IntroductionWelcome back to the Investing Iguana, where we turn the maze of financial planning into a straightforward path to wealth. I'm Iggy, your navigator in the world of savings and investments. The Investing Iguana is featured and ranked 8th in the "2023 Influential Tigers" by Tiger Brokers. Today, we’re embarking on an in-depth exploration of Singapore’s Budget for the year 2024. Our focus is on a subject that resonates deeply with many Singaporeans - the modifications to the Central Provident Fund (CPF) system. The CPF system is a key pillar of Singapore’s social security structure, and changes to it can have significant implications for citizens’ retirement plans. Our specific area of interest is how these imminent adjustments can be leveraged to bolster your retirement savings. If you’re on the cusp of retirement or in the process of planning for your future, this is a topic you’ll want to delve into. The upcoming changes could have a profound impact on your retirement years, and understanding them is crucial to making informed decisions about your financial future. We’re about to delve into the nitty-gritty of these changes, shedding light on how they could affect your golden years. But we won’t stop at just explaining the changes. We’ll also provide insights on strategic moves you can make to optimize your retirement savings. Our goal is to equip you with the knowledge and strategies you need to navigate these changes and ensure a comfortable retirement. So, let’s dive in and uncover the potential of the new CPF system for your retirement planning.  Major Updates in Singapore’s Retirement Scheme

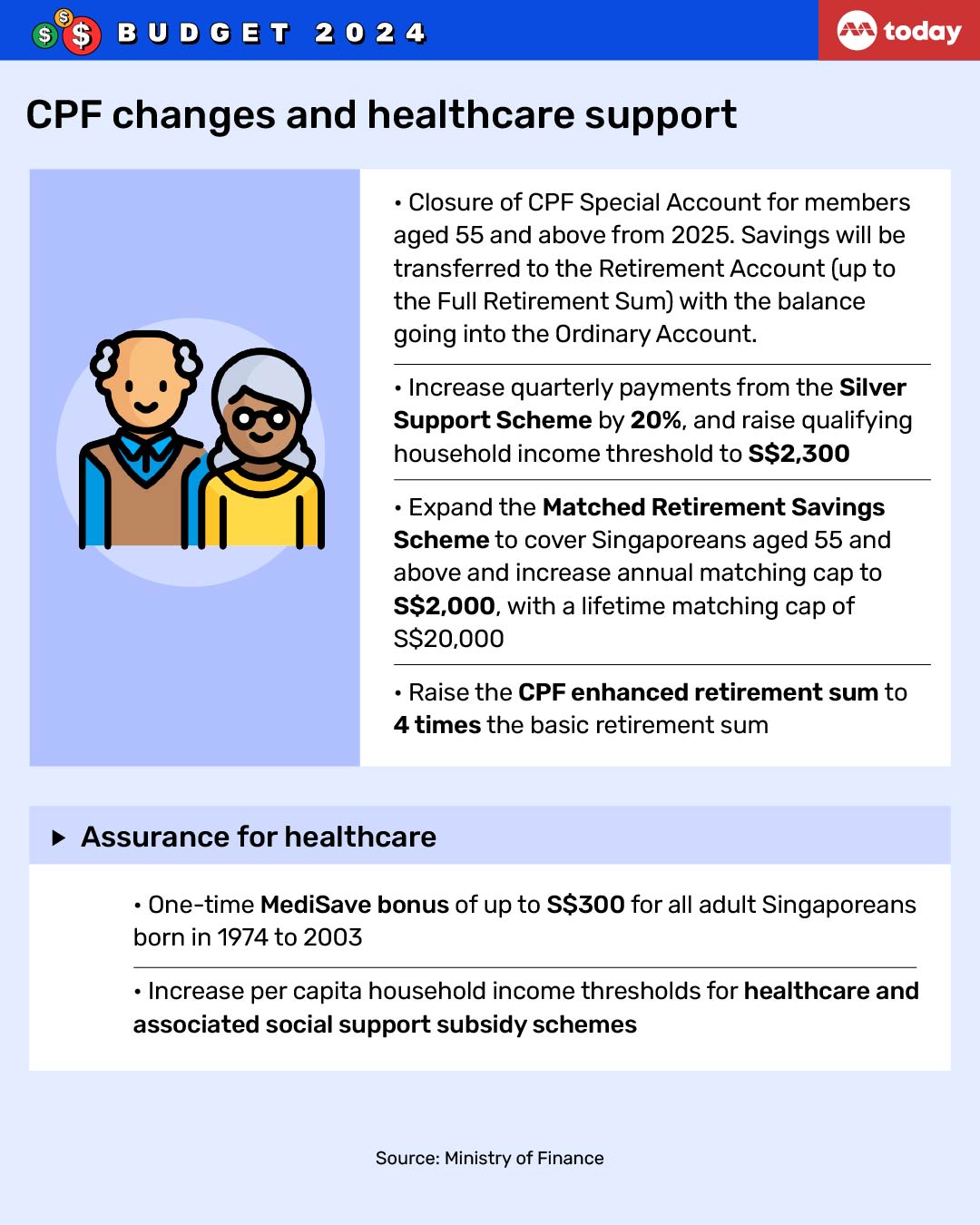

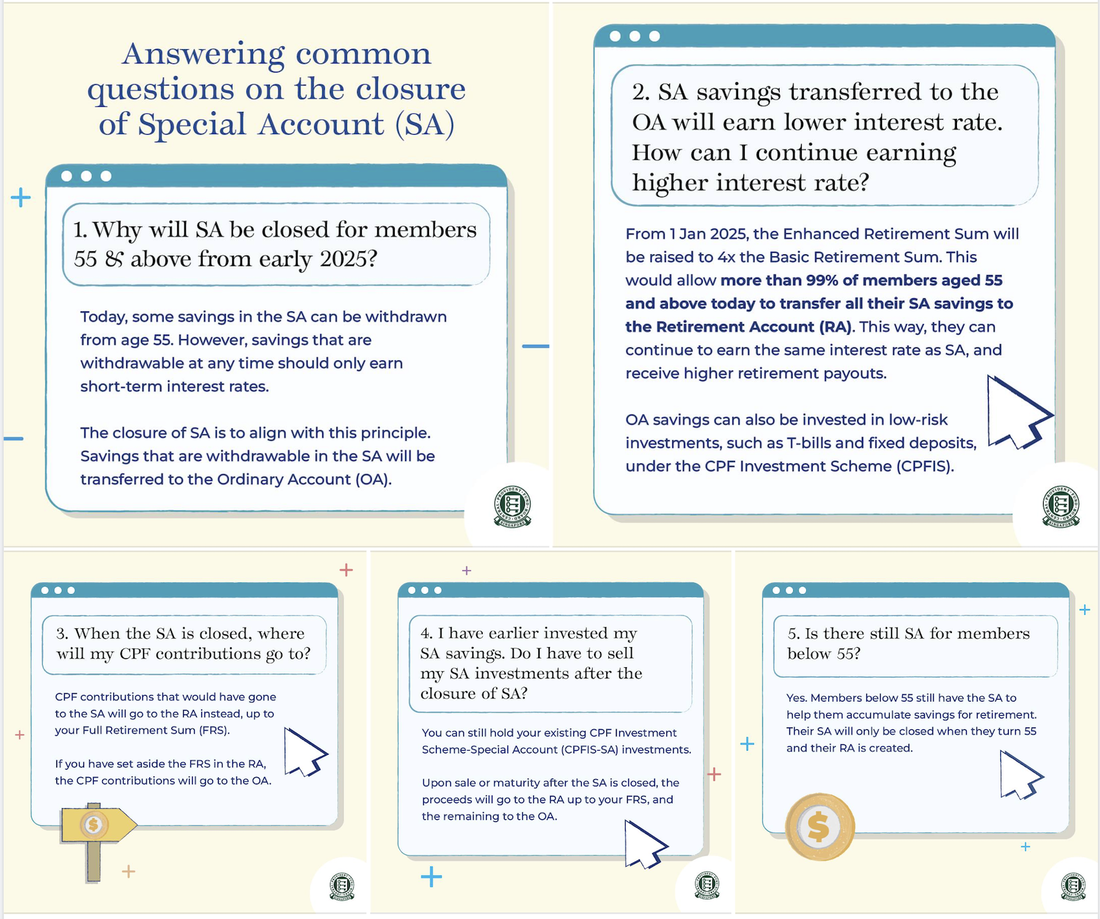

At the core of these changes is a major update that has been creating quite a buzz – the discontinuation of the CPF Special Account (SA) for members who reach the age of 55, which will take effect from 2025. This is a significant shift as the SA has traditionally been a crucial component of retirement savings for many Singaporeans. But that’s not all! There’s another key change on the horizon. The Enhanced Retirement Sum (ERS), which is an optional higher retirement sum that members can set aside for greater monthly payouts in retirement, is set to increase to four times the Basic Retirement Sum (BRS). This means that if you choose to set aside the ERS, you could potentially receive higher monthly payouts during your retirement. You might be asking, “What implications do these changes have for me?” Well, the closure of the SA could mean that you’ll need to reassess your retirement savings strategy. You might need to consider other avenues for saving or investing to ensure you have sufficient funds for your retirement. As for the increase in the ERS, if you’re able to set aside more funds in your CPF account, this could mean higher monthly payouts when you retire. However, it’s important to consider your personal circumstances and financial goals when deciding whether to set aside the ERS.  Key Retirement Sums in CPF SystemIndeed, the CPF system is structured around three key retirement sums: the Basic Retirement Sum (BRS), the Full Retirement Sum (FRS), and the Enhanced Retirement Sum (ERS). These sums serve as benchmarks for the amount of savings you should aim to accumulate in your CPF accounts for a comfortable retirement. The Basic Retirement Sum (BRS) is the minimum amount that you should have in your CPF accounts when you reach the age of 55. This sum is designed to provide for basic living expenses in retirement. The Full Retirement Sum (FRS) is essentially twice the amount of the BRS. If you have more savings and want a higher level of retirement income, you can opt to set aside the FRS in your CPF accounts. The Enhanced Retirement Sum (ERS) is the highest retirement sum that you can set aside in your CPF accounts. It is three times the amount of the BRS and provides for the highest level of retirement income. With the upcoming changes, the ERS is set to increase to four times the BRS, which means that if you’re able to set aside more funds in your CPF account, you could potentially receive higher monthly payouts during your retirement. Understanding these terms and their implications is crucial for effective retirement planning. By knowing how much you need to save and how these sums can impact your retirement income, you can make informed decisions and plan strategically for your golden years. CPF System’s Retirement Savings Goals The Full Retirement Sum (FRS) and the Basic Retirement Sum (BRS) are two key components of the CPF system that play a crucial role in your retirement planning. Let’s break down what these terms mean and how they impact your retirement savings. The Full Retirement Sum (FRS) is essentially your retirement savings goal. It’s set at double the amount of the Basic Retirement Sum (BRS). This means that if you’re turning 55 in the year 2024, your target should be to have S$205,800 in your CPF account. This sum is designed to provide a comfortable lifestyle in your retirement years, allowing you to maintain your standard of living even after you’ve stopped working. On the other hand, the Basic Retirement Sum (BRS) serves as the foundation of your retirement savings. It’s the minimum amount you should aim to have in your CPF account when you retire. For those turning 55 in 2024, this sum is set at S$102,900. The BRS is calculated to cover your basic living needs in retirement, excluding rental expenses. This ensures that even at the very least, you’ll have enough to cover your basic necessities during your golden years.  Enhanced Retirement Sum’s Significant ChangeThe Enhanced Retirement Sum (ERS) is another crucial component of the CPF system. Until recently, the ERS was set at three times the Basic Retirement Sum (BRS). However, a significant change is on the horizon. Starting from 2025, the ERS will increase to four times the BRS. This change marks a significant milestone in Singapore’s retirement planning landscape. You might be wondering why these changes are being implemented. The answer lies in the commitment of the CPF Board and the Singaporean government to continually adapt the CPF system to meet the evolving needs of Singaporeans. These changes are designed to ensure that Singaporeans can meet the cost of living and enjoy a higher standard of living in retirement. Moreover, these adjustments also take into account the realities of increased life expectancy. As people live longer, it’s important to have sufficient savings to cover the extended retirement years. By increasing the ERS, the CPF system provides a more robust safety net for Singaporeans as they navigate their retirement years.  Strategies for Meeting Retirement Sums

With the upcoming closure of the Special Account (SA) for those aged 55 and above, it’s natural to wonder about the strategies you can employ to ensure you’re on the right track to meeting your Full Retirement Sum (FRS) or even aiming for the Enhanced Retirement Sum (ERS). There are several pathways you can explore to enhance your retirement savings, each with its own benefits and considerations. One strategy is to transfer funds from your Ordinary Account (OA) to your Special Account (SA). The SA typically offers a higher interest rate than the OA, which means your savings could grow faster in the SA. However, it’s important to note that once transferred, the funds cannot be moved back to the OA. Therefore, this strategy requires careful consideration and planning. Another strategy is to leverage the Retirement Sum Top-Up scheme. This scheme allows you to top up your own or your loved ones’ CPF accounts with cash or CPF savings. In addition to boosting your retirement savings, these top-ups also qualify for tax reliefs, which could potentially reduce your tax bill. You could also explore the CPF Investment Scheme (CPFIS), which allows you to invest your CPF savings in a wide range of investment products for potentially higher returns. However, investing involves risks, and the returns are not guaranteed. Therefore, it’s crucial to understand the risks involved and consider your risk tolerance before investing your CPF savings. In essence, the pathways to enhancing your retirement savings are diverse and each has its own set of advantages and considerations. It’s important to understand these strategies, assess your financial situation and retirement goals, and make informed decisions that best suit your needs. Remember, retirement planning is not a one-size-fits-all process. It’s a journey that requires careful planning, regular review, and strategic adjustments along the way. ConclusionAs we wrap up this journey through the updates to Singapore's CPF system, remember, navigating these changes successfully requires understanding, planning, and a bit of strategy. And there you have it, folks—the lowdown on the CPF changes coming your way in 2024 and how you can turn these adjustments to your advantage. Remember, understanding these changes is the first step towards optimizing your retirement savings. If this video helped shed light on the path to maximizing your CPF funds, give us a thumbs up and hit that subscribe button for more insights into making your money work for you. Have any questions or need further clarification? Drop your thoughts in the comments below, and let's keep the conversation going. Until next time, stay savvy, plan wisely, and let's make the most of our retirement savings together. See you in the next video! IntroductionHey there, everyone! It's me, your ever-so-friendly Investing Iguana, also known as Iggy, and I'm back with another super important topic that's absolutely crucial for all my fellow Singaporeans! Whether you're getting closer to hanging up your work boots and enjoying retirement, or you're just a smart cookie who wants to plan ahead for those golden years, you've definitely clicked on the right video to watch. Today, we're going to explore every nook and cranny of CPF LIFE, which is Singapore's very own, one-of-a-kind pension scheme designed to help you live comfortably when you're older. So, go ahead and grab your favorite cup of kopi-o, or any other drink you like, and make yourself comfy because we're about to dive deep into this fascinating subject! But wait, before we jump into all the juicy details, do me a quick favor—go ahead and smash that like button below this video and hit subscribe so you won't miss out on any more of this awesome, informative content that I've got lined up just for you! CPF LIFE: Singapore's Never-Ending Birthday Gift for Seniors Sure, let's dive into the simple stuff first. You know how in many places around the world, there's a system to give older people some money to live on when they retire? It's usually called a pension. Well, in Singapore, we have our very own unique version of that, and it's called CPF LIFE. CPF LIFE stands for Lifelong Income For The Elderly, and it's like a super special savings plan just for people who are 65 or older. So, what happens is, once you turn 65, this plan starts to give you money every single month. And the best part? It doesn't stop! As long as you're alive, you'll keep getting this money month after month. It's like having a never-ending birthday gift that keeps on giving! So, it's not just a one-time thing; it's a lifelong deal that makes sure you have some income to rely on for the rest of your life. Isn't that awesome? Make Your Retirement Money Last Longer by Deferring Your Payouts Alright, let's break this down so it's super easy to understand. The money you'll get every month when you retire is based on two main things. The first thing is how much money you've saved up in your Retirement Account, which is also called an RA. Think of your RA like a piggy bank for your older self. The more money you put into this piggy bank, the more money you'll get to spend every month when you retire. But that's not the only way to get more money! There's a second option, and it's called deferring your payouts. This means you choose to wait a little longer to start taking money out of your piggy bank. If you decide to wait until after you turn 65, you'll get even more money every month. For each year you wait, your monthly amount goes up by about 7%. So, let's say you were going to get between $750 and $800 every month starting at age 65. If you wait until you're 70 to start taking money out, you could get between $990 and $1,070 every month instead. So, you have choices: save more now or wait a bit longer to start spending, and either way, you'll end up with more money to enjoy your golden years! CPF LIFE: Your Portable Money Machine in RetirementCPF LIFE is a really helpful program that gives you a bunch of advantages, especially when you get older and stop working. One of the coolest things about it is that it promises to give you money every month for the rest of your life. Imagine having a money machine that never stops; that's what the guaranteed monthly payout from CPF LIFE is like! It's like having a safety net made of money that you can always count on when you're older and not working anymore. But wait, there's more! CPF LIFE isn't a one-size-fits-all thing; it lets you pick from different plans. Think of it like going to an ice cream shop with lots of flavors; you can choose the one that you like the most. Whether you want more money now or more money later, there's a plan that's just right for you. And the best part? This program is like a portable money machine. Let's say you decide to move to another country when you're older; guess what? Your CPF LIFE money will follow you there! You'll still get your monthly payouts, even if you're sipping coconut water on a beach far, far away. So, in a nutshell, CPF LIFE gives you a reliable, never-ending flow of money, lets you pick a plan that fits you best, and will keep paying you no matter where in the world you are. CPF LIFE: A Safety Net with DrawbacksCPF LIFE is a program designed to provide Singaporeans with a monthly income during retirement, but it's not perfect and has some downsides you should know about. First, there's the issue of being stuck with your choice: once you pick a CPF LIFE plan, it's really hard to switch to another one, kind of like choosing a flavor of ice cream and not being able to change it later. Second, the money you get every month from CPF LIFE is usually not as much as what you could get from other retirement plans, like having a smaller slice of cake compared to other options. Lastly, there's the matter of what happens to your money if you pass away before turning 85. In that case, the remaining money in your CPF account won't go to your family or friends, almost like a game where you can't pass on your points to someone else. So, while CPF LIFE can be a good way to have some income when you're older, it's important to think about these drawbacks before making a decision. Ice Cream Scoops: Picking the Right CPF Plan for YouAlright, let's dive into the different plans you can choose from, and trust me, it's as easy as picking your favorite ice cream flavor! So, you have three awesome choices: Standard, Basic, and Escalating. First up is the Standard Plan, which is like the go-to option. Imagine it as getting a bigger scoop of ice cream every month, but having less to share with your friends and family later. On the flip side, the Basic Plan is like getting a smaller scoop each month, but you'll have more to share with your loved ones in the long run. Just a little warning: if you go with the Basic Plan, your monthly "scoops" could get even smaller if your CPF account has less than $60,000 in it. It's like running low on your ice cream stash! Finally, there's the Escalating Plan, which is super cool because it's like getting a 2% bigger scoop of ice cream every single year. This helps you keep up with things getting more expensive, like when your favorite hawker stall starts charging more for chicken rice. So, you see, each plan has its own perks and quirks, making sure you can pick the one that fits your life just right! The Best Retirement Plan for Seniors Who Want to Live to Be 85 or OlderSelecting a plan for your future isn't as easy as playing a quick game of "eeny, meeny, miny, moe." You really have to think about how long you're likely to live. In Singapore, if you look at everyone from babies to old folks, the average person lives to be 82.6 years old. But that number can be a bit misleading because it starts counting from the day you're born. If you've already celebrated your 65th birthday, the situation changes. On average, people who are 65 years old can expect to live for another 20.8 years, which means they'll reach around 85 or 86 years old. So, if you're 65 and you're thinking, "Hey, I might live to be 85 or even older," then the Basic Plan could be the best choice for you. It might offer you the most value for your money, helping you make the most out of your golden years. Retirement Planning: How to Choose the Right Plan for Your NeedsSure, let's dive deeper into these numbers and break it down so it's super easy to understand, okay? Imagine you're 55 years old and you've saved up what's called a Full Retirement Sum, which is $186,000. Now, fast forward to when you're 85 years old, and let's see how much money you could potentially have based on different plans. With the Standard Plan, you could end up with anywhere between $356,198 and $394,035. That's a lot, right? But wait, there's more! If you go for the Basic Plan, your money could grow to be between $419,830 and $460,126. That's even more money! Now, there's also something called the Escalating Plan, where you could have between $340,656 and $380,192 by the time you're 85. So, what does all this mean for you? Well, if you think you'll live until you're 85, the Basic Plan seems like the best choice because it gives you the most money. But hold on, if you're feeling super optimistic and think you'll live until you're 95 or even older, then you might want to consider the Standard or Escalating Plan. These plans could offer you more money in the long run. So, depending on how long you think you'll live, you can choose the plan that will give you the most bang for your buck! Your Health Today Determines Your Life TomorrowLife is full of surprises and you never really know what's going to happen next. It's impossible to predict exactly how many years you'll be around, but you can get a pretty good idea by looking at how healthy you are right now and the way you live your life. Think about the foods you eat, how much you exercise, and even how much stress you have, because all of these things can give you clues about your future health. Take a moment to really think about this. You might even want to talk it over with your family members, because they know you well and can offer good advice. Speaking to a financial advisor is also a smart move. They can help you plan for the future, especially when it comes to money matters. So, gather all this information and advice, and then make the most informed decision you can about what's best for you. It's all about taking steps today to set yourself up for a better, healthier future. CPF Life: A Step-by-Step Guide for Ages 55-60As the last useful tip for CPF Life, let me help by breaking it down in terms of milestones so that you have a better understanding on what to do at what age. Age 55: When you reach the age of 55, it's a good time to start thinking about your future and how you'll live when you're not working anymore. One way to do this is by using a special tool called the CPF LIFE calculator. This calculator helps you figure out how much money you'll get every month once you retire. It's like a sneak peek into your financial future! Additionally, you can give your future self a financial boost by adding more money to your CPF savings now. This will make your monthly payouts bigger when you do retire, so you'll have more money to enjoy your golden years. Age 60: At 60, you'll get a letter in the mail from the CPF Board. This letter will have important details about CPF LIFE, which is a program that helps you manage your money when you're older. You can also go to special events called CPF LIFE roadshows and seminars. These events are like mini-classes where experts teach you all about how CPF LIFE works and how it can benefit you. It's like going to school, but for learning about your retirement! CPF LIFE: Your Retirement Income Plan at 65, 70, and 85Age 65: When you turn 65, it's decision-making time! You'll need to pick a CPF LIFE plan that suits you best. Once you've made your choice, the money you've saved up in your CPF account will be used to buy something called a life annuity. Think of this like a magical money fountain that gives you a certain amount of money every month for the rest of your life. It's a way to make sure you always have money coming in, even when you're not working. Age 70: You have the option to delay, or "defer," starting your CPF LIFE payouts until you're 70 years old. But there are some rules you have to follow. For instance, if you've been a super saver and have more than $500,000 in your CPF account, you can only delay your payouts until you're 67. It's like a game with certain rules you have to play by. Age 85: If something happens and you pass away before you turn 85, don't worry—your money won't go to waste. The remaining money in your CPF account will be given to the people you care about, like your family or friends. These people are called your beneficiaries, and they'll receive the money you've saved up, so you can still help take care of them even if you're not around. How CPF LIFE Can Help You Achieve a Secure RetirementAlright, that's a wrap for today's deep dive into CPF LIFE! I hope this video helps you make a more informed decision about your retirement plans. We hope you enjoyed this video and learned something new. If you did, please give us a ‘Like’ to show your appreciation. It helps us know what kind of content you find useful and valuable. And if you haven’t already, please subscribe! Here at ‘The Investing Iguana’, we’re passionate about helping you achieve your financial goals with ease and peace of mind. And we have a lot more to share with you! Stay tuned for our upcoming videos, where we’ll explore other important financial topics like how to use CPF and SRS to boost your retirement savings, how to invest wisely and safely in the stock market, and how to make your money grow faster and smarter! We’re so grateful to have you as part of our ‘Investing Iguana’ family. Your support enables us to keep creating free content like this. Remember, every ‘like’, ‘share’, and ‘subscribe’ makes a difference! Thanks for watching today. Keep investing, keep learning, and we’ll see you in the next video. Take care!

Introduction: The CPF Dilemma in Singapore The Central Provident Fund (CPF) is not just a governmental retirement program; it’s a multi-faceted tool designed for Singaporeans to reach various life goals. From financing homes to setting up a sturdy retirement nest, CPF can be a game-changer. However, missteps can cost you in the long run. The key is to make educated decisions that align with your life stage and financial aspirations. This article serves as a guide, providing crucial insights and presenting facts to consider before tapping into your CPF account. 1. Understanding CPF's Triple Account Structure The CPF is divided into three accounts: Ordinary Account (OA), Special Account (SA), and Medisave Account (MA). Each serves a unique purpose. The OA is often used for housing and education. SA focuses on long-term retirement investments, and MA primarily deals with healthcare needs. The interest rates also differ, making it crucial to understand how best to allocate your CPF contributions among these accounts for optimized financial planning. On top of these base rates, you can also earn an extra 1% interest on the first $60,000 of your combined balances (with up to $20,000 from OA). This means that you can earn up to 3.5% interest on your OA balance and up to 5% interest on your SA and MA balances. The interest rates are reviewed quarterly and are adjusted according to the prevailing market conditions. However, they are guaranteed by the government to be at least 2.5% for OA and 4% for SA and MA. So why is this important? Well, because interest rates matter a lot when it comes to compounding your money over time. The higher the interest rate, the faster your money grows.  2. Exploring CPF Investment Schemes (CPFIS) The CPF Investment Scheme (CPFIS) enables Singaporeans to invest their OA and SA funds in a variety of financial instruments, such as stocks, bonds, and unit trusts. Although these investments can yield higher returns than the CPF's guaranteed interest rates, they come with their own set of risks. Thus, having a well-thought-out investment strategy is pivotal to leveraging the CPFIS effectively. 3. Making Sense of Voluntary Contributions For Singaporeans keen on amplifying their retirement corpus or other financial goals, voluntary contributions to CPF accounts offer a viable pathway. Not only do these contributions accelerate the growth of your funds, but they also come with tax benefits. These voluntary contributions are subject to an annual limit, so planning ahead is crucial.  4. Navigating Singapore Treasury Bills An alternative low-risk investment opportunity within the CPF ecosystem is Singapore Treasury Bills. These are short-term government-backed securities that offer a way to grow your money securely. While they might not offer the same return potential as other high-risk investments, they provide a safety net for those looking to diversify their investment portfolio. 5. Considering Supplementary Retirement Scheme (SRS) Beyond CPF, the Supplementary Retirement Scheme (SRS) serves as another avenue for tax-advantaged retirement savings in Singapore. Contributions to the SRS are eligible for tax reliefs, adding an extra layer of financial flexibility. When used in conjunction with CPF, SRS can greatly enhance your retirement planning strategy.  6. Leveraging CPF for Housing CPF allows for the withdrawal of funds for home purchases, a feature that has facilitated homeownership for many Singaporeans. However, it's important to be aware of the long-term impact of using your CPF for housing, as this could potentially deplete your retirement savings. A balanced approach is essential. 7. Understanding CPF Minimum Sum and CPF LIFE The CPF Minimum Sum is the minimum amount you must have in your retirement account upon reaching 55 years old. This sum is then used to provide monthly payouts via CPF LIFE, an annuity scheme, during your retirement years. Being aware of these thresholds and understanding the annuity payouts can significantly influence your retirement planning. 8. Tax Benefits and CPF Various tax incentives are tied to your CPF contributions. For instance, contributions to your Medisave Account or making voluntary contributions can significantly reduce your taxable income. Tax planning should be an integral part of your overall CPF strategy, as it can result in substantial savings. 9. Dipping into CPF for Education Education is another sector where CPF can be utilized, specifically through the CPF Education Scheme. While this can ease the financial burden of educational expenses, it's worth noting that the amount withdrawn plus interest has to be refunded. This could impact your long-term financial goals if not managed wisely.  10. Importance of CPF Nomination Planning for unfortunate events is a crucial but often overlooked aspect of financial planning. CPF Nomination allows you to specify beneficiaries who will receive your CPF savings upon your demise. This ensures that your hard-earned money is distributed according to your wishes, giving you peace of mind. Conclusion: The Holistic Approach to CPF in Singapore

Understanding the intricacies of CPF and how it fits into your broader financial planning is crucial for a secure future in Singapore. From making informed decisions about CPFIS and Singapore Treasury Bills to utilizing SRS and understanding tax benefits, CPF offers myriad options for wealth accumulation and retirement planning. Your CPF account is more than just a mandatory savings scheme; when utilized wisely, it can be a powerful financial tool. Introduction: The Necessity of CPF in Singapore Central Provident Fund (CPF) isn't just a mandatory savings scheme; it is the financial backbone of every Singaporean citizen. With rising living costs and uncertainties surrounding retirement, understanding CPF is not just useful—it's crucial. This article aims to dissect the CPF in a way that helps you make the most of this unique social security system. 1. What is CPF? The Central Provident Fund (CPF) is a mandatory social security savings scheme funded by contributions from employers and employees in Singapore. The objective is to provide financial security during retirement. While it is often perceived as complicated, understanding the nuances of CPF can significantly benefit your long-term financial planning.  CPF Contribution Rates 2023 (from Seedly) 2. Three Main Accounts in CPF The Central Provident Fund (CPF) in Singapore is a compulsory savings scheme for all working citizens and permanent residents. It comprises three main accounts: Ordinary Account (OA), Special Account (SA), and Medisave Account (MA). Ordinary Account (OA) The OA is the most flexible of the three accounts, and it is primarily used for housing and education needs. Employers and employees contribute equally to the OA, and the interest rate is typically higher than the other two accounts. However, there are some restrictions on withdrawals from the OA, such as a minimum age requirement for buying a home. Special Account (SA) The SA is designed for retirement savings. Employers and employees contribute to the SA at a lower rate than the OA, but the interest rate is also higher. Withdrawals from the SA are generally only allowed for retirement purposes, such as buying a retirement property or paying for long-term care. Medisave Account (MA) The MA is used to pay for healthcare expenses. Employers and employees contribute to the MA at a fixed rate, and the interest rate is lower than the other two accounts. Withdrawals from the MA are allowed for a wide range of healthcare expenses, including hospital bills, outpatient treatments, and preventive care. Each CPF account has its own unique interest rate and withdrawal limitations. It is important to understand the different features of each account so that you can make informed decisions about how to manage your CPF savings. For example, if you are planning to buy a home in the near future, you may want to focus on building up your OA savings. If you are saving for retirement, you should focus on maximizing your contributions to the SA. And if you have significant healthcare expenses, you should make sure that you have enough savings in your MA.  3. The Importance of Voluntary Contributions Beyond mandatory contributions, individuals can make voluntary contributions to their CPF accounts. This is especially beneficial if you're self-employed or wish to enhance your retirement funds. Voluntary contributions are tax-deductible, providing dual benefits of increased savings and reduced tax liability. 4. Investing through CPFIS The CPF Investment Scheme (CPFIS) allows you to invest your CPF funds in various instruments like shares, bonds, and unit trusts. This provides a means to potentially earn higher returns compared to the standard CPF interest rates, though it comes with associated risks. 5. The Role of Singapore Treasury Bills Singapore Treasury Bills (T-bills) are a low-risk, short-term investment option that can be used to grow your CPF savings. T-bills are issued by the Singapore Government and are backed by its full faith and credit, making them one of the safest investments available. T-bills typically have maturities of less than one year, which means that investors can lock in a return for a relatively short period of time. T-bills are also very liquid, meaning that investors can easily sell them before maturity if needed. To invest in T-bills using your CPF savings, you must be a member of the Central Provident Fund (CPF) and have at least S$1,000 in your Ordinary Account (OA). You can apply for T-bills at primary auctions held by the Monetary Authority of Singapore (MAS). When you invest in T-bills, you are essentially lending money to the Singapore Government. In return, you receive a fixed interest payment at maturity. The interest rate on T-bills is determined at auction and is typically higher than the interest rate you would earn on your CPF savings in your OA. T-bills can be a good way to increase your CPF savings without taking on too much risk. They are a good option for investors who are looking for a safe and liquid investment with a relatively high return. Here are some of the key benefits of investing in T-bills using your CPF savings:

6. Retirement Schemes: CPF LIFE CPF LIFE (Lifelong Income for the Elderly) is a national annuity scheme that provides a guaranteed monthly payout for life, regardless of how long you live. This makes it a cornerstone in retirement planning, as it can provide peace of mind knowing that you will have a steady stream of income to support your needs, no matter how long your retirement lasts. There are several key benefits to opting for CPF LIFE:

7. Supplementary Retirement Scheme (SRS) The Supplementary Retirement Scheme (SRS) is a voluntary savings program that complements the CPF. Contributions to SRS are eligible for tax relief, making it another excellent avenue for retirement savings for Singaporeans. 8. Housing and CPF Using CPF for housing is common in Singapore. However, it's important to understand the impact of utilizing CPF funds for property, as it reduces the amount available for retirement. It's essential to strike a balance between housing needs and retirement planning. 9. Tax Benefits and CPF CPF contributions come with a significant tax relief that can greatly enhance your personal finance strategy. For example, contributions to the Medisave Account are tax-deductible, which means that you can reduce your overall taxable income by the amount of your contributions. This can lead to a lower tax bill and more money in your pocket. In addition to the tax relief on Medisave contributions, there are also tax reliefs available for voluntary contributions to the Special Account and Retirement Account. These tax reliefs can be claimed up to a certain limit each year. By understanding the tax benefits of CPF contributions, you can make informed decisions about how to save for your future. For example, you may want to consider increasing your Medisave contributions to reduce your tax bill and save for your healthcare needs. You may also want to consider making voluntary contributions to the Special Account or Retirement Account to save for your retirement. Here are some specific examples of how you can use CPF contributions to enhance your personal finance strategy:

10. CPF Nomination Scheme The CPF Nomination Scheme allows you to specify beneficiaries for your CPF savings in the event of your demise. It’s a critical aspect often overlooked but highly essential to ensure your funds are distributed according to your wishes. Conclusion: Plan, Invest, Retire in SingaporeUnderstanding CPF is pivotal for sound financial planning, especially in the Singaporean context. From investment options like Singapore Treasury Bills to understanding the intricacies of housing and retirement schemes, CPF serves as an all-encompassing tool for financial security. So, familiarize yourself with these ten crucial points, make informed decisions, and secure your financial future in Singapore.

IntroductionHi everyone, welcome back to The Investing Iguana, where we talk about all things related to money, savings, and investments. I'm your host, Iggy, and today were going to discuss a very important topic that affects many Singaporeans: the changes to the monthly CPF ceiling. If you're not familiar with CPF, it stands for Central Provident Fund, which is a compulsory savings scheme for all working Singaporeans and permanent residents. CPF helps you save for your retirement, healthcare, housing, and education needs. Every month, a portion of your salary goes into your CPF account, and your employer also contributes a matching amount. You can use your CPF savings to buy a home, pay for medical bills, invest in various schemes, or withdraw them when you reach the retirement age.  CPF Monthly Salary Ceiling to be Increased to S$8,000 by 2026But how much of your salary goes into your CPF account? Well, that depends on two factors: your age and the CPF monthly salary ceiling. The CPF monthly salary ceiling is the maximum amount of your monthly salary that is subject to CPF contributions. For example, if the CPF monthly salary ceiling is S$6,000 and you earn S$7,000 a month, you only contribute CPF on the first S$6,000 of your salary. The remaining S$1,000 is not subject to CPF contributions. So why does the CPF monthly salary ceiling matter? Well, it affects how much you can save for your future needs through CPF. The higher the CPF monthly salary ceiling, the more you can save in your CPF account. The lower the CPF monthly salary ceiling, the less you can save in your CPF account. Now, here’s the big news: the CPF monthly salary ceiling is going to change soon. In fact, it’s going to increase gradually from S$6,000 to S$8,000 by 2026. This means that more of your salary will be subject to CPF contributions in the coming years. This is part of the government’s plan to help Singaporeans save more for their retirement and other long-term needs. How to Make the Most of Your CPF Savings But what does this mean for you? How will this affect your take-home pay and your CPF savings? Well, that’s what we’re going to find out in this video. We’ll look at how the changes to the CPF monthly salary ceiling will impact different income groups and age groups. We’ll also look at some of the benefits and drawbacks of having a higher CPF monthly salary ceiling. And finally, we’ll give you some tips on how to make the most of your CPF savings and investments. How the CPF monthly salary ceiling affects low-income earnersHow will the changes to the CPF monthly salary ceiling affect different income groups? The changes to the CPF monthly salary ceiling will affect different income groups differently. Basically, there are three income groups that we can consider: low-income earners, middle-income earners, and high-income earners. Low-income earners Low-income earners are those who earn less than or equal to the current CPF monthly salary ceiling of S$6,000. For this group, the changes to the CPF monthly salary ceiling will have no impact on their take-home pay or their CPF savings. They will continue to contribute 20% of their salary to their Ordinary Account (OA), up to the current CPF monthly salary ceiling of S$6,000. Their employers will also continue to match their contributions dollar-for-dollar. So if you’re a low-income earner, you don’t have to worry about any changes to your take-home pay or your CPF savings. You can continue to enjoy the benefits of having a compulsory savings scheme that helps you save for your future needs.  Middle-income earnersMiddle-income earners are those who earn more than the current CPF monthly salary ceiling of S$6,000 but less than or equal to the new CPF monthly salary ceiling of S$8,000 by 2026. For this group, the changes to the CPF monthly salary ceiling will have some impact on their take-home pay and their CPF savings. They will have to contribute more of their salary to their OA in the coming years as the CPF monthly salary ceiling increases gradually. For example, let’s say you’re a middle-income earner who earns S$7,000 a month. Currently, you only contribute 20% of S$6,000 (which is S$1,200) to your OA every month. Your employer also contributes another S$1,200 to your OA every month. The remaining S$1,000 of your salary is not subject to CPF contributions. However, from September 2023 onwards, you will have to contribute 20% of S$6,300 (which is S$1,260) to your OA every month. Your employer will also contribute another S$1,260 to your OA every month. The remaining S$740 of your salary will not be subject to CPF contributions. This means that your take-home pay will decrease by S$60 every month from September 2023 onwards. However, your CPF savings will increase by S$120 every month from September 2023 onwards. Similarly, from September 2024 onwards, you will have to contribute 20% of S$6,600 (which is S$1,320) to your OA every month. Your employer will also contribute another S$1,320 to your OA every month. The remaining S$480 of your salary will not be subject to CPF contributions. This means that your take-home pay will decrease by another S$60 every month from September 2024 onwards. However, your CPF savings will increase by another S$120 every month from September 2024 onwards. And so on, until September 2026, when you will have to contribute 20% of S$8,000 (which is S$1,600) to your OA every month. Your employer will also contribute another S$1,600 to your OA every month. The remaining S$0 of your salary will be subject to CPF contributions. This means that your take-home pay will decrease by a total of S$400 every month from September 2026 onwards. However, your CPF savings will increase by a total of S$800 every month from September 2026 onwards. So if you’re a middle-income earner, you have to be prepared for some changes to your take-home pay and your CPF savings in the coming years. You will have less cash in hand every month, but you will have more savings in your CPF account. High-income earnersHigh-income earners are those who earn more than the new CPF monthly salary ceiling of S$8,000 by 2026. For this group, the changes to the CPF monthly salary ceiling will have no impact on their take-home pay or their CPF savings. They will continue to contribute 20% of their salary to their OA, up to the new CPF monthly salary ceiling of S$8,000 by 2026. Their employers will also continue to match their contributions dollar-for-dollar. So if you’re a high-income earner, you don’t have to worry about any changes to your take-home pay or your CPF savings. You can continue to enjoy the benefits of having a compulsory savings scheme that helps you save for your future needs.  CPF Income Ceiling: What Does It Mean for Youths?Experts agree that the changes to the CPF monthly income ceiling may not seem relevant to most youths now, as the average salary for people between the ages of 20 and 34 is between S$4,446 and S$5,792. However, they argue that raising the income ceiling now is still beneficial for youths, as it allows them to start saving more for their future. When the income ceiling is raised, it means that a larger portion of their salary will be contributed to their CPF. This means that they will have more money saved up for retirement, a home, and other expenses. Additionally, a higher income ceiling can help youths to boost their Special and MediSave accounts, which can be used to pay for medical expenses and other healthcare needs. In short, raising the CPF income ceiling is a form of future-proofing for youths. It allows them to start saving more money now, so that they will be better prepared for their future financial needs. How will the changes to the CPF monthly salary ceiling affect different age groups?The changes to the CPF monthly salary ceiling will affect different age groups differently. Basically, there are four age groups that we can consider: below 35 years old, 35 to 45 years old, 45 to 55 years old, and above 55 years old. Below 35 years old If you’re below 35 years old, the changes to the CPF monthly salary ceiling will have a positive impact on your long-term CPF savings. You will be able to save more for your retirement and other needs through CPF in the coming years. You will also have more time to grow your CPF savings through compound interest and investments. However, you may also face some challenges in managing your cash flow and budgeting in the short term. You may have less disposable income every month as more of your salary goes into your CPF account. You may also have less flexibility in using your CPF savings for other purposes such as buying a home or paying for education. Therefore, if you’re below 35 years old, you should plan ahead and adjust your spending habits accordingly. You should also make use of the various schemes and grants that are available to help you achieve your financial goals with CPF. 35 to 45 years old.If you’re between 35 and 45 years old, the changes to the CPF monthly salary ceiling will have a mixed impact on your long-term CPF savings. On one hand, you will be able to save more for your retirement and other needs through CPF in the coming years. On the other hand, you may not have enough time to grow your CPF savings through compound interest and investments. Moreover, you may also face some challenges in managing your cash flow and budgeting in the short term. You may have less disposable income every month as more of your salary goes into your CPF account. You may also have less flexibility in using your CPF savings for other purposes such as buying a home or paying for education. Therefore, if you’re between 35 and 45 years old, you should review your financial situation and goals regularly. You should also make use of the various schemes and grants that are available to help you achieve your financial goals with CPF. 45 to 55 years oldIf you’re between 45 and 55 years old, the changes to the CPF monthly salary ceiling will have a negative impact on your long-term CPF savings. You may not be able to save enough for your retirement and other needs through CPF in the coming years. You may also not have enough time to grow your CPF savings through compound interest and investments. Furthermore, you may also face some challenges in managing your cash flow and budgeting in the short term. You may have less disposable income every month as more of your salary goes into your CPF account. You may also have less flexibility in using your CPF savings for other purposes such as buying a home or paying for education. Therefore, if you’re between 45 and 55 years old, you should take action and boost your CPF savings as much as possible. You should also make use of the various schemes and grants that are available to help you achieve your financial goals with CPF.  Above 55 years old.If you’re above 55 years old, the changes to the CPF monthly salary ceiling will have no impact on your long-term CPF savings. You have already reached the retirement age and can withdraw your CPF savings at any time. You can also choose to leave your CPF savings in your account and earn interest on them. However, you may still want to consider how the changes to the CPF monthly salary ceiling will affect your future income and expenses. You may want to plan ahead and decide how much you need to withdraw from your CPF account and how much you want to leave behind. You may also want to explore the various options and schemes that are available to help you manage your retirement income and healthcare costs. Therefore, if you’re above 55 years old, you should review your retirement plan and budget regularly. You should also make use of the various schemes and grants that are available to help you achieve your financial goals with CPF. How can you make the most of your CPF savings and investments?Regardless of how you feel about the changes to the CPF monthly salary ceiling, you should always try to make the most of your CPF savings and investments. Here are some tips on how to do that: a. Start saving early and save consistently. The earlier you start saving, the more time you have to grow your CPF savings through compound interest and investments. The more consistently you save, the more stable and secure your CPF savings will be. b. Transfer excess funds from your OA to your Special Account (SA) or Retirement Account (RA). Your SA and RA earn higher interest rates than your OA (up to 6% per annum). By transferring excess funds from your OA to your SA or RA, you can boost your retirement savings and enjoy higher returns. c. Top up your own or your loved ones’ CPF accounts with cash or voluntary contributions. By topping up your own or your loved ones’ CPF accounts, you can increase your retirement savings and enjoy tax relief (up to S$14,000 per year). You can also help your loved ones achieve their financial goals with CPF. d. Invest wisely and diversify your portfolio. By investing wisely, you can grow your CPF savings faster and achieve higher returns. By diversifying your portfolio, you can reduce your risk exposure and balance out your gains and losses. e. Plan ahead and review regularly. By planning ahead, you can set realistic and achievable financial goals with CPF. By reviewing regularly, you can monitor your progress and make adjustments if necessary. ConclusionWe hope you enjoyed this article and video and learned something new. If you did, please give us a ‘Like’ to show your appreciation. It helps us know what kind of content you find useful and valuable. And if you haven’t already, please subscribe! Here at ‘The Investing Iguana’, we’re passionate about helping you achieve your financial goals with ease and peace of mind. And we have a lot more to share with you!

Stay tuned for our upcoming articles and videos, where we’ll explore other important financial topics like how to use CPF and SRS to boost your retirement savings, how to invest wisely and safely in the stock market, and how to make your money grow faster and smarter! We’re so grateful to have you as part of our ‘Investing Iguana’ family. Your support enables us to keep creating free content like this. Remember, every ‘like’, ‘share’, and ‘subscribe’ makes a difference! Thanks for watching today. Keep investing, keep learning, and we’ll see you in the next video. Take care! IntroductionHi everyone, welcome back to The Investing Iguana, where we talk about all things related to money and finance in Singapore. I'm your host, Iggy, and today were going to discuss a hot topic that has been making headlines recently: the Majulah Package. The Majulah Package is a new support package announced by Prime Minister Lee Hsien Loong at the National Day Rally on Sunday. It is aimed at boosting the retirement adequacy of lower and middle-income Singaporeans aged 50 and above this year. It will cover young seniors in their 50s and early 60s, as well as those of the Merdeka Generation and the Pioneer Generation. But what exactly is the Majulah Package, and how will it benefit you or your loved ones? In this video, I will explain the 7 things you need to know about the Majulah Package, and why it is important for your financial planning. Fact 1: The Majulah Package has three componentsFact 1: The Majulah Package has three components: a yearly CPF bonus, a one-time CPF Retirement Savings Bonus, and a one-time MediSave bonus. The first component of the package is the Earn and Save Bonus. Lower- and middle-income workers can get a CPF bonus of between $400 and $1,000 yearly as long as they remain in the workforce, whether full- or part-time. This bonus will be credited into their CPF account, on top of the usual employer and employee contributions. This means that you can grow your retirement savings faster by working longer. The second component of the package is the Retirement Savings Bonus. This is a one-time CPF bonus of between $1,000 and $1,500 for those who have not reached their Basic Retirement Sum (BRS). The BRS is the amount of savings you need in your CPF account when you reach 65 years old to receive a monthly payout for life under the CPF LIFE scheme. The Retirement Savings Bonus will help you top up your CPF account so that you can receive higher monthly payouts when you retire. The third component of the package is the MediSave Bonus. This is a one-time top-up of between $500 and $1,000 to your MediSave account. MediSave is a national medical savings scheme that helps you pay for your healthcare expenses, such as hospitalisation bills, outpatient treatments, and insurance premiums. The MediSave Bonus will give you more peace of mind when it comes to your healthcare needs. Fact 2: The Majulah Package is means-tested, so not everyone will receive the same amount of benefits Fact 2: The Majulah Package is means-tested, so not everyone will receive the same amount of benefits. The Majulah Package aims to offer additional support to those who are most in need. Accordingly, eligibility for its range of benefits will be determined by various factors such as income level, the annual value of one's residence, ownership of property, and CPF savings. Comprehensive information on the qualification criteria will be released in 2024. For instance, if you are someone with a lower income and fewer assets, you could gain up to an additional $12,000 in CPF savings, inclusive of interest, if you opt to work for another decade and retire at the age of 65. You can also qualify for a one-time Retirement Savings Bonus of up to $1,500 if you haven't met the Basic Retirement Sum (BRS). Additionally, a one-time MediSave Bonus of up to $1,000 will be available to you. Conversely, if you are on the higher end of the income spectrum and possess considerable wealth, you may not be eligible for any of the Majulah Package's benefits. This is because it is assumed that you already have adequate savings for retirement and sufficient healthcare coverage. Fact 3: The Majulah Package will benefit 1.4 million Singaporeans aged 50 and above in 2023 Fact 3: The Majulah Package will benefit 1.4 million Singaporeans aged 50 and above in 2023. The Majulah Package is designed to benefit individuals born in 1973 or earlier. This includes people in their early 50s to early 60s, as well as members of the Merdeka Generation born between 1950 and 1959, and the Pioneer Generation born before 1950. The package aims to assist more than 80% of Singaporeans within this age range. Regarding its financial implications, the Majulah Package is projected to have a lifetime cost of $7 billion. This substantial allocation by the government aims to enhance retirement security and healthcare provisions for older Singaporeans. Fact 4: The Majulah Package complements existing schemes for older Singaporeans Fact 4: The Majulah Package complements existing schemes for older Singaporeans. The Majulah Package is designed to work in harmony with existing support systems for older residents of Singapore, rather than replace or duplicate them. For instance, if you're part of the Merdeka Generation or Pioneer Generation, your existing benefits like MediSave top-ups, outpatient care subsidies, and premium subsidies for MediShield Life will remain unchanged. The Majulah Package enhances these benefits by offering supplementary contributions to your CPF and MediSave accounts, over and above what you already get. Likewise, if you're a younger senior qualified for other initiatives like the Workfare Income Supplement (WIS), Silver Support Scheme (SSS), or GST Voucher (GSTV), you will still receive these benefits. The Majulah Package steps in to augment your financial situation by giving you an extra layer of income and savings, in addition to what you already receive. Fact 5: The Majulah Package is part of the government’s long-term plan to prepare Singaporeans for an ageing population Fact 5: The Majulah Package is part of the government’s long-term plan to prepare Singaporeans for an ageing population. The Majulah Package is part of the government’s long-term plan to prepare Singaporeans for an ageing population. By 2030, one in four Singaporeans will be aged 65 and above. This means that there will be fewer working-age people to support the growing number of seniors. To address this challenge, the government has been implementing various measures to help Singaporeans live longer, healthier, and happier lives. These include enhancing healthcare services and infrastructure, promoting active ageing and lifelong learning, and strengthening social support networks. The Majulah Package is another step in this direction. It aims to encourage older Singaporeans to stay in the workforce longer, build up their retirement savings, and take care of their health. By doing so, they can enjoy a better quality of life in their golden years, and contribute to the nation’s progress. Fact 6: The Majulah Package reflects the government’s recognition and appreciation of older Singaporeans Fact 6: The Majulah Package reflects the government’s recognition and appreciation of older Singaporeans. The Majulah Package reflects the government’s recognition and appreciation of older Singaporeans. PM Lee said that the package is a way of saying “thank you” to the seniors who have contributed to Singapore’s development over the years. He also said that the package is a way of showing “solidarity” with the seniors who may face more difficulties in their later years. He urged younger Singaporeans to support their elders, and expressed his confidence that Singaporeans will overcome any challenges together as one people. The Majulah Package is thus a manifestation of the spirit of “Majulah”, which means “onward” or “forward” in Malay. It signifies the government’s commitment to help older Singaporeans move forward with dignity and confidence, and the nation’s aspiration to advance together as a united and resilient society. Fact 7: The Majulah Package is not yet finalised, and more details will be announced in 2024 Fact 7: The Majulah Package is not yet finalised, and more details will be announced in 2024. The Majulah Package is not yet finalised, and more details will be announced in 2024. PM Lee said that the government will consult widely with stakeholders and experts before finalising the package. He also said that the government will seek Parliament’s approval for the package before implementing it. This means that there may be some changes or refinements to the package before it is rolled out. Therefore, it is important to stay updated on the latest developments and announcements regarding the package. You can visit the CPF website or follow The Investing Iguana for more information and updates on the Majulah Package. And that wraps up our video on the 7 things you need to know about the Majulah Package. I hope you found this video informative and helpful. If you did, please give it a thumbs up and share it with your friends and family who may benefit from this package. Also, don’t forget to subscribe to our channel and hit the bell icon to get notified of our new videos. Thank you for watching The Investing Iguana, where we help you make smart financial decisions. I’m Iggy, signing off. See you in the next video!

|

Author🦖 Welcome to the Investing Iguana YouTube channel, your one-stop destination for all things related to investment tips, news, and advice! Our mission is to empower you with the knowledge and insights you need to make informed investment decisions and grow your wealth. With a perfect blend of engaging content, expert advice, and practical strategies, the Investing Iguana is here to guide you through the complex world of investing and help you achieve your financial goals. Archives

February 2024

Categories |

RSS Feed

RSS Feed