lead to unwanted legal complexities for your loved ones. 10. Liquidity Concerns One of the most significant drawbacks of annuities is their lack of liquidity. Once you commit a lump sum or series of payments, those funds are generally locked in for a long period. Some annuities do offer withdrawal options, but these often come with hefty penalties. If you're someone who values liquidity and wants to keep options open for other investment opportunities, make sure to account for this characteristic of annuities in your overall financial planning. Conclusion: Are Annuities Right for Your Retirement in Singapore?Annuities can serve as a financial cornerstone for retirees, providing a steady income stream that can last a lifetime. However, they are not a one-size-fits-all solution. Understanding the various facets, from CPF and SRS options to the risks and rewards of other investment avenues like Singapore Treasury Bills, is crucial. As you journey towards retirement, take the time to analyze whether annuities align with your financial aspirations and needs. A well-informed decision today could mean a more secure and comfortable retirement tomorrow in Singapore.

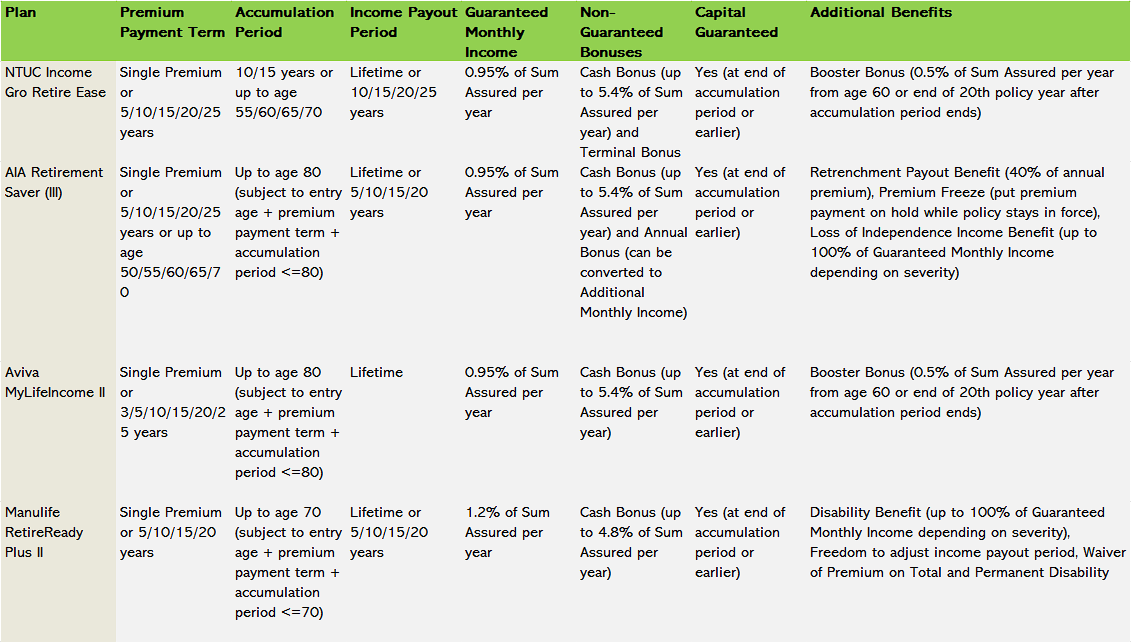

IntroductionIf you are planning for your retirement, you may have heard of annuity plans. Annuity plans are a type of insurance product that can provide you with a steady stream of income for life or a fixed number of years after you retire. They can supplement your CPF LIFE payouts and give you more financial freedom and security in your golden years. But how do annuity plans work? And what are the best ones available in Singapore? In this article, we will answer these questions and compare four of the best annuity plans in Singapore: NTUC Income Gro Retire Ease, AIA Retirement Saver (III), Aviva MyLifeIncome II, and Manulife RetireReady Plus II. How do annuity plans work?How do annuity plans work? Annuity plans work like this: you pay a lump sum or regular premiums to an insurance company during your working years, and in return, you get a monthly payout starting from a certain age, usually 65 or 70. The monthly payout consists of two components: a guaranteed monthly income and a non-guaranteed bonus. The guaranteed monthly income is a fixed amount that is determined by the sum assured, which is the amount of money that the insurance company promises to pay you or your beneficiaries upon death or maturity of the policy. The sum assured is usually based on your age, gender, health status, premium payment term, and accumulation period. The non-guaranteed bonus is an extra amount that is determined by the performance of the insurance company’s participating fund, which is a pool of money that is invested in various assets such as equities, bonds, properties, and cash. The non-guaranteed bonus can vary from year to year depending on the investment returns and expenses of the fund. The monthly payout can be received for life or for a fixed number of years, depending on the plan you choose. Some plans also offer additional benefits such as retrenchment payout, premium freeze, loss of independence income, disability benefit, booster bonus, and waiver of premium.  How much income do you need in retirement?How much income do you need in retirement? But before we dive into the details, let me ask you a question: do you know how much income you'll need to retire comfortably in Singapore? According to a study by the Lee Kuan Yew School of Public Policy, the average monthly household expenditure for retirees in 2022 was about $1,250. That means you'll need at least $15,000 per year to cover your basic living expenses. How about Your CPF Life Payouts?But what about your CPF LIFE payouts? Can they provide enough income for your retirement? Well, that depends on how much CPF savings you have and how much CPF LIFE payouts you can get. According to the CPF website , the current Basic Retirement Sum (BRS) is $93,000. If you have this amount in your Retirement Account at age 55, you can expect to receive about $740 to $800 per month from age 65 onwards. That’s not too bad, but it’s still below the average household expenditure for retirees. What if you have more CPF savings? Well, the current Full Retirement Sum (FRS) is $186,000. If you have this amount in your Retirement Account at age 55, you can expect to receive about $1,390 to $1,490 per month from age 65 onwards. That’s pretty good, but it’s still just enough to cover your basic living expenses. What if you want to have more income to enjoy a better quality of life in retirement? What if you want to travel the world, pursue your hobbies, or spoil your grandchildren? Well, that’s where annuity plans come in handy. They can supplement your CPF LIFE payouts and give you more financial freedom and security in your golden years. Let's look at the best 4 annuity plans in Singapore as per CPF websiteWhat are the best retirement annuity plans in Singapore? Now that you have an idea of how much income you will need in retirement, let’s take a look at some of the best annuity plans in Singapore: NTUC Income Gro Retire Ease , AIA Retirement Saver (III) , Aviva MyLifeIncome II , and Manulife RetireReady Plus II . Here’s a table that summarizes their main features and benefits:  As you can see, there are some similarities and differences among the four plans. Let’s go through them one by one and see what they have to offer. NTUC Income Gro Retire EaseThis plan offers you the option to receive a lifetime income or a fixed income for 10, 15, 20, or 25 years. You can choose to pay a single premium or regular premiums for 5, 10, 15, 20, or 25 years. You can also choose your accumulation period from 10 or 15 years, or up to age 55, 60, 65, or 70. The guaranteed monthly income is 0.95% of the sum assured per year, which is the same as AIA and Aviva. However, the non-guaranteed bonuses are slightly higher, with a cash bonus of up to 5.4% of the sum assured per year and a terminal bonus at maturity or death. You also get a booster bonus of 0.5% of the sum assured per year starting from age 60 or the end of the 20th policy year after the accumulation period ends, whichever is later. The capital is guaranteed at the end of the accumulation period or earlier, depending on your premium payment term. For example, if you pay a single premium, your capital is guaranteed at the end of the eighth policy year. If you pay regular premiums for five years, your capital is guaranteed at the end of the 15th policy year. One drawback of this plan is that it does not offer any additional benefits for retrenchment, premium freeze, or loss of independence. However, you can add on supplementary benefits such as cancer premium waiver, easy term, and easy payer premium waiver for extra protection.  AIA Retirement Saver (III) This plan offers you the option to receive a lifetime income or a fixed income for 5, 10, 15, or 20 years. You can choose to pay a single premium or regular premiums for up to age 50, 55, 60, 65, or 70. You can also choose your accumulation period up to age 80, subject to your entry age plus premium payment term plus accumulation period being less than or equal to 80. The guaranteed monthly income is also 0.95% of the sum assured per year, but the non-guaranteed bonuses are slightly lower, with a cash bonus of up to 5.4% of the sum assured per year and an annual bonus that can be converted to additional monthly income at a non-guaranteed rate. The capital is also guaranteed at the end of the accumulation period or earlier, depending on your premium payment term. For example, if you pay a single premium, your capital is guaranteed at the end of the eighth policyyear. If you pay regular premiums for three years, your capital is guaranteed at the end of the 13th policy year. One advantage of this plan is that it offers some additional benefits for retrenchment, premium freeze, and loss of independence. If you are retrenched during your premium payment term and remain unemployed for at least three months, you will receive a lump sum payout of 40% of your annual premium. If you face financial difficulties during your premium payment term, you can put your premium payment on hold for up to two years while your policy stays in force. If you suffer from loss of independence during your income payout period, you will receive up to an additional 100% of your guaranteed monthly income depending on the severity of your condition. Aviva MyLifeIncome IIThis plan offers you the option to receive a lifetime income only. You can choose to pay a single premium or regular premiums for 3, 5, 10, 15, 20, or 25 years. You can also choose your accumulation period up to age 80, subject to your entry age plus premium payment term plus accumulation period being less than or equal to 80. The guaranteed monthly income is also 0.95% of the sum assured per year, and the non-guaranteed bonuses are the same as NTUC Income, with a cash bonus of up to 5.4% of the sum assured per year and a terminal bonus at maturity or death. You also get the same booster bonus of 0.5% of the sum assured per year starting from age 60 or the end of the 20th policy year after the accumulation period ends, whichever is later. The capital is also guaranteed at the end of the accumulation period or earlier, depending on your premium payment term. For example, if you pay a single premium, your capital is guaranteed at the end of the eighth policy year. If you pay regular premiums for three years, your capital is guaranteed at the end of the 13th policy year. One drawback of this plan is that it does not offer any additional benefits for retrenchment, premium freeze, or loss of independence. However, you can add on supplementary benefits such as cancer premium waiver, easy term, and easy payer premium waiver for extra protection.  Manulife RetireReady Plus IIThis plan offers you the option to receive a lifetime income or a fixed income for 5, 10, 15, or 20 years. You can choose to pay a single premium or regular premiums for 5, 10, 15, or 20 years. You can also choose your accumulation period up to age 70, subject to your entry age plus premium payment term plus accumulation period being less than or equal to 70. The guaranteed monthly income is higher than the other three plans, at 1.2% of the sum assured per year. However, the non-guaranteed bonuses are lower, with a cash bonus of up to 4.8% of the sum assured per year only. The capital is also guaranteed at the end of the accumulation period or earlier, depending on your premium payment term. For example, if you pay a single premium, your capital is guaranteed at the end of the eighth policy year. If you pay regular premiums for five years, your capital is guaranteed at the end of the 15th policy year. One advantage of this plan is that it offers some additional benefits for disability and premium waiver. If you suffer from total and permanent disability during your premium payment term, you will receive a waiver of future premiums and continue to receive your monthly income. If you suffer from disability during your income payout period, you will receive up to an additional 100% of your guaranteed monthly income depending on the severity of your condition. Another advantage of this plan is that it gives you more flexibility to adjust your income payout period. You can choose to shorten or lengthen your income payout period by up to five years before it starts, subject to certain conditions and charges. How to choose the best annuity plan for you?So there you have it: four of the best annuity plans in Singapore that can help you achieve your retirement goals. Which one should you choose? Well, that depends on your personal preferences and circumstances. Here are some factors that you may want to consider:

To help you make an informed decision, you may want to consult a financial adviser who can assess your needs and recommend the best plan for you. You may also want to compare different plans using online tools such as MoneySmart’s annuity comparison tool or SingSaver’s annuity comparison tool.  ConclusionAnnuity plans are a great way to secure your retirement income and enjoy a better quality of life in your golden years. They can supplement your CPF LIFE payouts and give you more financial freedom and security. However, not all annuity plans are created equal. Some offer higher payouts, some offer more flexibility, some offer more protection, and some offer more bonuses. How do you choose the best one for your retirement needs?

In this article, we have compared four of the best annuity plans in Singapore: NTUC Income Gro Retire Ease, AIA Retirement Saver (III), Aviva MyLifeIncome II, and Manulife RetireReady Plus II. We have looked at their features, benefits, pros and cons, and see how they stack up against each other. We have also given you some factors to consider when choosing an annuity plan. We hope this article has given you some insights into annuity plans and how they can help you secure your retirement income. If you have any questions or comments, please feel free to leave them below. And if you found this article helpful, please share it with your friends and family who may benefit from it. Thank you for reading, and we wish you a happy and prosperous retirement! Read more in detail from CPF's website. |

Author🦖 Welcome to the Investing Iguana YouTube channel, your one-stop destination for all things related to investment tips, news, and advice! Our mission is to empower you with the knowledge and insights you need to make informed investment decisions and grow your wealth. With a perfect blend of engaging content, expert advice, and practical strategies, the Investing Iguana is here to guide you through the complex world of investing and help you achieve your financial goals. ArchivesCategories |

RSS Feed

RSS Feed