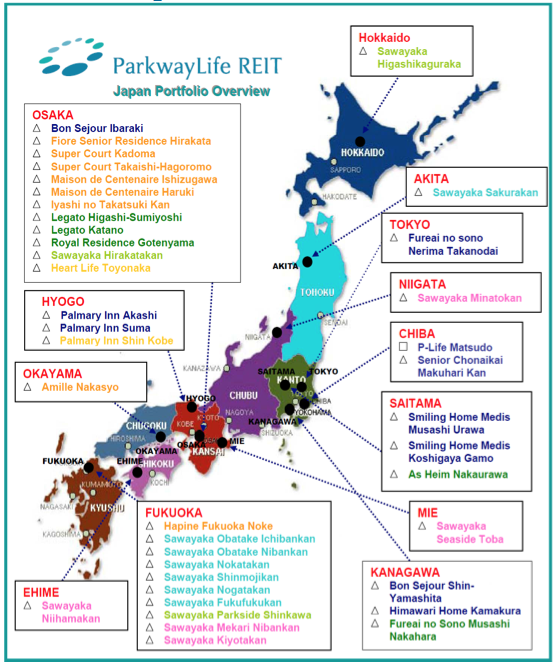

Introduction: Parkway Life REIT: Asia's Largest Healthcare REITParkway Life REIT, or PLife REIT for short, is one of Asia’s largest listed healthcare REITs. It invests in income-producing real estate and real estate-related assets used primarily for healthcare and healthcare-related purposes. It is listed on the Singapore Exchange Securities Trading Limited (SGX-ST). It was formed in 2007 and is managed by Parkway Life REIT Management Limited. As of 30 June 2023, PLife REIT’s total portfolio size stands at 61 properties totaling approximately S$2.20 billion. The properties in PLife REIT's portfolio are located in Singapore, Japan, and Australia. The majority of the properties are nursing homes, with the remainder being hospitals, medical centers, and other healthcare-related assets. The Singapore portfolio consists of three hospitals: Mount Elizabeth Hospital, Gleneagles Hospital, and Parkway East Hospital. These are some of the most prestigious and well-known private hospitals in Singapore, offering a wide range of medical services and specialties. They are also strategically located in prime areas with high accessibility and visibility. The Japan portfolio consists of 50 properties, comprising 49 nursing homes and one pharmaceutical product distributing and manufacturing facility. These properties are located across various regions in Japan, such as Hokkaido, Kanto, Chubu, Kansai, Chugoku, Shikoku, and Kyushu. They cater to the growing demand for elderly care services in Japan, which has one of the world’s fastest aging populations.  How does PLife REIT make money? Parkway Life REIT (PLife REIT) makes money mainly from the rent it collects from its tenants. The rent is usually based on a fixed lease agreement with regular rental escalations. This means that PLife REIT can enjoy stable and predictable income streams regardless of the occupancy or performance of its properties. PLife REIT has 30 properties in Singapore, which account for 57.4% of its total portfolio value. These properties are mostly nursing homes, with the remainder being hospitals and medical centers. The rent for the Singapore portfolio is linked to the consumer price index (CPI) of Singapore. This means that PLife REIT can benefit from inflation protection as well as potential upside from positive CPI growth. The lease term for the Singapore portfolio is 15 years with an option to renew for another 15 years. The current lease will expire in August 2029. PLife REIT has 19 properties in Japan, which account for 29.2% of its total portfolio value. These properties are mostly nursing homes, with the remainder being hospitals and other healthcare-related assets. The rent for the Japan portfolio is linked to the CPI of Japan or a fixed percentage increase (whichever is higher). This means that PLife REIT can also enjoy inflation protection as well as guaranteed rental growth for its Japan properties. The lease term for the Japan portfolio ranges from 10 to 20 years with an option to renew for another 10 to 20 years. PLife REIT has 2 properties in Malaysia, which account for 13.4% of its total portfolio value. These properties are both nursing homes. In addition to rent, PLife REIT also generates income from other sources, such as management fees and development income. However, rent is the main source of income for PLife REIT.  How has PLife REIT performed financially? Parkway Life REIT (PLife REIT) has delivered consistent and impressive financial performance over the years. It has achieved positive growth in its revenue, net property income (NPI), distributable income (DI), distribution per unit (DPU), net asset value (NAV) per unit, and gearing ratio. Here are some key financial highlights from its latest quarterly report as of 30 June 2023:

Overall, Parkway Life REIT financial performance remains strong. The REIT is well-positioned to continue delivering sustainable growth in the future. Additional DetailsHere are some additional details about Parkway Life REIT's financial performance:

What are the growth prospects of PLife REIT?Parkway Life REIT (PLife REIT) has a strong growth potential due to its exposure to the resilient and defensive healthcare sector. The healthcare sector is driven by favorable long-term trends, such as: Aging population: The proportion of elderly people (aged 65 and above) is expected to increase significantly in Singapore, Japan, and Malaysia in the coming years. This will lead to higher demand for healthcare services and facilities, especially for chronic and age-related diseases. Rising income and affluence: The income and wealth levels of people in Singapore, Japan, and Malaysia are expected to rise in the future. This will enable them to afford better quality and more sophisticated healthcare services and facilities, especially for elective and preventive care. Medical tourism: Singapore, Japan, and Malaysia are attractive destinations for medical tourists from other countries, especially from the region. This will boost the demand for healthcare services and facilities, especially for specialized and niche treatments. These trends are expected to drive the growth of the healthcare sector in Singapore, Japan, and Malaysia over the long term. Parkway Life REITis well-positioned to benefit from this growth, as it has a portfolio of healthcare properties in these countries. In addition to the favorable long-term trends, Parkway Life REIT also has a number of other factors that support its growth potential. These include:

Recent Growth Initiatives by PLife REITParkway Life REIT (PLife REIT) has also demonstrated its ability to grow organically and inorganically over the years. It has achieved organic growth through regular rental escalations, positive rental reversions, asset enhancement initiatives (AEIs), and green initiatives. It has achieved inorganic growth through strategic acquisitions, divestments, and joint ventures. Some of the recent growth initiatives undertaken by PLife REIT include:

PLife REIT has also stated its intention to explore opportunities in new markets, such as China, Australia, and Europe. It has also expressed its interest in diversifying into other sub-sectors of healthcare, such as medical office buildings, laboratories, and wellness centers. These initiatives demonstrate PLife REIT s commitment to growth and its ability to adapt to the changing healthcare landscape. The REIT is well-positioned to continue growing its portfolio and its income stream in the years to come. Should you invest in PLife REIT ?Based on the information I have gathered, I think that PLife REIT is a solid investment for anyone who is looking for a stable and growing income stream from the healthcare sector. PLife REIT has a high-quality portfolio of healthcare properties that are well-located, well-managed, and well-tenanted. It has a strong track record of financial performance and distribution growth. It has a low risk profile due to its long-term leases, high occupancy rate, and low gearing ratio. It has a bright growth outlook due to its exposure to favorable long-term trends and its ability to execute organic and inorganic growth strategies. Of course, PLife REIT is not without its challenges and risks. Some of the possible challenges and risks that PLife REIT may face include:

It is important to carefully consider these challenges and risks before investing in PLife REIT . However, I believe that the potential rewards outweigh the risks, and PLife REIT is a good investment for investors who are looking for a stable and growing income stream from the healthcare sector. ConclusionThat’s all for today’s article and video on Parkway Life REIT. I hope you found it useful and informative. If you did, please give it a thumbs up, share it with your friends, and leave a comment below. I’d love to hear your thoughts and opinions on PLife REIT and the healthcare sector in general.

Introduction: Background of First REITFirst REIT is a Singapore-listed real estate investment trust (REIT) that focuses on healthcare properties in Indonesia, Japan, and Singapore. It was listed on the Singapore Exchange Securities Trading Limited (SGX-ST) on 11 December 2006. The REIT's portfolio consists of 32 properties, with a total net lettable area of over 1.1 million square meters. The properties are operated by a variety of healthcare providers, including PT Siloam International Hospitals Tbk, a leading private hospital operator in Indonesia, and Perpetual Healthcare Pte Ltd, a leading nursing home operator in Singapore. First REIT is managed by First REIT Management Limited, which is a wholly-owned subsidiary of OUE Limited. OUE Limited is a leading diversified group of companies with interests in real estate, infrastructure, and telecommunications. First REIT is the first healthcare REIT in Singapore and the first REIT to be listed on the SGX-ST with a focus on Indonesia. The REIT has been well-received by investors and has been consistently listed in the MSCI Singapore REIT Index. First REIT is well-positioned to benefit from the growing demand for healthcare services in Indonesia, Japan, and Singapore. The Indonesian healthcare market is expected to grow at a compound annual growth rate (CAGR) of 7.5% from 2022 to 2027, while the Japanese healthcare market is expected to grow at a CAGR of 4.5% from 2022 to 2027. The Singaporean healthcare market is already mature, but it is still expected to grow at a CAGR of 2.5% from 2022 to 2027. How has First REIT performed? First REIT has delivered consistent growth in its revenue, net property income, distributable income, and distribution per unit (DPU) since its listing in 2006. It has also achieved positive rental reversion rates for its properties. In 2022, First REIT reported a revenue of S$116.5 million, up by 1.8% year-on-year. Its net property income was S$112.7 million, up by 2.3% year-on-year. Its distributable income was S$67.9 million, down by 3.6% year-on-year due to higher interest expenses and retention of S$3 million for working capital purposes. Its DPU was 6.75 cents, down by 5.6% year-on-year. As of 31 December 2022, First REIT had an occupancy rate of 94.5%, a weighted average lease expiry (WALE) of 8.9 years, and a gearing ratio of 39.9%. Its interest coverage ratio was 3.7 times and its average cost of debt was 5.1%. Here are some key takeaways from the text:

First REIT's PortfolioFirst REIT's portfolio is diversified across Indonesia, Japan and Singapore. The properties are a mix of hospitals, nursing homes and hotels. The hospitals are located in major cities in Indonesia, while the nursing homes and hotels are located in Japan and Singapore. First REIT's portfolio is well-positioned to benefit from the growing demand for healthcare and healthcare-related facilities in Indonesia, Japan and Singapore. The Indonesian healthcare market is expected to grow at a compound annual growth rate (CAGR) of 7.5% from 2022 to 2027, while the Japanese healthcare market is expected to grow at a CAGR of 4.5% from 2022 to 2027. The Singaporean healthcare market is already mature, but it is still expected to grow at a CAGR of 2.5% from 2022 to 2027. Breaking down what happened to First REIT during COVID First REIT, a Real Estate Investment Trust (REIT), faced a series of challenges that led to a breakdown in its business. First REIT, known for its investment in healthcare properties, had entered into long-term master leases with hospitals in Indonesia. These leases provided a stable rental income and attracted investors. However, the outbreak of the COVID-19 pandemic severely impacted the healthcare industry, leading to a significant drop in occupancy rates and rental income for First REIT. As a result, the share price of First REIT plummeted, causing distress among its unitholders. To address its financial difficulties, First REIT decided to conduct a rights issue to raise capital and refinance its debt. However, this move further diluted the shares and added additional burden to the already skeptical investors. In addition, the valuation of First REIT's investment properties was negatively affected, impacting its overall investment portfolio. Consequently, the future prospects of First REIT remain uncertain as it grapples with the aftermath of the pandemic and struggles to regain its footing in the market. The REIT conducted a rights issue to raise capital and refinance its debt in December 2020, not 2022 as implied by the statement. The rights issue was highly dilutive and resulted in a significant drop in the share price and distribution per unit (DPU) of the REIT.  First REIT's new growth strategy 2.0The healthcare sector offers immense opportunities, underpinned by factors such as the structural demographic megatrend of ageing population, and a demand for quality healthcare services in markets that lack capacity. To capture the immense opportunities in the healthcare sector, and to ensure sustainable long-term growth to maximise returns for all stakeholders, First REIT is guided by its ‘2.0 Growth Strategy’, comprising the following four well-defined strategic pillars: (1) Diversify into developed markets. First REIT aims to reduce geographical and tenant concentration risk and targets to increase presence in developed markets to more than 50% of AUM by FY2027. (2) Reshape portfolio for capital efficient growth. First REIT aims to recycle capital from non core, non-healthcare or mature assets for reinvestment. (3) Strengthen capital structure to remain resilient. First REIT aims to diversify funding sources and continue to optimise financial position. And (4) Pivoting to megatrends. First REIT will look at environmental, social and governance areas, including ageing population, demographics and other growth drivers. Based on Growth Strategy 2.0, First REIT managed to accomplish the following in 2022. They extended the Hak Guna Bangunan title for Siloam Hospitals Lippo Cikarang for another 20 years to the year 2043. They received unitholders' approval and acquired 12 nursing homes in Japan. Rental and other income grew 0.4% year-on-year to S$54.0 million in 1H 2023, mainly due to a full half-year rental income contribution from 12 Japan nursing homes acquired from sponsor OUE Healthcare Limited in March 2022 and two additional Japan nursing homes acquired from third parties in September 2022. The Trust’s portfolio in Indonesia and in Singapore also registered improvement in rental income. However, the growth in rental income was partly offset by the depreciation of the Indonesian Rupiah and the Japanese Yen against the Singapore Dollar in 1H 2023 compared to 1H 2022. With the new Japan portfolio, property operating expenses increased to S$1.6 million in 1H 2023 from $1.1 million to 1H 2022, leading to a 0.6% dip in Net property and other income (“NPI”) to S$52.4 million in 1H 2023. Finance costs also increased to S$11.2 million in 1H 2023 from S$8.4 million in 1H 2022, mainly due to higher borrowings coupled with higher interest rates. As a result, distributable amount in 1H 2023 grew only 1.0% to S$25.5 million. As at 30 June 2023, net asset value (“NAV”) per unit improved to 31.02 Singapore cents from 30.70 Singapore cents as at 31 December 2022, due to the appreciation of Indonesian Rupiah against Singapore Dollar during 1H 2023. Separately, rentals outstanding from PT Metropolis Propertindo Utama (“PT MPU”) amounts to approximately S$4.2 million as at 30 June 2023, while security deposits of approximately S$2.3 million was received from PT MPU. As at 31 July 2023, PT MPU has further repaid approximately S$2.0 million, which together with the security deposits are in excess of the remaining outstanding rental receivables. The management will continue to engage closely with PT MPU on the repayment of the rental in arrears.  First REIT Delivers Sustainable Rental Growth in 1H 2023Mr Victor Tan, Executive Director and Chief Executive Officer of the Manager, said, “All of the Trust’s 32 high-quality healthcare and healthcare-related properties continued to deliver sustainable rental growth in 1H 2023. Global economic uncertainties have brought about a challenging business environment, but the Trust has grown in resilience through the early refinancing of debt and the ongoing diversification of our geographical and tenant mix, in line with First REIT’s 2.0 Growth Strategy. “Our nursing homes in Japan and Singapore now comprises more than one-quarter of the Trust’s AUM, and we remain committed towards growing our developed markets portfolio to more than half of the Trust’s AUM by FY2027. We also continue to ride on the strong demand for quality healthcare services in Indonesia. With an increasingly diversified portfolio, we expect to remain well-positioned to generate sustainable growth for our Unitholders.” First REIT's OutlookThe healthcare real estate sector is a large and growing market. This is supported by factors such as the structural demand for quality healthcare services where there is low capacity, and the ageing population megatrend. In Indonesia, the demand for quality healthcare is resilient, due to growing affluence. According to BMI, middle-to-upper-income households are expected to grow from 38.8% of total households in 2023 to 40.4% in 2027. While hospital bed capacity in Indonesia has been below the regional average, the Indonesian Parliament has passed into law a new Health Bill allowing foreign medical specialists to practice and be based in the country. In Japan, people aged 65 and older are expected to grow from 29.9% of the population in 2022 to 37.5% of the population by 2050. In Singapore, the country is expected to become a "super aged" society in 2026, as 21% of the population will be 65 years old or older. In line with First REIT 2.0 Growth Strategy, First REIT will continue to seek opportunities to diversify into developed markets, reshape its portfolio for capital-efficient growth through the divestment of non-core, non-healthcare, or mature assets, and to continue to strengthen its capital structure. With strong support from its Sponsors, OUE Limited and OUE Healthcare Limited, First REIT is well positioned to deliver sustainable distributions to Unitholders in the long term. First REIT's Analysts CoverageBased on analyst Ada of OCBC in August 2023, First REIT’s 1H23 results met their expectations. Rental income grew 0.4% y-o-y to S$54m, while net property income (NPI) declined 0.6% y-o-y to S$52.4m. During the quarter, First REIT carried out an early refinancing of its JPY-denominated Tokutei Mokuteki Kaisha (TMK) bonds, which were originally due in May 2025, terming it out to 2030. As a result, weighted average debt to maturity has increased to 4.1 years as at 30 Jun 2023. First REIT has no refinancing requirements until May 2026. Interest coverage ratio dipped slightly to 4.1x from 4.2x on 31 Mar 2023, but remains at a healthy level. Maintain fair value estimate of S$0.30. Based on analyst Elizabella of DBS coverage in June 2023, A Breath Of New Life; Initiate With BUY. As at FY22, First REIT has 32 assets with assets under management (AUM) of S$1.15bn, with 15 assets in Indonesia (72.1% of AUM), 14 nursing homes in Japan (25.1%), and 3 nursing homes in Singapore (2.8%), with a WALE of 12.2 years (as at 1Q23). Worst is over; a more sustainable master lease structure is now in place for First REIT. Most importantly, we believe rebased rents are now more sustainable for hospital operator Siloam, with rent as a percentage of EBITDAR1 estimated to be in the range of 40%-45%, aligned with the industry, versus an estimated 60% prior to the restructuring. Furthermore, with Siloam being added as a party in the MLAs, First REIT will be able to directly collect its rent from its hospital operator and reduce its concentration risks to LPKR, suggesting that First REIT’s rents will be more correlated to the performance of Siloam. Potential upside from growing in tandem with high long-term growth trajectory of Siloam. Initiate with BUY recommendation of S$0.30, based on DCF valuation. According to Yahoo Finance, First REIT's current stock price is SGD0.265 as of August 22, 2023.  What are the growth prospects and risks for First REIT?First REIT has several growth drivers that could enhance its value and income in the future. These include:

However, First REIT also faces several risks that could affect its performance and outlook. These include:

Overall, First REIT has several growth drivers that could enhance its value and income in the future. However, the REIT also faces several risks that could affect its performance and outlook. Investors should carefully consider these risks before investing in First REIT. Is it a good time to invest in First REIT?Based on the above analysis, First REIT seems to offer a compelling value proposition for investors who are looking for a high-yield healthcare REIT with exposure to the fast-growing Asian markets. However, it also comes with significant risks that could affect its stability and sustainability.

Therefore, whether it is a good time to invest in First REIT depends on your risk appetite, investment horizon, and portfolio allocation. You should also do your own due diligence and research before making any investment decision. |

Author🦖 Welcome to the Investing Iguana YouTube channel, your one-stop destination for all things related to investment tips, news, and advice! Our mission is to empower you with the knowledge and insights you need to make informed investment decisions and grow your wealth. With a perfect blend of engaging content, expert advice, and practical strategies, the Investing Iguana is here to guide you through the complex world of investing and help you achieve your financial goals. Archives

January 2024

Categories

All

|

RSS Feed

RSS Feed