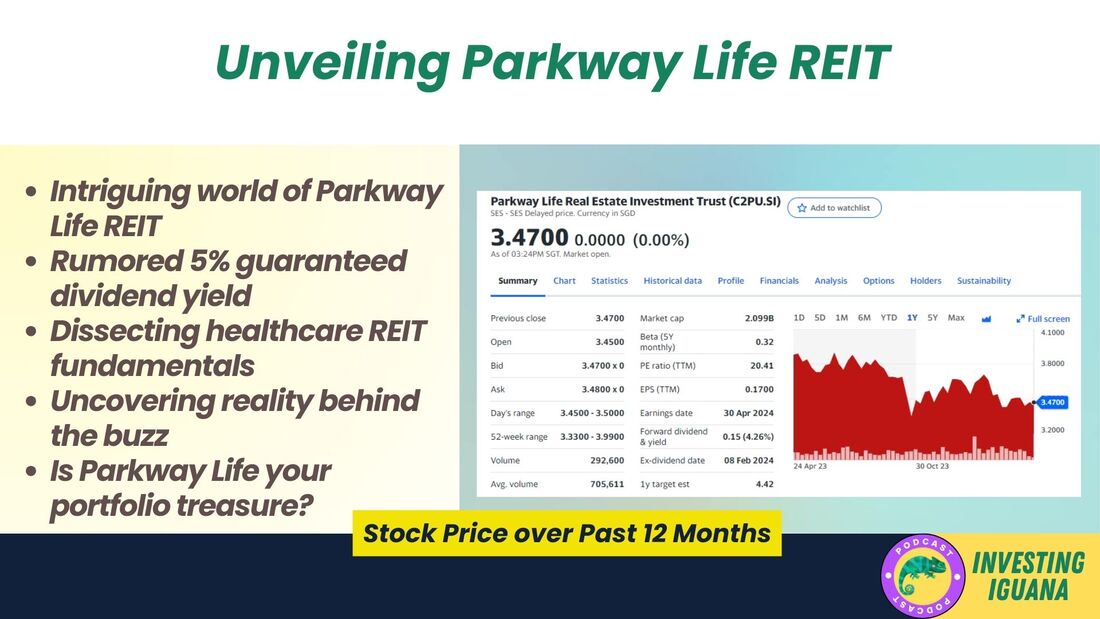

IntroductionWelcome, financial adventurers! It’s your guide, Iggy the Investing Iguana, ready to embark on another thrilling investment journey. The Investing Iguana is featured and ranked 8th in the "2023 Influential Tigers" by Tiger Brokers, with a total of 460,000 reads. Today’s destination? The intriguing world of Parkway Life reet! A place where a tantalizing 5% dividend yield is rumored to be guaranteed. Can it be true? Or is it just an investor’s mirage? Together, we’ll dissect the fundamentals of this healthcare reet and uncover the reality behind the buzz. By the end of our expedition, you’ll be equipped to decide if Parkway Life is the treasure you’ve been searching for in your investment portfolio. So, buckle up and let’s dive right in!  Parkway Life REIT: A Diverse InvestmentLet’s start by understanding what Parkway Life reet is. It’s a type of healthcare Real Estate Investment Trust (reet), which was introduced to the public in 2007. This means it’s been part of the investment landscape for over a decade, providing a way for investors to participate in the healthcare real estate market. Now, what makes Parkway Life reet stand out is its diverse portfolio of properties. It owns a total of 63 properties, spread across three different countries in Asia. This includes three hospitals located in Singapore, which is known for its world-class healthcare system. These hospitals not only provide essential healthcare services but also represent valuable real estate assets in a country where land is scarce. In addition to the hospitals in Singapore, Parkway Life reet also owns 59 nursing homes in Japan. Japan has one of the world’s oldest populations, which means there’s a high demand for nursing homes and other types of senior care facilities. By owning these properties, Parkway Life reet is well-positioned to benefit from this demographic trend. Last but not least, Parkway Life reet owns a specialist clinic in Malaysia. This adds another layer of diversification to its portfolio, both in terms of geography and the type of healthcare facility. So, when we talk about diversification in the context of Parkway Life reet, we’re referring to its wide range of properties spread across different countries and healthcare sectors. This diversification can help reduce risk and increase the potential for stable returns, making Parkway Life reet an interesting option for investors interested in the healthcare real estate sector.  Parkway Life REIT: A Standout InvestmentNow, let’s delve into the aspects that make Parkway Life reet particularly appealing. One of the standout features is the exceptional performance of its management team. They have consistently demonstrated their ability to enhance the Distribution Per Unit (DPU), a key metric for REITs that signifies the payout received by each unit holder. For those who may not be familiar with the terminology, think of DPU as the dividends in the world of stocks. What’s truly impressive about Parkway Life’s management is their ability to grow the DPU without resorting to unit dilution. In the reet landscape, this is no small achievement. Unit dilution typically occurs when a reet issues additional units to raise capital for acquisitions or other purposes. While this can lead to growth in the short term, it can also result in a lower DPU because the same amount of income is distributed among a larger number of units. However, Parkway Life’s management has skillfully navigated this challenge. They’ve managed to expand and enhance the reet’s portfolio, thereby increasing the income generated by its properties, all while maintaining the same number of units. This means that the DPU has grown, benefiting all unit holders equally without diminishing the value of individual units. In the world of REITs, this ability to grow DPU without diluting units is a testament to the management’s strategic acumen and operational efficiency. It reflects a balance of growth and income generation, which is a key indicator of a well-managed reet. This remarkable feat is one of the many reasons why Parkway Life reet stands out in the healthcare real estate sector.  Parkway Life REIT: A Defensive PowerhouseAnother significant advantage of Parkway Life reet is its operation within a defensive industry. But what does this mean? A defensive industry refers to a sector of the economy that is generally more resistant to economic downturns. These industries provide essential services or products that people continue to need, regardless of the state of the economy. In the case of Parkway Life reet, this defensive industry is healthcare. Regardless of economic conditions, people will always require healthcare services. Hospitals, nursing homes, and specialist clinics – the types of properties owned by Parkway Life reet – are all essential facilities that continue to operate and generate income even during tough economic times. This characteristic of Parkway Life reet’s business model acts as a protective shield, much like a trusty umbrella during a rainstorm. Just as the umbrella keeps you dry, operating in a defensive industry helps to safeguard Parkway Life reet’s rental income. Even when the economic climate is challenging, the demand for healthcare services remains relatively stable, ensuring a steady flow of rental income from their properties. This stability is a significant benefit for investors. It provides a level of income security that is highly valued, especially during periods of economic uncertainty. It’s like having a steady hand guiding you through the storm, ensuring that you stay dry no matter what. This resilience to economic downturns is another reason why Parkway Life reet stands out as a robust investment option in the healthcare real estate sector.  Parkway Life REIT: A High-Yield InvestmentAnother aspect that adds to the appeal of Parkway Life reet is the high Weighted Average Lease Expiry (WALE) of its overall portfolio. WALE is a measure used by REITs to indicate the average time period in which all leases in a portfolio will expire. A high WALE is generally seen as a positive attribute because it means that the reet has long-term leases in place. This provides a stable and predictable stream of rental income, which is a key factor for investors seeking regular returns. In the case of Parkway Life reet, these long-term leases are not just a source of steady income, but they also have built-in protections against inflation. A significant percentage of these leases have Consumer Price Index (CPI)-linked revision formulas and rent review provisions incorporated into the tenancy contracts. This means that the rent can be adjusted upwards in line with inflation. This is a significant advantage as it allows Parkway Life reet to maintain its real income levels even in times of inflation, thereby protecting its bottom line. Furthermore, the management team at Parkway Life reet deserves special mention for their consistent efforts in generating yield-accretive capital recycling over the past 16 years. Capital recycling is a strategy used by REITs to sell off lower-yielding properties and reinvest the proceeds into higher-yielding ones. This strategy has been effectively employed by the management team at Parkway Life reet, demonstrating their clear strategic direction and effective execution. In essence, the high WALE, inflation-protected leases, and effective capital recycling strategies all contribute to making Parkway Life reet a robust and well-managed investment option in the healthcare real estate sector. These factors, combined with the defensive nature of the healthcare industry, make Parkway Life reet an attractive proposition for investors seeking stable returns and capital appreciation.  Parkway Life REIT: Navigating RisksIndeed, like any investment, Parkway Life reet is not without its potential downsides. One of the key risks to consider is foreign exchange risk. A significant portion of Parkway Life’s revenue is derived from its properties in Japan, and therefore, it is denominated in Japanese Yen. This exposes the reet to fluctuations in the exchange rate between the Japanese Yen and the currency in which the reet’s distributions are made. Foreign exchange risk, also known as FX risk, refers to the potential for loss due to changes in exchange rates. If the Japanese Yen were to depreciate against the distribution currency, the value of the revenue generated from the Japanese properties when converted back would decrease. This could potentially lead to lower distributions for unit holders. While the decision to expand into Japan was strategically sound from a demographic perspective, given the country’s aging population and the consequent demand for healthcare facilities, it does introduce this additional layer of FX risk. It’s an inevitable part of operating in multiple countries and dealing with different currencies. However, it’s worth noting that many REITs and multinational corporations manage foreign exchange risk through various hedging strategies. These can include the use of financial instruments like futures, options, and swaps to mitigate the potential impact of adverse currency movements. While these strategies can’t eliminate FX risk entirely, they can help to manage and reduce it.  Parkway Life REIT: FY 2023 PerformanceNow, let’s turn our attention to Parkway Life reet’s recent performance in the fiscal year 2023. The Distribution Per Unit (DPU), a key performance indicator for REITs, exhibited a healthy growth of 2.7% year-over-year. This growth was primarily driven by a robust increase in both gross revenue and net property income, indicating a strong operational performance. However, it’s important to note that this growth was partially offset by higher financing costs. Financing costs typically include interest payments on loans and other forms of debt, which are a common aspect of reet operations given the capital-intensive nature of real estate investments. Despite this, the net effect on Parkway Life reet’s performance was positive, demonstrating the reet’s ability to effectively manage its finances and generate growth. In addition to its strong financial performance, Parkway Life reet also made significant strategic moves during FY 2023. One of the most notable was a $350 million collaboration with IHH Healthcare Singapore. The aim of this collaboration is to transform Mount Elizabeth Hospital into a modern, integrated multi-service medical hub by 2025. This is a substantial investment that underscores Parkway Life reet’s commitment to enhancing its portfolio and staying at the forefront of healthcare real estate. This transformation of Mount Elizabeth Hospital represents a forward-looking strategy that could yield significant benefits in the long run. By creating a multi-service medical hub, Parkway Life reet is positioning itself to cater to a broader range of healthcare needs, thereby potentially attracting a larger patient base and generating higher revenues.  Parkway Life REIT: Navigating Currency ChallengesLooking into the future, there are several positive factors that could potentially boost Parkway Life reet’s performance. One of these is the completion of the acquisition of two additional nursing homes in 2023. These new properties are expected to start contributing to Parkway Life’s bottom line in the fiscal year 2024. This expansion of their portfolio not only increases their asset base but also enhances their income-generating potential, which is a positive sign for investors. Another favorable aspect is Parkway Life’s financial position. The reet has no refinancing requirements until March 2025. This is significant because it means that the reet has a stable financial footing for the next couple of years, without the need to refinance any of its debts. This stability is further enhanced by the expectation that interest rates will come back down by the time Parkway Life needs to refinance. This could help offset the higher interest rates they might experience in Japan and keep their overall cost of borrowing stable. This financial prudence and foresight is another testament to the strong management of Parkway Life reet. However, like any investment, Parkway Life reet is not without its challenges. One of these is the recent depreciation of the Japanese Yen against the Singapore Dollar. Given that a significant portion of Parkway Life’s revenue comes from Japan, this depreciation could potentially impact their distributions when converted back to Singapore Dollars. But it’s important to note that the management team at Parkway Life reet has taken proactive measures to mitigate this foreign exchange risk. They have put in place a foreign exchange (FX) hedging strategy, with forward positions until the first quarter of 2029. This strategy involves entering into contracts that lock in the exchange rate for a future date, thereby reducing the uncertainty and potential impact of future currency fluctuations.  A Balanced InvestmentSo, what’s the final takeaway? Parkway Life reet presents itself as a compelling investment opportunity, particularly for those who are seeking a stable dividend yield coupled with a high degree of capital preservation. This essentially means that investors can expect a regular and reliable income stream in the form of dividends, while also maintaining the value of their initial investment. Parkway Life reet’s robust portfolio, which spans across multiple countries and includes a diverse range of healthcare facilities, contributes to this stability. The long-term leases and built-in inflation protections further enhance the predictability of its income. Moreover, the reet operates in the defensive healthcare industry, which tends to remain resilient even during economic downturns. All these factors combine to provide a degree of income stability and capital preservation that is highly sought after by investors. However, like any investment, Parkway Life reet does come with its share of risks. The most notable among these is the foreign exchange risk arising from its operations in Japan. Fluctuations in the exchange rate between the Japanese Yen and the Singapore Dollar could potentially impact the reet’s distributions. But it’s important to note that the management team has proactively addressed this risk by implementing a foreign exchange hedging strategy, thereby demonstrating their commitment to protecting the interests of the unit holders. Speaking of the management team, they have consistently shown a strong track record of performance. They have successfully grown the Distribution Per Unit (DPU) without diluting the units, which is a remarkable achievement in the reet landscape. Their strategic vision for the future, including the transformation of Mount Elizabeth Hospital into a multi-service medical hub and the acquisition of additional nursing homes, indicates a clear path towards continued growth and success. Parkway Life REIT: A Hidden Gem?So, is Parkway Life reet a hidden gem or a too-good-to-be-true investment? While nothing in the market is ever truly guaranteed, Parkway Life's strong track record, defensive qualities, and growth plans make it a compelling option for income investors.

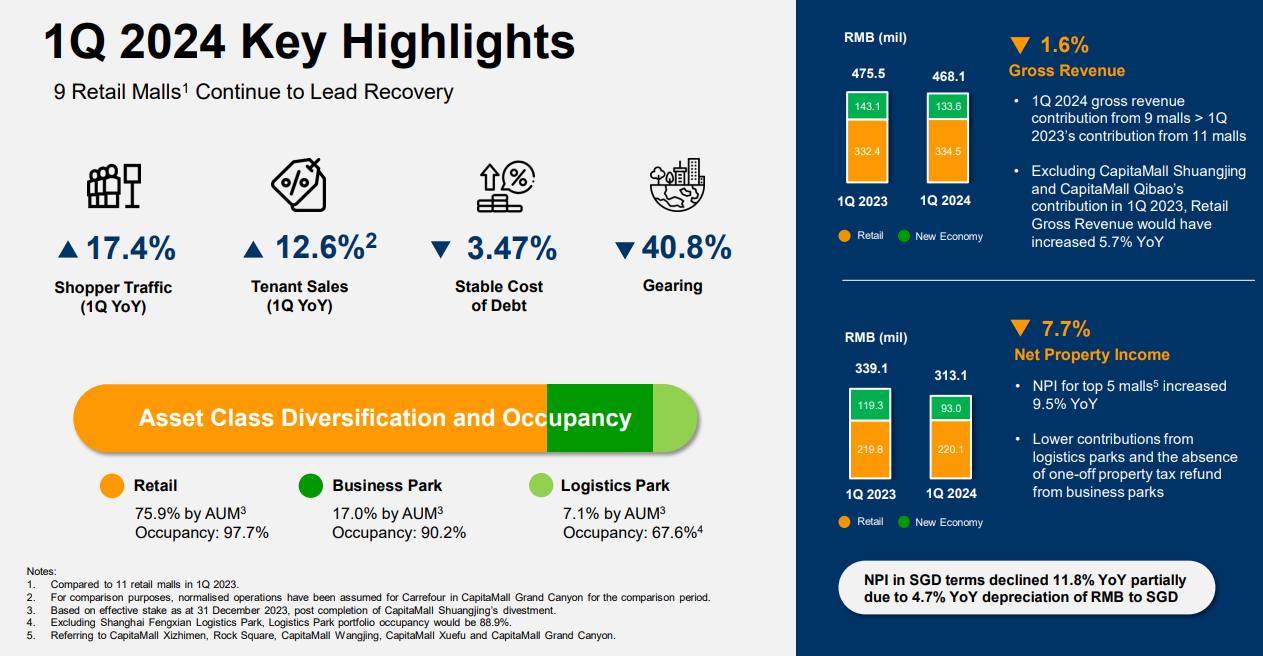

As always, do your own research before diving in. But if you're looking for a reliable dividend payer with recession-resistant properties, Parkway Life is definitely worth a closer look. If you found this analysis helpful, smash that like button and subscribe to The Investing Iguana for more insights to help you navigate the wild world of investing. Stay tuned for my next video, where I'll be sharing my top 5 REITs for 2024. Trust me, you won't want to miss it! Until then, stay curious, stay invested, and stay awesome! Iggy out. IntroductionHey there, Investing Iguanas! Iggy here with a quick rundown of CapitaLand China Trust's first quarter business updates. Let's dive in and see what's been cooking in the world of retail and real estate! I will start by giving my overall summary, and then I will deep dive and decode their 8 key slides. Let's go! CapitaLand China Trust has seen some mixed results this quarter. On the bright side, retail mods are experiencing significant growth, with shopper traffic up 17.4% and tenant sales rising 12.6% year on year. That's a pretty impressive feat, considering the challenges faced by the retail industry. The company has also managed to reduce its gearing from 42.3% in September 2023 to 40.8% in March 2024, showing a positive trend in financial management. However, it's not all sunshine and rainbows. The largest logistics park lost a tenant due to business closure, resulting in a 0% occupancy rate. Ouch! Additionally, revenue dropped by $9.3 million for the new economy site, likely due to the bankruptcy of a major tenant. Despite these setbacks, retail gross revenue increased by 5.7% year on year, even after selling two malls. But here's the catch: net property income (NPI) decreased by 7.7%, and when considering SGD terms, it further dropped to 11.8%.  CapitaLand China Trust Operational UpdateOperationally, retail occupancy remains strong at 97.7%, indicating high demand for CapitaLand China Trust's retail properties. However, business parks are facing challenges with a 90.2% occupancy rate, as weak business sentiments and new supply put pressure on the sector. Management has taken steps to mitigate risks, such as converting SGD-denominated debt to RMB-denominated debt and maintaining an adjusted income coverage ratio of 3x. However, it's not all sunshine and rainbows. The largest logistics park lost a tenant due to business closure, resulting in a 0% occupancy rate. Ouch! Additionally, revenue dropped by $9.3 million for the new economy site, likely due to the bankruptcy of a major tenant. Despite these setbacks, retail gross revenue increased by 5.7% year on year, even after selling two malls. But here's the catch: net property income (NPI) decreased by 7.7%, and when considering SGD terms, it further dropped to 11.8%. Operationally, retail occupancy remains strong at 97.7%, indicating high demand for CapitaLand China Trust's retail properties. However, business parks are facing challenges with a 90.2% occupancy rate, as weak business sentiments and new supply put pressure on the sector. Management has taken steps to mitigate risks, such as converting SGD-denominated debt to RMB-denominated debt and maintaining an adjusted income coverage ratio of 3x. Shopper trends show double-digit growth in various sectors, including entertainment (12.6%) and supermarkets (14.2%). While retail occupancy slightly decreased, the majority of properties remain above 95% occupancy. Looking ahead, 40.3% of the retail portfolio leases are up for renegotiation, which could potentially impact rental rates. Business and logistic parks are also facing softer leasing demand and increased competition from new supply. In the broader context, China's economy grew by 5.3%, showing resilience in industrial activities. However, uncertainty regarding land lease renewals in the future may affect investors' confidence in the long run.  Slide 1: CLCT Q1 2024 Performance SnapshotThe image focuses on the performance of CLCT's retail malls segment, which seems to be leading the recovery. Shopper traffic increased by a solid 17.4% year-over-year, indicating a rebound in consumer demand. Tenant sales also grew by an impressive 12.6%, reflecting improved spending. On the financial front, the company managed to keep its cost of debt stable at 3.47%, suggesting effective financing management. Even better, the gearing or debt-to-asset ratio decreased by a massive 40.8%, signaling reduced leverage. CLCT's asset portfolio is well-diversified across retail properties (75% of portfolio, 97.7% occupancy), business parks (17%, 90.2% occupancy), and logistics parks (7.1%, 67.6% occupancy). This diversification helps mitigate risks. Now, let's look at the numbers. CLCT's gross revenue for the first quarter of 2024 was S$468.1 million, a 1.6% increase from the previous year. This growth was driven mainly by the strong performance of the retail malls, offsetting weaker contributions from other segments. The net property income, a key profitability metric, stood at S$313.1 million, down 7.7% year-over-year. This decline was attributed to lower contributions from logistics parks and the absence of income from business parks. Overall, CLCT seems to be on a solid recovery path, with its retail malls leading the charge. The management's focus on debt reduction and portfolio diversification also bodes well for long-term sustainability.  Slide 2: CapitaLand China Trust Q1 2024 UpdatesLooking at the operational updates for CapitaLand China Trust in Q1 2024, there are some positive signs amidst the challenges. Their retail performance got a boost from asset enhancement initiatives completed in 2023 at malls like Rock Square and CapitaMall Yuhuating. This helped the retail occupancy rate stay high at 97.7%, above market levels. Shopper traffic also saw a solid 17.4% year-on-year increase in Q1, indicating consumer demand is recovering well post-COVID. The business park segment maintained a stable 90.2% occupancy despite new supply entering the market. Their tailored leasing strategies for each asset seem to be working in attracting suitable tenants. In the logistics parks division, they successfully secured leases with key tenants at parks like Kunshan Bacheng and Wuhan Yangluo. Rental rates were also aligned with market conditions to stay competitive. Overall, CapitaLand China Trust appears to be navigating the challenges well by leveraging their diversified portfolio and proactive asset management strategies. Their focus on the resilient 'new economy' sectors like e-commerce and technology is a smart move. I'll continue monitoring their performance, but the Q1 updates give reasons for cautious optimism about their prospects.  Slide 3: CapitaLand China Trust Financial HealthThe slide paints a picture of a healthy financial standing. As of March 31, 2024, the trust's total debt stood at a manageable $1.86 billion, with a gearing ratio of 40.8%. This suggests a prudent approach to leverage, providing a comfortable buffer for investors. Additionally, the interest coverage ratio of 3.2x indicates a strong ability to service its debt obligations. One notable aspect is the impact of interest rate movements on the trust's distribution. The slide outlines how a 50 basis point increase in interest rates could potentially reduce the distribution per unit by 0.9 cents for SGD loans, while a 50 basis point decrease could boost it by 1.0 cent for RMB loans. This information is crucial for investors to understand the trust's sensitivity to interest rate fluctuations and how it may affect their returns. Overall, CapitaLand China Trust's financial position appears robust, with a diversified portfolio of retail, business park, and logistics properties across China. However, investors should keep a close eye on factors such as currency fluctuations, interest rate movements, and the overall economic conditions in China, as these could impact the trust's performance. As always, conducting thorough research and aligning investments with your risk appetite is key to successful investing.  Slide 4: CapitaLand China Trust Debt StructureThis slide provides a comprehensive overview of the trust's debt structure, highlighting its impressive ability to manage its financial obligations without the need for refinancing until 2025. The key takeaway is the trust's proactive debt management approach, where it has strategically termed out its RMB loans at a lower interest rate, ensuring a more favorable financing cost in the coming fiscal year. Additionally, the trust's debt portfolio is well-balanced, with a mix of RMB-denominated debt (23%), SGD-denominated debt (77%), and a combination of fixed-rate (75%) and floating-rate (25%) instruments, which helps mitigate interest rate risks. Furthermore, the trust has managed to increase its RMB-denominated facilities from 20% in December 2023 to 23% by March 2024, demonstrating its ability to access local currency funding and optimize its capital structure. Notably, the trust has also increased its sustainability-linked loans, which now account for 36% of its total loans, aligning with the growing emphasis on sustainable financing and responsible investing practices. Overall, CapitaLand China Trust's well-staggered maturity profile and proactive debt management strategies position it favorably to navigate potential market volatility and capitalize on growth opportunities in the Chinese real estate market.  Slide 5: CapitaLand China Trust Portfolio DiversificationThe key highlight is CapitaLand China Trust's focus on enhancing portfolio stability through broader diversification. This approach reduces exposure to tenant concentration risks. The retail segment dominates at 70.4%, followed by a well-diversified business park segment at 26.8%. Within business parks, the portfolio spans electronics, engineering, IT, biomedical sciences and other trades. This diversification strategy strengthens CapitaLand China Trust's resilience by minimizing overdependence on any single tenant or industry. A prudent move, especially in today's volatile market conditions. The data also shows the trust increasing its exposure to specialty retail and services, indicating proactive portfolio management. From an investor's lens, CapitaLand China Trust's diversified approach to portfolio construction aligns with our principles of mitigating risks and pursuing long-term sustainability.  Slide 6: CapitaLand China Trust Q1 2024 LeasingFrom the slide, we can see that CapitaLand China Trust had a healthy retail retention rate of 60.9% for renewed leases in Q1 2024. This is a significant improvement from 35.4% in the previous quarter, indicating better tenant retention and stable occupancy rates. Additionally, the majority of malls recorded positive rental reversions, suggesting the reet's ability to negotiate favorable lease terms. The slide also highlights CapitaLand China Trust's increased exposure in targeted sectors generating higher sales. The Food & Beverages category takes the largest share at 43.5%, followed by Leisure & Entertainment at 11.7%, and Fashion & Accessories at 11.2%. These sectors are likely benefiting from the post-pandemic recovery in consumer spending as people return to physical retail spaces. Overall, the portfolio's occupancy cost appears to be within a sustainable range of high teens to low 20%, indicating prudent management of operating expenses.  Slide 7: CapitaLand China Trust Strategy OverviewFrom the slide, we can see that CapitaLand China Trust has a well-diversified portfolio, with a significant chunk of its assets allocated to business parks, contributing a solid 17% to their overall portfolio. Now, this diversification is key because it helps mitigate risk and ensures a steady stream of income, even if one sector experiences a downturn. But wait, there's more! The slide also highlights CapitaLand's proactive approach to tenant engagement and customized leasing solutions. They're not just sitting back and waiting for tenants to come knocking – they're actively pursuing them, both globally and domestically, to expand their client base. Talk about hustle! And let's not forget about their asset-specific leasing strategy. CapitaLand is implementing customized leasing approaches to capture demand from tenants in their Ascendas Xinsu portfolio. This includes targeting international and domestic tenants, securing renewals, and retaining tenants poised for robust growth in sectors like electronics and engineering. It's clear that CapitaLand China Trust is playing the long game here. They're not just focused on short-term gains but are positioning themselves for long-term success by diversifying their portfolio, actively engaging with tenants, and adapting their strategies to capture emerging market trends.  Slide 8: CapitaLand China Trust Logistics ChallengesNow, while the logistics segment only makes up 7.1% of the portfolio, there are some concerning trends we need to discuss. The occupancy rates for their Grade A logistics facilities in Shanghai and Kunshan have taken a hit, dropping to 82% and 80% respectively. This decline can likely be attributed to the challenging macro environment in China, with supply chain disruptions from the zero-COVID policy impacting economic activity and tenant operations. To address this, CapitaLand China Trust is implementing customized leasing strategies like adjusting rents to retain existing tenants and attract new ones. They're also leveraging their properties' proximity to major transportation hubs as a selling point. However, with increased market supply and softening demand, maintaining healthy occupancies and rental rates will be an uphill battle in the near-term. While the logistics segment is a relatively small part of the portfolio, its performance could serve as an early indicator of broader economic headwinds impacting CapitaLand China Trust's other operating segments. As investors, we'll want to keep a close eye on how management navigates these challenges and pivots their strategies accordingly. Staying invested for the long haul requires carefully evaluating both the risks and opportunities at play. CapitaLand China Trust Q1 FY24 SnapshotAlright, Investing Iguanas, that wraps up our analysis of CapitaLand China Trust's Q1 FY24 results. As we've seen, there are some bright spots, like the growth in retail mods and the reduction in gearing. But we can't ignore the challenges, such as the loss of a major tenant in the logistics park and the drop in revenue for the new economy site. It's crucial to keep a close eye on these developments and adjust our investment strategies accordingly.

If you found this video helpful, be sure to smash that like button and subscribe to the Investing Iguana channel for more financial insights and analysis. Remember, investing is a wild ride, but with the right knowledge and a bit of iguana intuition, we can navigate these markets together. Until next time, stay savvy, stay invested, and keep on iguana-ing! IntroductionHello, savvy investors and real estate enthusiasts! Welcome back to Investing Iguana, the channel where we dissect the complexities of the market and make investing more accessible to you. I'm Iggy, and today we're diving into a topic that's been hot on the lips of every Singaporean investor – the recent share price slide of Mapletree Pan Asia Commercial Trust, also known as MPACT. The Investing Iguana is featured and ranked 8th in the "2023 Influential Tigers" by Tiger Brokers.  MPACT's DPU Dip: Unveiling the Real Story

In the bustling realm of Singapore's real estate investment trusts (REITs), Mapletree Pan Asia Commercial Trust (MPACT) has recently unveiled its financial performance for the third quarter of the fiscal year 2023/2024, ending December 2023. In a surprising twist, the distribution per unit (DPU) took a slight dip to 2.20 Singapore cents from the previous year's 2.42 cents. This downturn has nudged MPACT's 9-month DPU down by 10.1% year-on-year, sparking curiosity and a bit of concern among investors. Why has this once stalwart of the Singapore reet sector seen a dip in its share price, despite a seemingly solid performance? Buckle up as we explore the real story behind MPACT's financial performance, what led to the dip, and what this means for investors like you. Stay tuned as we uncover the layers behind the numbers and what the future holds for MPACT.  MPACT's Share Price Fluctuation: Unpacking the Causes

Following the announcement of its earnings, MPACT’s share price experienced a brief surge of optimism. The price peaked at S$1.46, reflecting a positive reaction from the market. Investors, buoyed by the company’s performance, drove the price up in anticipation of continued growth and profitability. However, this surge was ephemeral, and the price soon wobbled back down to S$1.39 by the 9th of February 2024. This fluctuation in MPACT’s share price is not uncommon in the stock market. Prices are influenced by a myriad of factors, including the company’s earnings, economic indicators, and market sentiment. In this case, the initial optimism was likely driven by MPACT’s earnings announcement, which often provides investors with a snapshot of the company’s financial health. However, the subsequent drop in price suggests that investors may have reassessed their initial reactions. Perhaps they took a closer look at the earnings report and found some areas of concern, or maybe broader market trends influenced their decision to sell. Regardless of the reason, the drop in price serves as a reminder of the volatility inherent in the stock market.  MPACT's Distributions Squeeze: Analyzing the Causes

Let’s delve into the heart of the matter. The squeeze on distributions, a key concern for investors, was largely due to an increase in financial costs. These costs, which include interest payments on loans and other financial obligations, surged by 14.1%. This surge was primarily driven by rising interest rates, a global economic phenomenon that has a direct impact on the cost of borrowing. When interest rates rise, the cost of borrowing increases. This means that companies have to pay more to service their debts, which can put a squeeze on their profits. In this case, the rising interest rates nudged up the cost of borrowing for the company, leading to higher financial costs. Despite this financial hurdle, the company’s Net Property Income (NPI), a key measure of a real estate company’s operating performance, managed to record a modest increase of 1.7% year-over-year. This growth was largely thanks to the strong performance of the company’s operations in Singapore, as well as resilient earnings from Hong Kong and Japan. The strong performance in these markets helped to offset the impact of rising financial costs, allowing the company to maintain a positive growth trajectory. This demonstrates the company’s ability to navigate economic challenges and deliver solid results, a testament to its strategic acumen and operational efficiency.  MPACT's Occupancy & Leverage: Strategies for Success

The occupancy rates across MPACT’s portfolio have shown a positive trend, rising to 96.7% from 96.3%. This increase is a clear indication of the trust’s operational efficiency and its ability to attract and retain tenants. The full backfilling of mTower, bringing its occupancy rate to an impressive 98.6%, and Festival Walk maintaining its 100% occupancy, are noteworthy achievements that highlight the trust’s successful management strategies. However, there’s another aspect that requires attention - the leverage ratio. The leverage ratio, a measure of the company’s debt relative to its equity, has slightly increased to 40.8%, just above the previous figure of 40.7%. This increase might seem small, but in the world of finance, even small changes can have significant implications. In response to this, MPACT has taken strategic steps to mitigate the impact of rising interest rates, which can increase the cost of borrowing and thus affect the leverage ratio. One such step is swapping more of their Hong Kong Dollar (HKD) loans into Chinese Yuan (CNH). This could potentially offer more favorable interest rates, thereby reducing the cost of borrowing. Additionally, MPACT has increased the proportion of fixed-rate debt from 79.9% to 85.0%. Fixed-rate debt has the advantage of providing certainty about future payments, as the interest rate remains constant over the life of the loan. This can be particularly beneficial in a rising interest rate environment, as it shields the borrower from increasing costs. MPACT's Appealing Dividend Yield & Target Price

MPACT, with its current dividend yield around the appealing figure of 6.5%, has positioned itself as a compelling option for investors who are exploring opportunities in the Real Estate Investment Trust (reet) sector. The dividend yield is a financial ratio that shows how much a company returns to its shareholders in the form of dividends. A yield of 6.5% is considered attractive, indicating that MPACT is potentially a profitable investment. Analysts, who study market trends and use that information to predict future performance, also maintain a cautiously optimistic outlook for MPACT. They have set an average share price target at S$1.62. This target price is a projection of what analysts believe the stock will be worth at a specific future date. The projected price of S$1.62 suggests a potential uplift of 17% from the current share price. This means that if the company performs well and meets analysts’ expectations, investors could see a significant return on their investment. However, it’s important to note that these are projections and actual results may vary. Market conditions, economic factors, and company performance can all impact the actual share price. Therefore, while the outlook for MPACT is positive, investors should do their own research and consider their own financial goals and risk tolerance before making an investment decision. Investing in the stock market always carries risk, and it’s important to make informed decisions. ConclusionAnd there you have it, folks – a comprehensive breakdown of Mapletree Pan Asia Commercial Trust's recent financial journey and the reasons behind its share price movement. From the impact of higher financing costs to the strategies MPACT is employing to navigate these turbulent times, we've covered it all. If this deep dive has helped you gain a better understanding of MPACT's situation or sparked further interest in the reet sector, why not give this video a thumbs up? Your support encourages us to keep bringing you detailed analyses and insights into the investment world. Don't forget to subscribe to Investing Iguana for more in-depth looks into your favorite stocks and investment trends. Have thoughts, questions, or topics you'd like us to cover next? Drop a comment below – we're all about growing together in our investment journey. Until next time, stay informed, invest wisely, and see you in the next video!

Parkway Life REIT: 2024 Investment SpotlightHello, savvy investors of Singapore! It’s Iggy here from Investing Iguana. In today's video, 'Parkway Life REIT: Soaring High in 2024 – OCBC Analyst Insights,' we're diving into a detailed analysis of one of Asia's top healthcare REITs. Are you wondering what makes Parkway Life REIT stand out in the Singapore REIT market, especially going into 2024? I’m here to break down the latest OCBC analyst report, uncovering the key factors that are propelling Parkway Life REIT to new heights. We’ll explore the insights behind their impressive financial performance, strategic asset management, and what this all means for you as an investor. So, let's get started and discover why Parkway Life REIT is a name to watch in the coming year! Parkway Life REIT: A Robust Investment in 2024Parkway Life reet (SGX:C2PU) is indeed a significant player in the healthcare reet sector. Its expansive portfolio of 61 properties is not just a testament to its size but also a reflection of its strategic investments in high-quality healthcare assets. These properties include top-tier private hospitals in Singapore and Malaysia, and nursing homes spread across various prefectures in Japan. As of September 30, 2023, the total valuation of these assets was an impressive S$2.2 billion. This substantial footprint in the healthcare sector is particularly noteworthy in the context of Singapore and Asia, regions known for their rapidly aging populations and increasing demand for quality healthcare services. In 2023, despite facing a challenging macroeconomic environment characterized by uncertainties and volatilities, Parkway Life reet demonstrated remarkable resilience and strategic prowess. It managed to deliver impressive results, as highlighted in the report by Ada Lim from OCBC Investment. One of the key performance indicators of a reet is its Distribution Per Unit (DPU), which is essentially the income distribution to investors. Parkway Life reet saw a 2.8% increase in its DPU, rising from S$0.107 in the first nine months of 2022 (9M22) to S$0.1099 in the same period in 2023 (9M23). This growth, achieved in a challenging macroeconomic environment, underscores the reet’s robust operations and its ability to generate stable returns for its investors. Parkway Life REIT: Financial Health in 2024ndeed, the financial performance of Parkway Life reet in 2023 further underscores its robustness and growth potential. The reet’s gross revenue and net property income (NPI) saw a substantial rise of 24.6% and 26.2% respectively, reaching S$110.9 million and S$104.5 million in the first nine months of 2023 (9M23). These figures are not just mere numbers; they are strong indicators of the reet’s financial health and its ability to generate significant income from its healthcare assets. This growth in revenue and NPI is particularly impressive given the challenging economic environment, demonstrating the reet’s resilience and its strategic asset management capabilities. In the world of REITs, financial health is indeed key. A strong balance sheet is indicative of a reet’s ability to manage its debt levels effectively and its financial flexibility to pursue growth opportunities. Parkway Life reet’s balance sheet is a testament to its strong financial stewardship. It boasts a healthy gearing ratio of 36.0%, well within the regulatory limit, indicating a balanced approach to leveraging and risk management. Furthermore, the reet has an attractively low all-in cost of debt of just 1.32%, reflecting its ability to secure financing at competitive rates. This low cost of debt enhances the reet’s interest coverage ratio, providing a safety margin for distributions to unitholders. Driving Factors Behind Parkway Life REIT’s SuccessSo, what's driving this success? The success of Parkway Life reet can be attributed to a combination of strategic factors and prudent management practices, as highlighted in Ada Lim’s report. Firstly, the defensive nature of the healthcare sector plays a significant role. Healthcare is a critical service that remains in demand regardless of economic conditions. This characteristic makes investments in healthcare real estate, such as hospitals and nursing homes, relatively stable and resilient to economic downturns. Secondly, the well-structured master leases of Parkway Life reet’s properties provide a steady stream of rental income. These leases often include built-in rent escalations, which contribute to the growth of the reet’s income over time. Thirdly, prudent capital management is a key factor in the reet’s success. This involves maintaining a healthy balance sheet, managing debt levels effectively, and securing financing at competitive rates. As of September 30, 2023, Parkway Life reet had a healthy gearing ratio of 36.0% and a low all-in cost of debt of 1.32%, indicating strong financial stewardship. Lastly, the experienced management team at the helm of Parkway Life reet is instrumental in navigating the complexities of the healthcare real estate sector and driving the reet’s growth. Their expertise and strategic decision-making have been pivotal in the reet’s ability to deliver stable returns and sustain its growth trajectory. As of January 8, 2024, OCBC Investment Research set a target price of S$4.27 for Parkway Life reet. This target price reflects the research firm’s confidence in the reet’s ability to continue its growth trajectory and deliver value to its investors. It suggests that the research firm expects the reet’s market price to reach or exceed S$4.27 in the future, based on their analysis of the reet’s fundamentals and growth prospects. Iggy's Review of the OCBC ReportNow, let me dissect OCBC's report and give my take on how Parkway Life reet will dare for 2024. As one of Asia’s largest healthcare REITs, Parkway Life has been a beacon of stability in the Singapore market, and I'm here to dissect what the future holds for this stalwart. Steady Growth in a Resilient Sector: First off, Parkway Life operates in the healthcare real estate sector – a field known for its resilience, especially in uncertain economic times. With a portfolio that includes private hospitals in Singapore and Malaysia, as well as nursing homes across Japan, the reet has a geographically diversified income stream. This diversification not only spreads risk but also taps into the growing demand for healthcare services in these aging societies. Performance Amidst Macroeconomic Challenges: Despite the global economic challenges faced in 2023, Parkway Life showed commendable performance. The reet reported a 2.8% increase in its Distribution Per Unit (DPU) from the same period the previous year. This kind of growth amidst adversity highlights the reet's strong operational capabilities and efficient asset management. Financial Health and Capital Management: Parkway Life boasts a healthy balance sheet – a crucial aspect for any reet. With a gearing ratio of 36.0% and a low all-in cost of debt at 1.32%, it stands in a strong position to weather financial storms and seize growth opportunities. This prudent financial management is essential for sustaining growth and providing stable returns to investors. Expansion and Value Enhancement Opportunities: Looking forward, Parkway Life's potential to expand its portfolio in the high-demand healthcare sector is significant. Strategic acquisitions and asset enhancement initiatives could further bolster its asset value and income streams. The management's track record of making savvy investment decisions bodes well for its ability to capitalize on these opportunities. Analyst Confidence: The confidence shown by analysts, as evidenced in reports like OCBC Investment's, further validates the strong fundamentals and growth prospects of Parkway Life. A target price of S$4.27 reflects a positive outlook and underscores the belief in the reet's ability to continue its growth trajectory. ConclusionAnd that wraps up our in-depth look at Parkway Life reet through the lens of OCBC's latest analysis. We've seen how this reet is setting itself apart with strong financial health, robust growth, and a resilient portfolio in the healthcare sector. It's clear that Parkway Life reet is not just surviving but thriving, even in challenging economic times, making it a potentially attractive option for investors in 2024.

If you found this analysis helpful and want to stay updated with more insightful reviews and investment tips, please hit that like button and subscribe to Investing Iguana. Your support encourages us to keep bringing valuable content to help you make informed investment decisions. Feel free to share your thoughts or questions about Parkway Life reet in the comments below – let's keep the conversation going. Stay tuned for more expert investment insights from Investing Iguana. Until next time, invest wisely and keep aiming high! IntroductionHey there, investors! Welcome back to the Investing Iguana channel, where we dive deep into the dynamic world of investing. I'm Iggy, your guide through the complexities of the market, and today we're focusing on a topic that's been on every savvy investor's radar – Singapore Real Estate Investment Trusts (S-REITs). In a market that's been grappling with high inflation and surging interest rates, some S-REITs have managed to not just survive, but thrive. We're zeroing in on Mapletree Logistics Trust, ParkwayLife reet, and Frasers Hospitality Trust – the standout performers in what many consider a tough market. Join me as we dissect their strategies, analyze their success, and understand what sets these S-REITs apart. So, grab your notepad, and let's get into the nitty-gritty of these market outperformers In the midst of a challenging economic landscape, the performance of Singapore Real Estate Investment Trusts (S-Reits) during the financial period ending 30 September 2023 has been a mixed bag, with a majority reporting a dip in distribution per unit (DPU). Investment advisory platform Beansprout attributes this decline as a contributing factor to the observed weakness in the share prices of these S-Reits. The sector has been navigating through the rough seas of high inflation and soaring interest rates. However, there's a silver lining. As the yield on 10-year US Government Bonds retreated from its mid-October peak, the iEdge S-Reit Index rallied, posting a 9.4% total return. This upswing helped pare down the year-to-date index decline from 9.0% as of 31 October 2023, to a mere 0.4% by 23 November 2023. 3 S-REITSAmid these industry challenges, three S-Reits have stood out by reporting an increase in their year-on-year DPU. Mapletree Logistics Trust (MLT) is one such example. Despite a slight dip in its H1FY2024 gross revenue and net property income, MLT saw a 0.5% increase in its DPU, reaching 4.539 cents. This was achieved even as MLT’s occupancy rate remained robust at 96.9%, despite a minor dip in average rental reversion, primarily affected by its Chinese properties. Interestingly, MLT has been proactive in its portfolio management, announcing several property divestments in Malaysia, Singapore, and Japan, and continuing this trend into November 2023 with more divestments. Another notable performer is ParkwayLife Reit (PLife), which reported a significant 24.6% year-on-year increase in its 9M2023 gross revenue, largely driven by higher rents from a new lease agreement for its three Singapore hospitals and contributions from newly acquired nursing homes in Japan. PLife's DPU also grew by 2.8% year-on-year to 10.99 cents, marking continued growth since its IPO in 2007. Lastly, Frasers Hospitality Trust (FHT) showcased a robust recovery, with a 28.5% year-on-year increase in FY2023 gross revenue and a 30.1% increase in net property income, buoyed by the global tourism sector's resurgence. FHT's distribution per stapled security jumped a noteworthy 49.3% year-on-year to 2.4426 cents. Notably, FHT's overall portfolio value has increased by 1.7% year-on-year to S$1.93 billion as of 30 September 2023, with most country portfolios exceeding pre-Covid levels in terms of Revenue per available room (RevPAR), except for Japan. Mapletree Logistics Trust (MLT) As we gaze into 2024, let's break down what the future might hold for these REITs and what this means for you as an investor. Mapletree Logistics Trust (MLT) has demonstrated a commendable performance in 2023, which has positioned them strongly for the upcoming year. One of the key factors that marked their success was their ability to maintain high occupancy rates across their properties. This not only reflects the effectiveness of their property management strategies but also their ability to retain tenants, which is crucial in the real estate industry. In addition to maintaining occupancy rates, MLT has also engaged in strategic divestments. This involves selling off non-core or underperforming assets, allowing them to focus their resources on more profitable ventures. This strategic move has improved their overall portfolio performance and has set a strong foundation for their operations in 2024. However, the road ahead is not without challenges. The Chinese market, in particular, presents its own set of unique obstacles. The key to overcoming these challenges will be MLT’s approach to navigating this complex market. Their ability to adapt to market conditions and regulatory changes will play a significant role in their success in the Chinese market. Looking ahead, MLT plans to continue focusing on capital recycling and expanding their footprint in more stable regions. This strategy involves reinvesting the proceeds from their divestments into promising new properties or improving existing ones. If executed effectively, this could potentially lead to an increase in their Distribution Per Unit (DPU), which would be a positive outcome for their investors. Investors should also closely watch how MLT manages their rental reversions and property portfolio diversification. These factors will be critical in sustaining their growth amidst global economic uncertainties. By effectively managing these aspects, MLT can ensure a steady stream of revenue and maintain a robust financial position, even in a volatile economic climate. ParkwayLife REIT (PLife) ParkwayLife REIT (PLife) has shown remarkable growth in 2023, laying a strong foundation for the upcoming year. This growth has been primarily driven by strategic acquisitions and enhanced lease agreements, which have not only expanded their portfolio but also strengthened their revenue streams. One of the key strategies that PLife has adopted is the establishment of a third key market. This move is particularly intriguing as it indicates PLife’s ambition to expand its footprint and diversify its portfolio. If PLife successfully navigates this expansion while maintaining their stronghold in their existing markets, Singapore and Japan, we could potentially see further growth in their Distribution Per Unit (DPU). This would be a positive outcome for their investors, potentially leading to higher returns. The healthcare sector, where PLife has a significant presence, is known for its resilience to economic downturns. This adds an element of stability to PLife’s portfolio. In times of economic uncertainty, healthcare REITs like PLife can offer a safe haven for investors, as the demand for healthcare services tends to remain stable, regardless of economic conditions. This makes PLife an attractive option for investors seeking defensive plays. By investing in PLife, investors can potentially benefit from the steady growth and stability of the healthcare sector, while also gaining exposure to PLife’s strategic expansion into new markets. Frasers Hospitality Trust (FHT) Frasers Hospitality Trust (FHT) has shown a strong performance in 2023, which bodes well for their prospects in 2024. This performance has been largely fueled by the global recovery of the tourism sector, a trend that has positively impacted the hospitality industry. However, the sustainability of this recovery will be a key factor to watch in the coming year. If travel and tourism continue on their upward trajectory, and FHT maintains its strategic approach to acquisitions and divestments, we could potentially see further growth in their Distribution Per Share (DPS). FHT’s strategy of diversification across geographies and asset types is another strength that could cushion them against market volatility. By spreading their investments across different regions and types of assets, FHT can mitigate risks associated with any single market or asset type. This diversification strategy not only provides a safety net against market downturns but also opens up opportunities for growth in various markets. ConclusionFor investors eyeing the S-reet market in 2024, these three trusts offer different angles of opportunity. MLT’s strength lies in its logistics and industrial portfolio, PLife in the healthcare sector, and FHT in hospitality. Each comes with its unique set of risks and rewards. As always, the devil is in the details – keep an eye on the macroeconomic factors, interest rate movements, and sector-specific trends.

In conclusion, while the future is never certain, Mapletree Logistics Trust, ParkwayLife reet, and Frasers Hospitality Trust have shown resilience and strategic acumen that bode well for their performance in 2024. As savvy investors, it's crucial to stay informed and agile. This is Iggy, your Investing Iguana, reminding you to do your due diligence and keep adapting your strategies to the ever-changing market landscape. Until next time, stay smart, stay invested! IntroductionWelcome to Investing Iguana, your trusted source for uncovering hidden investment treasures in Singapore. Today, we embark on a journey into the world of IREIT Global, an exceptional real estate investment trust that holds exciting prospects for investors in the heart of the Lion City. 1. Singapore's Trailblazer in European Real EstateAs Singapore’s pioneering European-focused real estate investment trust, IREIT Global stands at the forefront of international property investment since its notable inception on the 13th of August, 2014. With a strategic vision honed on acquiring and managing a lucrative spread of income-generating assets across Europe, IREIT has cultivated a robust portfolio that resonates with the discerning investor in Singapore. This portfolio is a testament to diversity and strategic positioning, encompassing 5 sterling office estates in Germany's robust markets, 5 prime office locations in the dynamic urban landscapes of Spain, and a collection of 27 retail havens in France's bustling consumer districts. Covering a sprawling total lettable expanse of roughly 384,000 square meters, these properties not only exemplify freehold excellence but are also pivotal in sectors critical to European commerce — office, retail, and the industrious realms of logistics. IREIT's assets boast an impressive occupancy rate hovering around 88.3%, a clear indicator of their strategic selections and management acumen. At the heart of IREIT’s operations is the impressive valuation of these European gems, which stands at an estimated €950.5 million. This figure is not just a number; it’s a reflection of IREIT’s commitment to delivering sustainable value to its stakeholders and fortifying Singapore's position in the global real estate market. Through such international ventures, Singaporean investors get to partake in the vibrancy of European economic spaces, right from the comfort of home.  2. Diverse Property PortfolioThis strategic diversification in their portfolio is designed to offer stability and resilience against fluctuating market conditions, which is particularly pertinent in a dynamic market like Singapore's. The diversification strategy allows investors to gain exposure to different segments of the real estate market through IREIT Global's investment platform. By holding a variety of property types in different locations, IREIT Global aims to reduce risks associated with market volatility. Investors benefit by having a stake in a portfolio that is not overly reliant on any single property type or geographic location. This is a crucial consideration for Singapore-based investors, given the city-state's limited size and the competitive nature of its property markets. The diverse nature of IREIT's portfolio, with a total of 99 tenants, indicates a wide-ranging tenant base, which further contributes to the stability of the investment since the risk is spread across many different businesses and sectors. 3. Strategic LocationsFor instance, IREIT Global has expanded its portfolio by acquiring a French retail portfolio from B&M, comprising 17 fully occupied sites which account for a substantial percentage of B&M stores in France. These properties boast a long Weighted Average Lease Expiry (WALE), indicating stable long-term rental income potential. Additionally, a significant deal was struck to buy a portfolio of 27 retail properties in France from Decathlon, a well-known sporting goods retailer, further emphasizing their strategic presence in prime retail locations. A specific example of their strategic property locations is the Darmstadt Campus, situated in a prime office location within a commercial zone in Europe. This property benefits from being at the gateway to Europaviertel and enjoys excellent connectivity to public transportation, with the main train station being just a short walk away. In simple English, investing in IREIT Global means putting money into a company that owns a variety of buildings in Europe that are used for work, shopping, and industry. These buildings are in places where a lot of people go for business and shopping, which means they are likely to be rented out consistently and could increase in value over time. The company is from Singapore but owns properties in Europe, including shops that are rented out to a big store chain in France and offices in a busy business area.  4. Trustworthy ManagementTrust is the cornerstone of any successful real estate investment, and IREIT Global prides itself on delivering just that. At the helm of this trust is a seasoned and highly competent management team. These industry veterans bring with them a proven track record of success, ensuring that IREIT Global is guided by experienced hands capable of navigating the complexities of the real estate market with precision and foresight. IREIT Global is indeed managed by a highly competent team. The management team of IREIT Global is led by Mr. Louis D’Estienne D’Orves, who serves as the Chief Executive Officer, and Ms. Chua Tai Hua, Anne, who is the Chief Financial Officer. As the Chief Executive Officer, Mr. D’Estienne D’Orves is responsible for planning and implementing IREIT’s investment strategy, the overall day-to-day management and operations of IREIT, as well as working with the Manager’s investment, asset management, financial, legal, and compliance personnel in meeting IREIT’s strategic investment. IREIT Global is managed by IREIT Global Group Pte. Ltd., which is jointly owned by Tikehau Capital and City Developments Limited (CDL). Tikehau Capital is a global alternative asset management group listed in France, while CDL is a leading global real estate company listed in Singapore. This experienced management team, along with the strategic backing of Tikehau Capital and CDL, ensures that IREIT Global is well-positioned to navigate the complexities of the real estate market and deliver value to its investors. 5. Consistent Rental IncomeIREIT Global offers a sense of financial security to those who invest for income, like receiving rent. This happens because they have agreements that last a long time with reliable tenants. For instance, their main tenant at the Berlin Campus has agreed to stay longer, until the end of 2024, and will pay even more rent—about 45% more. This Berlin Campus is very important because it brings in nearly a quarter of IREIT Global's rent money every year. They also have a new 15-year lease with a German government agency at the Darmstadt Campus, which shows they can keep making money from rent for a long time. And for a big retail portfolio in France, they have tenants staying for an average of almost 7 years, which also helps make sure they get a steady flow of rent money. What’s more, even though IREIT Global has borrowed money, they've been careful to fix the interest rates they pay back, which helps them manage their money well over time. However, they're prepared for the costs to go up a little if they need to borrow more for big projects or day-to-day expenses. This careful planning means investors can count on getting regular rent money, which can help them reach their money goals and feel more secure about their future. 6. Active Portfolio Enhancement IREIT Global is actively managed by a team that doesn't just passively watch its investments. They are always looking for ways to make their portfolio better. This could be by buying new properties, fixing up ones they already have, or doing things that make their properties worth more. They do this to stay competitive and to keep up with the changing real estate market. In 2021, despite the challenges of the pandemic, IREIT Global managed to achieve a lot. They bought a retail portfolio in France and an office building in Spain. They also raised funds to pay for these purchases and were able to lease out a lot of their properties. They plan to keep investing and changing their portfolio to include different types of assets and ways to make money. They will use the strengths of their joint sponsors, Tikehau Capital and City Developments Limited, to grow and diversify their business.  7. Transparent ReportingIn the investment community, clarity and openness are essential, and IREIT Global stands out for its dedication to these principles. As a real estate investment trust listed on the Singapore Exchange since 2014, IREIT Global has a clear strategy of investing in income-generating properties across Europe, which they share with their investors. They have demonstrated this commitment through consistent publication of comprehensive annual reports since their listing, detailing their financial activities and offering stakeholders a transparent view of the trust's performance. Moreover, IREIT Global provides regular financial updates, such as condensed interim financial statements, which include detailed financial figures and comparisons with previous periods. For instance, they've published their financial statements for the second half and the full year ended 31 December 2022, indicating a transparent approach to keeping stakeholders informed about their financial status. Additionally, investor presentations and meetings are a routine part of their investor relations, offering further insight into the trust's operations, strategies, and growth. This includes presentations of half-year results, extraordinary general meetings, and other significant updates, such as the acquisition of retail properties, which suggests a proactive approach in engaging with their investors and maintaining a two-way communication channel. In simple terms, IREIT Global makes sure that anyone who puts money into the trust knows how their investment is doing. They regularly share detailed reports and updates about their money matters. This helps build a strong trust with the people who invest with them, showing that they are a trustworthy option for putting one's money into. 8. Tax-Efficient InvestmentIREIT Global's investment structure in Singapore is indeed designed to be tax-efficient. The capital distribution component of IREIT Global is considered a return of capital to unitholders for Singapore income tax purposes. This means the amount distributed will reduce the cost base of the unitholder's units. When unitholders who are liable to pay Singapore income tax on profits from the sale of their units decide to sell, the reduced cost base will be used to calculate any taxable gains. This structure can lead to potential tax savings and enhance the overall returns for investors.  9. City Developments Limited as a part-ownerCity Developments Limited (CDL) has indeed made significant investments in IREIT Global, holding a substantial stake in the company. CDL has acquired a 12.4% stake in IREIT Global, and additionally, it owns 50% of IREIT Global Group Pte. Ltd., the manager of the European property trust. As of the latest available information, CDL holds 21% of the total issued units in IREIT Global. Regarding CDL's global presence, the company's network spans 143 locations across 28 countries and regions, with a diversified portfolio that includes residential, commercial, and hotel properties. CDL is one of Singapore's largest companies by market capitalization, and its income-stable and geographically diverse portfolio includes a range of residences, offices, hotels, serviced apartments, student accommodations, retail malls, and integrated developments. The company has a history of over 60 years in real estate development, investment, and management. Throughout its history, CDL has developed over 50,000 homes and currently owns approximately 21 million square feet of gross floor area in residential, commercial, and hospitality assets worldwide. Additionally, CDL's wholly-owned hotel subsidiary, Millennium & Copthorne Hotels Limited, operates over 150 hotels internationally, with many located in key gateway cities. 10. Investor-Friendly ApproachIREIT Global fosters an environment that values its investors, demonstrated by their structured and transparent approach to shareholder engagement. The trust conducts annual general meetings (AGMs) and extraordinary general meetings (EGMs), where investors are invited to participate. The 2023 AGM, for instance, was held on 25 April, with provisions for proxy voting, ensuring investors' voices are heard even if they cannot attend in person. The meetings are opportunities for shareholders to ask questions, delve into the trust's performance, and make informed decisions. This interactive approach cultivates a sense of involvement and community among investors, reinforcing the trust's commitment to transparency and accountability. For more details on how IREIT Global engages with its investors and the specifics of its AGM and EGM practices, you may visit their investor relations page on their official website. ConclusionIn summary, IREIT Global emerges as a formidable player in Singapore's real estate investment landscape. Its deep-rooted connection with Singapore, diverse and strategically positioned property portfolio, commitment to transparency, and investor-centric approach make it an exceptional choice for savvy investors in the Lion City. If you're looking to unlock the full potential of your investments in Singapore's dynamic real estate market, consider IREIT Global as a worthy addition to your portfolio.

If you found this video helpful, please hit that 'Like' button. It really helps us to understand what kind of content you want to see more of. And don't forget to subscribe! Here at 'The Investing Iguana', we're dedicated to helping you navigate your financial journey with confidence and clarity. And guess what? There's plenty more where this came from! Stay tuned for our upcoming videos, where we'll tackle other interesting financial topics like the best investment strategies, understanding the stock market, and how to make your money work harder for you! As always, we're thrilled to have you as part of our 'Investing Iguana' community. Your support helps us keep producing free content like this. Remember, every 'like', 'share', and 'subscribe' goes a long way! Thanks for joining us today. Keep investing, keep growing, and we'll see you in the next video. Bye for now! IntroductionHey, everyone! Welcome back to The Investing Iguana, your go-to channel for all things investment-related. I'm Iggy, your friendly and knowledgeable guide to the intricate yet super interesting universe of investments. Today, we're going to explore a topic that's buzzing in the minds of many—Real Estate Investment Trusts, commonly known as REITs. We're zooming in on one reet in particular, which is Frasers Logistics & Commercial Trust, or FLCT for short. You might also recognize it by its stock market ticker, which is SGX: BUOU. So, get ready, grab a notebook and a pen, or even your phone to jot down notes, because I've got not just a few, but seven essential facts that you absolutely must know about FLCT. Alright, let's kick things off by answering a basic question—what exactly is FLCT? Well, FLCT is a Real Estate Investment Trust based in Singapore that specializes in putting its money into properties that generate a steady income. We're talking about logistics centers, industrial buildings, and commercial spaces. But hold on, it's not just limited to Singapore! FLCT has a global reach, extending its investments to countries like Australia, Germany, the Netherlands, and even the United Kingdom. Think of it as the United Nations of the real estate world, but with a twist—it actually pays you dividends! So, it's like getting a little reward just for being part of it. Isn't that awesome? History of FLCTLet's take a moment to learn some history. FLCT, which stands for Frasers Logistics & Commercial Trust, came into existence in April 2020. How did it happen? Well, two different trusts, Frasers Logistics & Industrial Trust and Frasers Commercial Trust, decided to join forces and become one big trust. Even though it sounds like FLCT is pretty new, you shouldn't underestimate it. Fast forward to June 2023, and guess what? FLCT has grown incredibly strong and successful. It now owns a whopping 107 different properties, like buildings and land, and all of these together are worth an amazing S$6.9 billion. That's a lot of money! So, even though FLCT might seem young, it's already a big player in the game, showing that it's both strong and valuable. All Eggs in One Basket?So, let's talk about my next big idea, which is called diversification. You know how you shouldn't put all your eggs in one basket? Well, that's exactly what diversification is all about, and this company FLCT is really good at it. Imagine their business like a big pie. About 60% of that pie is made up of logistics properties, which are places where stuff gets moved around and stored. Then, another 30% of the pie is industrial properties, which are like big factories where things are made. The last slice, about 10%, is commercial properties, like offices and shops where people work and buy things. So, you see, they have a mix of different types of properties, which is really smart because if one part isn't doing so well, the other parts can help balance it out. Now, who rents these properties? It's a mix of big international companies and smaller local ones. They come from all sorts of industries like online shopping, moving goods around, making products, and even stores where you go shopping. So, FLCT is not just relying on one type of business or one type of property. They're spreading their eggs across many baskets, and that's a really smart way to do things. Frasers Logistics & Commercial Asset ManagementFor our third interesting point, let's dive into who's in charge of running things at FLCT. The company that manages FLCT is called Frasers Logistics & Commercial Asset Management. This management company is actually a smaller part of a much bigger company known as Frasers Property Limited. Now, if you haven't heard of Frasers Property, it's time to get familiar because they're a really big deal, especially in Singapore where they're super famous in the world of buildings and land. But they're not just big in Singapore; they're also a global powerhouse with their business stretching across more than 10 different countries around the world. So, when you decide to invest in properties that are part of FLCT, you're not just putting your money into bricks and mortar. Nope, you're also investing in a team of people who really know what they're doing. They've got tons of experience and they're super reliable, so you can feel confident that your investment is in good hands. FLCT Investment ApproachFact number four focuses on how FLCT goes about its investment approach. You see, what they do is look for really good properties that are logistics, industrial, and commercial types, and they choose ones that are in places that make a lot of sense for business. It's like they're on a treasure hunt for the best spots to set up shop. But they don't just buy these properties and call it a day. Oh no, they take it a step further. After they've bought these properties, they work on making them even better. They have special plans and projects, known as asset enhancement initiatives and redevelopments, to increase the value of what they own. It's like they don't just buy a super cool racecar; they keep working on it, tuning the engine, adjusting the wheels, and maybe even giving it a new paint job, all to make sure it runs at its absolute best. So, in simple terms, FLCT is all about smart buying and smarter improving. FLCT ReturnsSure, let's dive into why people invest money. The main reason is to get more money back, right? That's what we call "returns." Now, there's this company called FLCT, and they're really good at giving people more money for their investment. They have a history of doing this really well, year after year. So, let's get into some numbers. In the year that ended in March 2023, FLCT gave back S$0.0567 for each unit of investment. This might sound like just a bunch of numbers and letters, but it's actually really important. It means that if you invested in them, you would get a 7.12% return on your money based on how much one unit of their investment cost in the middle of October 2023. So, in simple terms, if you put your money with them, you're likely to see it grow by 7.12%, and that's pretty awesome, don't you think? FLCT Areas of FocusFact number six focuses on the specific areas where FLCT is expected to do really well. You see, FLCT has a lot of properties that are connected to logistics and online shopping, or what we call e-commerce. Logistics is like the behind-the-scenes magic that helps move things from one place to another, and e-commerce is basically shopping online. Because more and more people are shopping online these days, and businesses need to move their products efficiently, these sectors are growing fast. So, FLCT is in a really good position to benefit from this growth over a long period of time. It's like FLCT has planted seeds in a garden that's going to grow a lot in the future. This makes investing in FLCT a smart choice if you're thinking about the long-term, kind of like planting a tree and watching it grow bigger over the years. So, if you're looking for an investment that's geared towards the future and is likely to grow along with these booming sectors, FLCT is definitely an option worth considering. Well-run REITCertainly! So, the seventh and final thing you should know is that this Real Estate Investment Trust, or REIT for short, called FLCT, is really, really good at what it does. It's not just any old REIT that buys and manages properties. Nope, it's special because it has a mix of different types of top-notch properties, like a fruit salad with all your favorite fruits! This makes it strong and less likely to be hurt if one type of property isn't doing well. The people running FLCT are super smart and careful. They have a game plan that's like a strong fortress, built to stand tall even when the financial weather gets stormy. So, it's not just about making money right now; they're in it for the long run. They want to keep making money year after year, in a way that's steady and reliable. So, to sum it up, FLCT is a really well-run REIT with a variety of excellent properties, and it's designed to be strong and make money for a long time, even when things get a little shaky in the market. ConclusionAlright, listen up! We've just gone through seven super important things you need to know about Frasers Logistics & Commercial Trust. It doesn't matter if you're a seasoned pro at investing or if you're just starting out and dipping your toes into the world of Real Estate Investment Trusts (REITs)—you should absolutely keep an eye on FLCT. It's something you won't want to miss out on.